USLegal Guide on How to Stop Garnishment

Overview of this form

This guide provides essential information on how to stop garnishments of wages and bank accounts. It outlines the legal framework surrounding garnishments and presents actionable steps individuals can take to halt or reduce the garnishment process. This guide differs from other legal forms by offering clear advice on the motion to quash garnishments, including exploring alternatives like payment arrangements or bankruptcy considerations.

What’s included in this form

- Overview of garnishment laws and protections for employees.

- Definition and explanation of wage garnishment, including exemptions.

- Details on the process for stopping a garnishment, including motions and negotiations.

- Information on the legal implications of bankruptcy in relation to garnishments.

- Guidance on filing a Claim of Exemption in court.

When to use this form

This guide is useful when you find your wages or bank accounts are being garnished for debts. You may want to stop a garnishment due to financial hardship, an incorrect debt claim, or if you want to discuss alternative repayment options with your creditor.

Who this form is for

This guide is intended for:

- Individuals facing wage or bank account garnishment.

- Debtors who believe the garnishment is not valid.

- Individuals considering bankruptcy as a last resort to stop garnishments.

- Anyone seeking to understand their rights and options related to garnishments.

Completing this form step by step

- Identify and gather relevant documentation related to your income and debts.

- Contact the creditor to discuss possible negotiation options.

- If needed, prepare a motion to quash the garnishment, citing legal grounds.

- File the motion with the appropriate court and attend the hearing.

- If negotiations are successful, document any agreements in writing.

Notarization requirements for this form

Notarization is generally not required for this form. However, certain states or situations might demand it. You can complete notarization online through US Legal Forms, powered by Notarize, using a verified video call available anytime.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Typical mistakes to avoid

- Not verifying the validity of the debt before taking action.

- Failing to attend court hearings, resulting in a lack of defense against garnishment.

- Not obtaining documentation for any negotiated agreements.

- Overlooking state-specific laws that may provide additional protections.

Why complete this form online

- Convenience of accessing legal guidance from anywhere, anytime.

- Easy to download and fill out, ensuring you have the most up-to-date forms.

- Provides a clear structure for understanding rights and legal options.

Legal use & context

- This guide is not a substitute for legal advice but serves to inform about garnishment laws and rights.

- Understanding the process can lead to better outcomes when dealing with debtors and creditors.

- By filing the correct forms and attending hearings, debtors can effectively protect their rights.

What to keep in mind

- Know your rights regarding garnishment and any income exemptions.

- Consider negotiation or legal motion to stop unwarranted garnishments.

- Keep records of all communications and agreements with creditors.

Looking for another form?

Form popularity

FAQ

Include in your letter what steps you plan to take to address the default, such as making a reasonable effort at a payment plan. Mention any circumstances that have changed recently to make your ability to pay off the debt more likely. This conveys to the creditor your goodwill toward satisfying the debt.

There is no wage garnishment tax deduction that can automatically reduce your income tax if you have wages garnished. However, if your wages are being garnished to pay a tax-deductible expense, like medical debt, you may be able to deduct those payments.

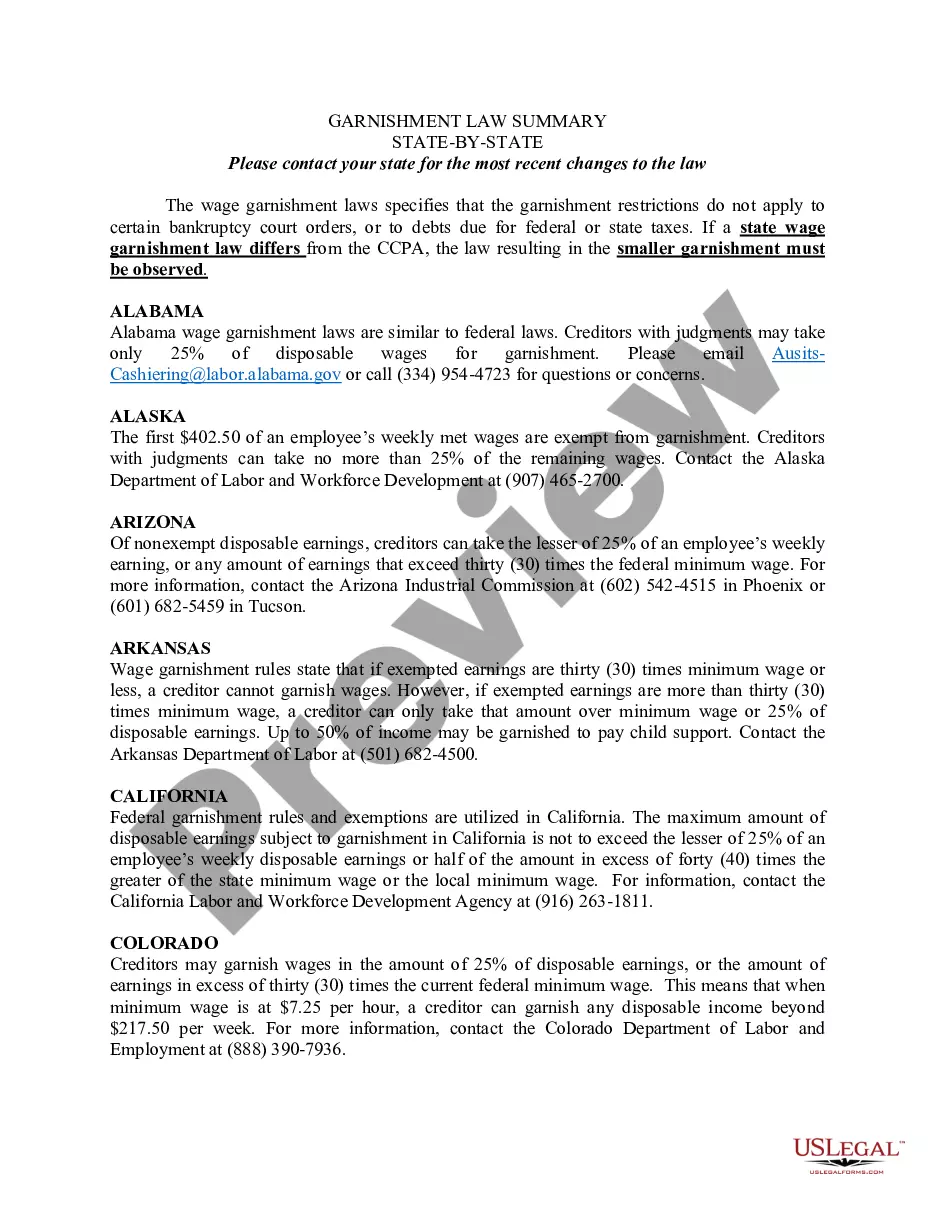

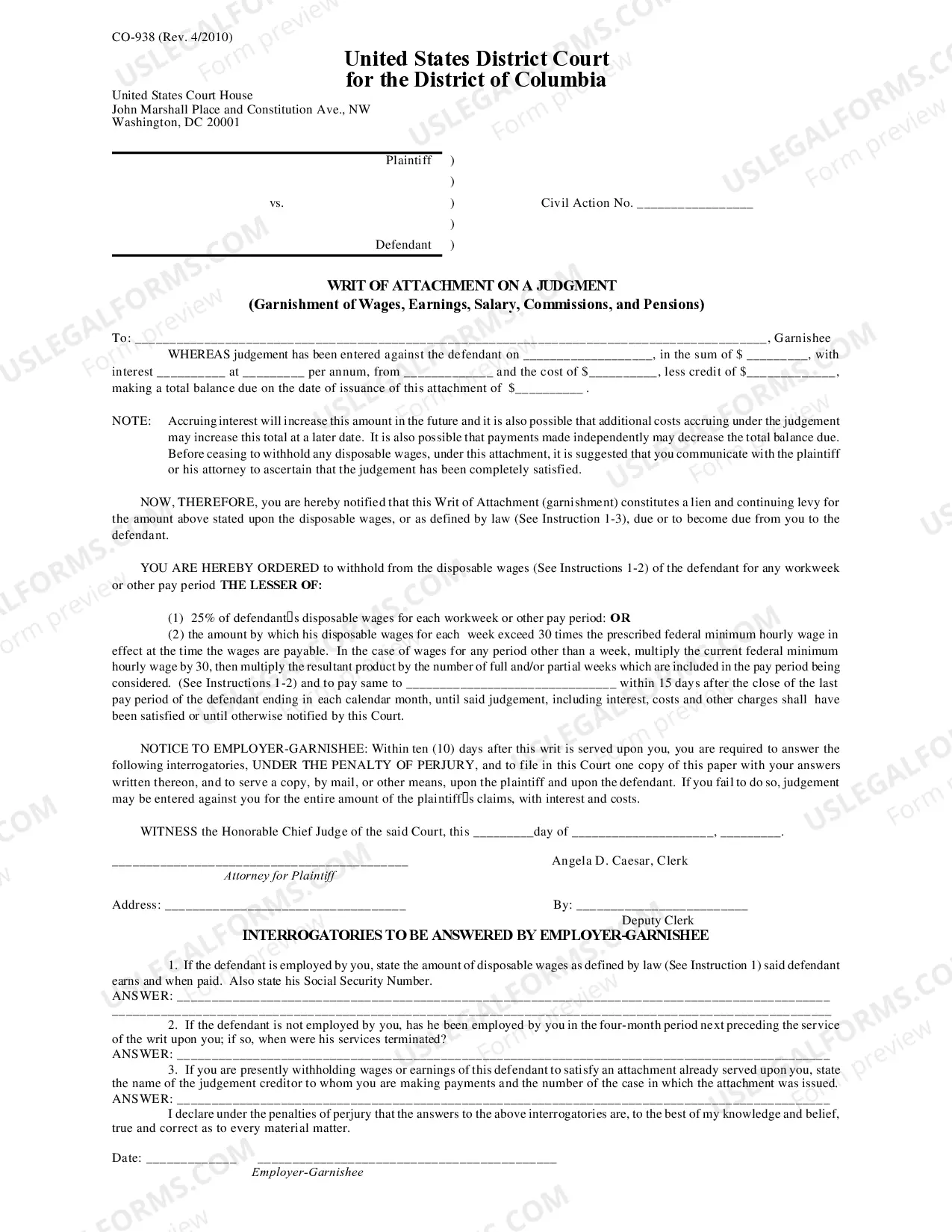

If you receive a notice of a wage garnishment order, you might be able to protect or exempt some or all of your wages by filing an exemption claim with the court. You can also stop most garnishments by filing for bankruptcy. Your state's exemption laws determine the amount of income you'll be able to keep.

In general terms, to attempt to have a wage garnishment ended, modified or reversed, you have the following options. First, you could attempt to negotiate a monthly payment agreement with the creditor/collector.Third, you could file an appeal with the court if you do not agree with the garnishment.

1) Quit Your Job Of course, when you learn that your creditors have won a garnishment order against you, you always have the option of quitting your job.As such, while quitting your job is certainly a legal option, you may do well to consider other recourse alternatives.

Pay off the debt completely. Set up an installment agreement. Negotiate with the IRS to pay less than you owe. Declare hardship. Declare bankruptcy. Get professional help.

Check to see if you're eligible to be garnished. object to the garnishment as a financial hardship; rehabilitate your student loans; lift the garnishment by making voluntary payments; or.

If it's already started, you can try to challenge the judgment or negotiate with the creditor. But, they're in the driver's seat, and if they don't allow you to stop a garnishment by agreeing to make voluntary payments, you can't really force them to. You can, however, stop the garnishment by filing a bankruptcy case.

Respond to the Creditor's Demand Letter. Seek State-Specific Remedies. Get Debt Counseling. Object to the Garnishment. Attend the Objection Hearing (and Negotiate if Necessary) Challenge the Underlying Judgment. Continue Negotiating.