Virginia Notice of Default for Past Due Payments in connection with Contract for Deed

What is this form?

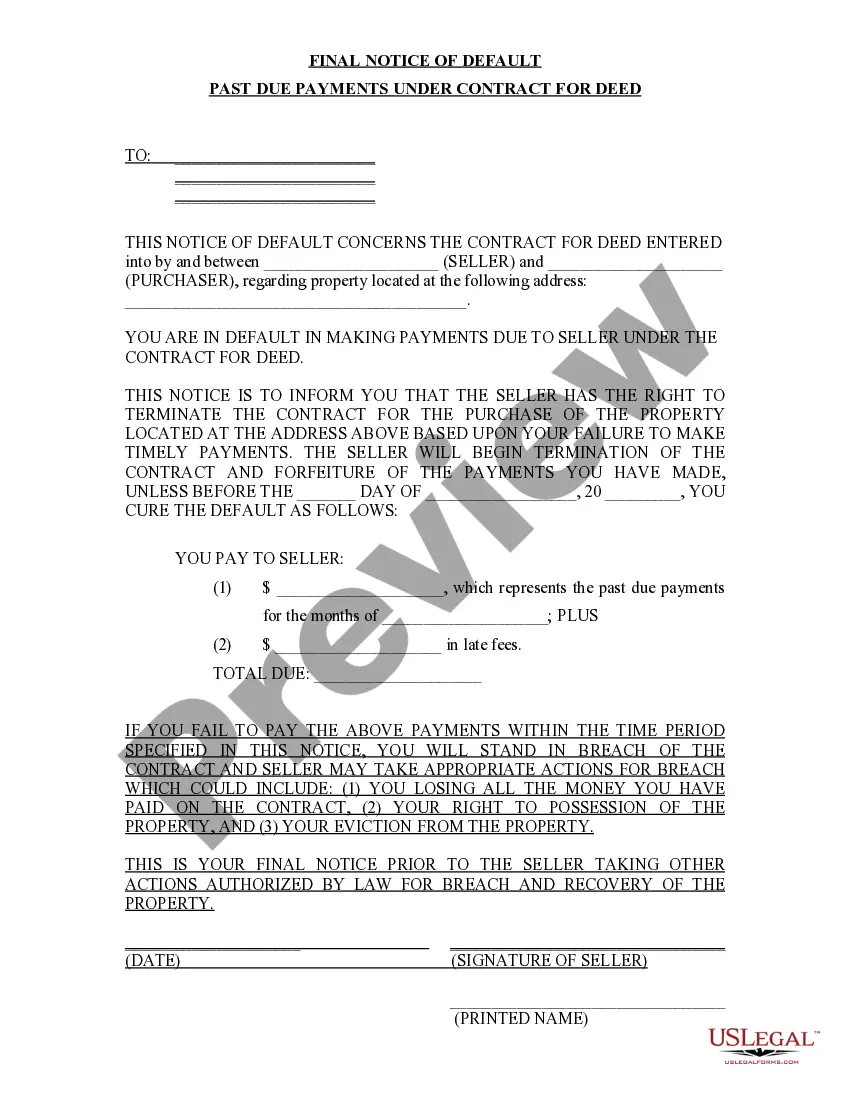

The Notice of Default for Past Due Payments in connection with Contract for Deed serves as an initial notification from the seller to the purchaser, indicating that payments have not been made according to the terms of the contract for deed. This legal document informs the purchaser that failure to respond could lead to the termination of the contract, setting it apart from other notification forms typically used in real estate transactions.

What’s included in this form

- Identification of the seller and purchaser, including names and contact information.

- Details of the property associated with the contract for deed.

- Notification of payment default and the consequences of failing to cure the default.

- Specific details on the amount due, including past due payments and late fees.

- Deadline for the purchaser to respond and remedy the default.

- Signature of the seller, confirming the notice has been issued.

Common use cases

This form is necessary when a purchaser under a contract for deed has failed to make timely payments. It serves as an official notice to alert the purchaser of their default status and the potential actions that the seller may take, which can include eviction and loss of any payments already made. Using this notice properly helps clarify the seller's rights and the purchaser's obligations under the contract.

Who this form is for

- Sellers of property who have entered into a contract for deed and are experiencing payment delays.

- Lawyers representing sellers in real estate transactions involving contracts for deed.

- Buyers who have received a notice and wish to understand their obligations.

Steps to complete this form

- Identify and enter the names of both the seller and purchaser at the beginning of the notice.

- Clearly state the address of the property involved in the contract for deed.

- Specify the past due payment amount and any applicable late fees.

- Set a deadline for the purchaser to remedy the default.

- Sign and date the notice to confirm its validity.

Is notarization required?

Notarization is required for this form to take effect. Our online notarization service, powered by Notarize, lets you verify and sign documents remotely through an encrypted video session, available 24/7.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Typical mistakes to avoid

- Failing to include all required parties' names, which can lead to disputes.

- Not specifying the exact amounts due, making it unclear for the purchaser.

- Missing the deadline for the purchaser to cure the default, impacting enforceability.

- Not signing the notice, which may invalidate the document.

Why complete this form online

- Convenient access to forms that can be downloaded and completed at your own pace.

- Editable templates that allow for customization to your specific situation.

- Reliable content drafted by licensed attorneys, ensuring legal compliance.

Legal use & context

- This notice serves as official documentation of the Purchaser's default status.

- Failure to respond to the notice may lead to the Seller initiating legal action.

- Utilizing this form can protect the Seller's rights in the event of a dispute over nonpayment.

Quick recap

- The Notice of Default is a crucial first step for Sellers facing payment issues.

- Clear communication of the default helps protect legal rights and obligations.

- Timely completion and delivery of the notice can prevent further complications.

Looking for another form?

Form popularity

FAQ

After the lender files the Notice of Default, you get 90 days to bring your past-due bill current. After the 90 days pass, the lender files a Notice of Sale with the clerk. The Notice of Sale displays the location, date and time of the sale. It lists the trustee's name and contact information.

How long does it take to foreclose a property in Virginia? Depending on the timing of the various required notices, it usually takes approximately 60-90 days to effectuate an uncontested non-judicial foreclosure.

In the first instance, if your deed is not recorded, there is nothing in the public record to stop the seller from conveying the property to another person.The second situation could happen if your seller fails to pay his or her debts and the seller's creditors file liens or judgments against your property.

Redeeming the Property Before the Sale One way to stop a foreclosure is by redeeming the property.Virginia law, however, doesn't provide a post-sale redemption period after a nonjudicial foreclosure.

Generally, after the court declares a foreclosure, the property will be auctioned off to the highest bidder. The borrower has two hundred forty (240) days from the date of the sale to redeem the property by paying the amount for which the property was sold, plus six (6) percent interest.

A notice of default is the first step to a bank or mortgage lender's foreclosure process.If the mortgage is not paid up to date, the lender will seize the home. A notice of default is also known as a reinstatement period, notice of public auction, or notice of foreclosure.

The notice of default doesn't affect your credit file, but when the account defaults this will be recorded.If the debt is regulated by the Consumer Credit Act, you must be sent a default notice warning letter and have time to act on it before the default is recorded on your credit file.

Redemption is a period after your home has already been sold at a foreclosure sale when you can still reclaim your home. You will need to pay the outstanding mortgage balance and all costs incurred during the foreclosure process. Many states have some type of redemption period.

In a foreclosure by judicial sale, the redemption period is six months from the date of the foreclosure decree, unless the court orders a shorter time. Redemption is also available before the sale takes place, even if the initial redemption period expired.