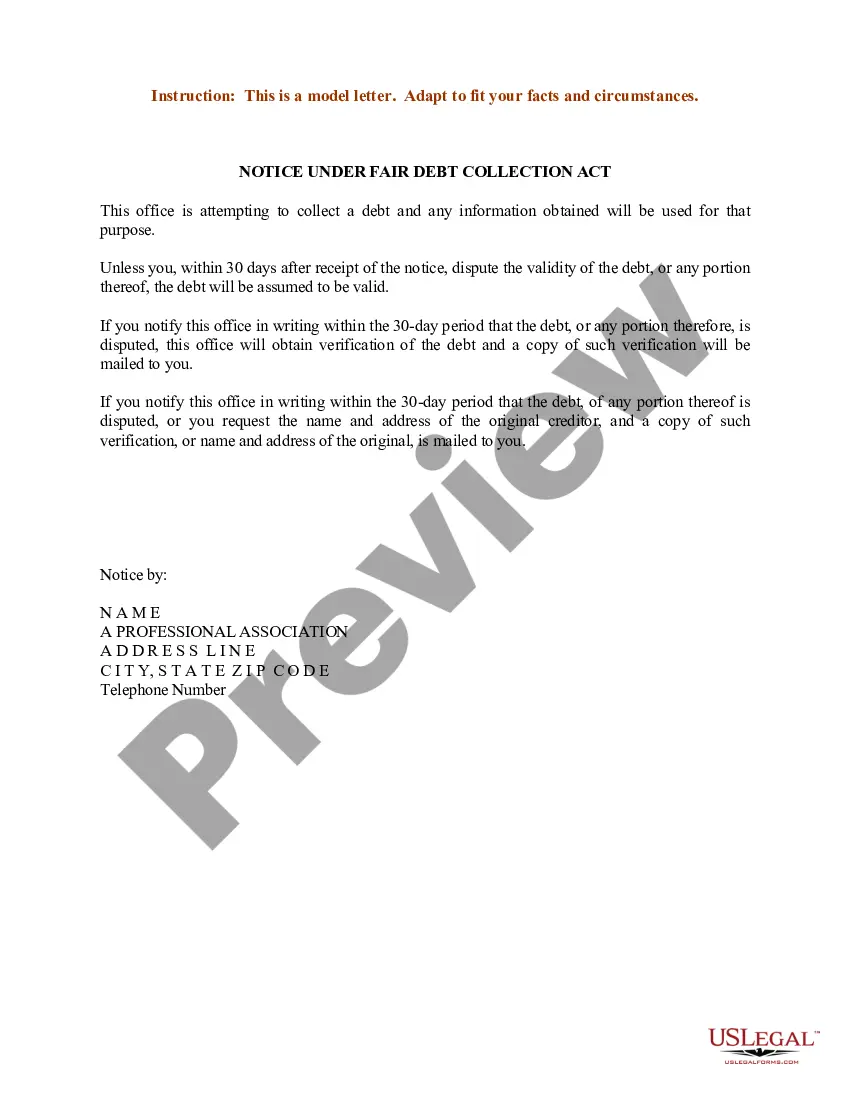

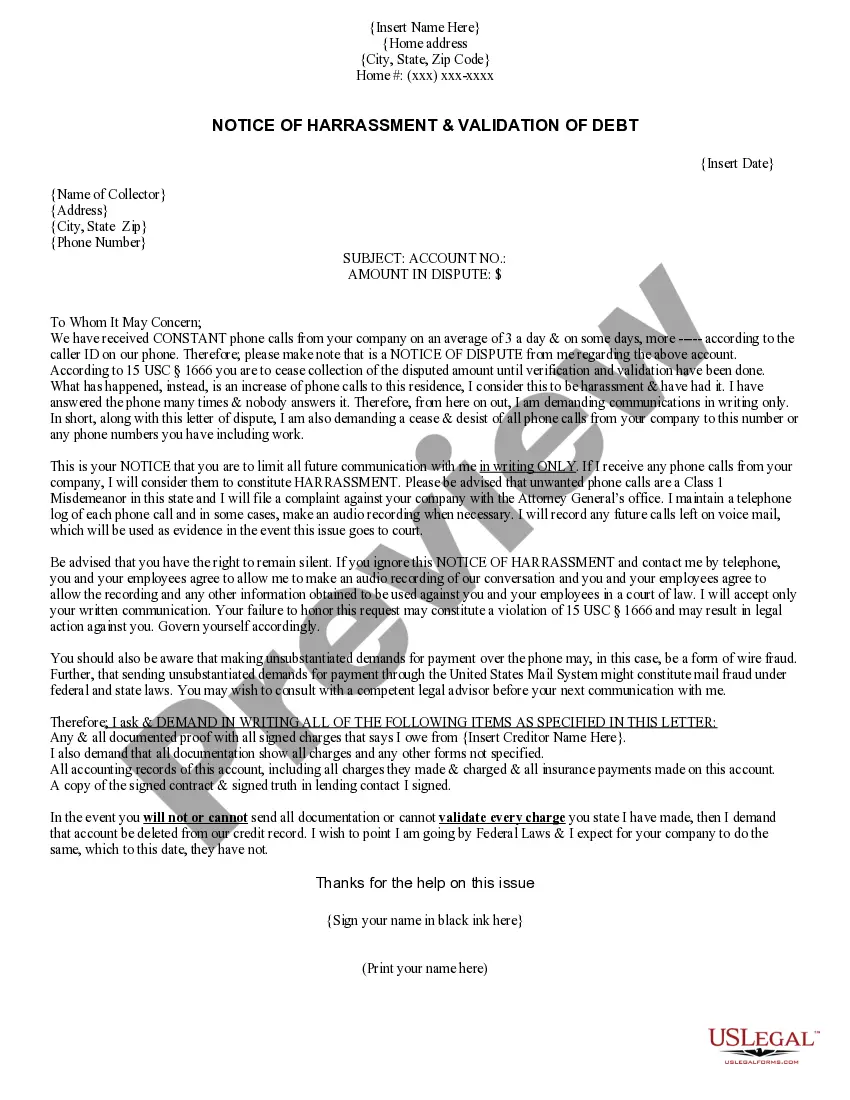

Notice to Debt Collector - Use of False Threats

Overview of this form

The Notice to Debt Collector - Use of False Threats is a legal document that informs a debt collector of their violations under the Fair Debt Collection Practices Act (FDCPA). By sending this notice, you make it clear that their misleading actions and threats are unacceptable. This form is critical for consumers who want to ensure their rights are protected when dealing with aggressive debt collection practices.

Key parts of this document

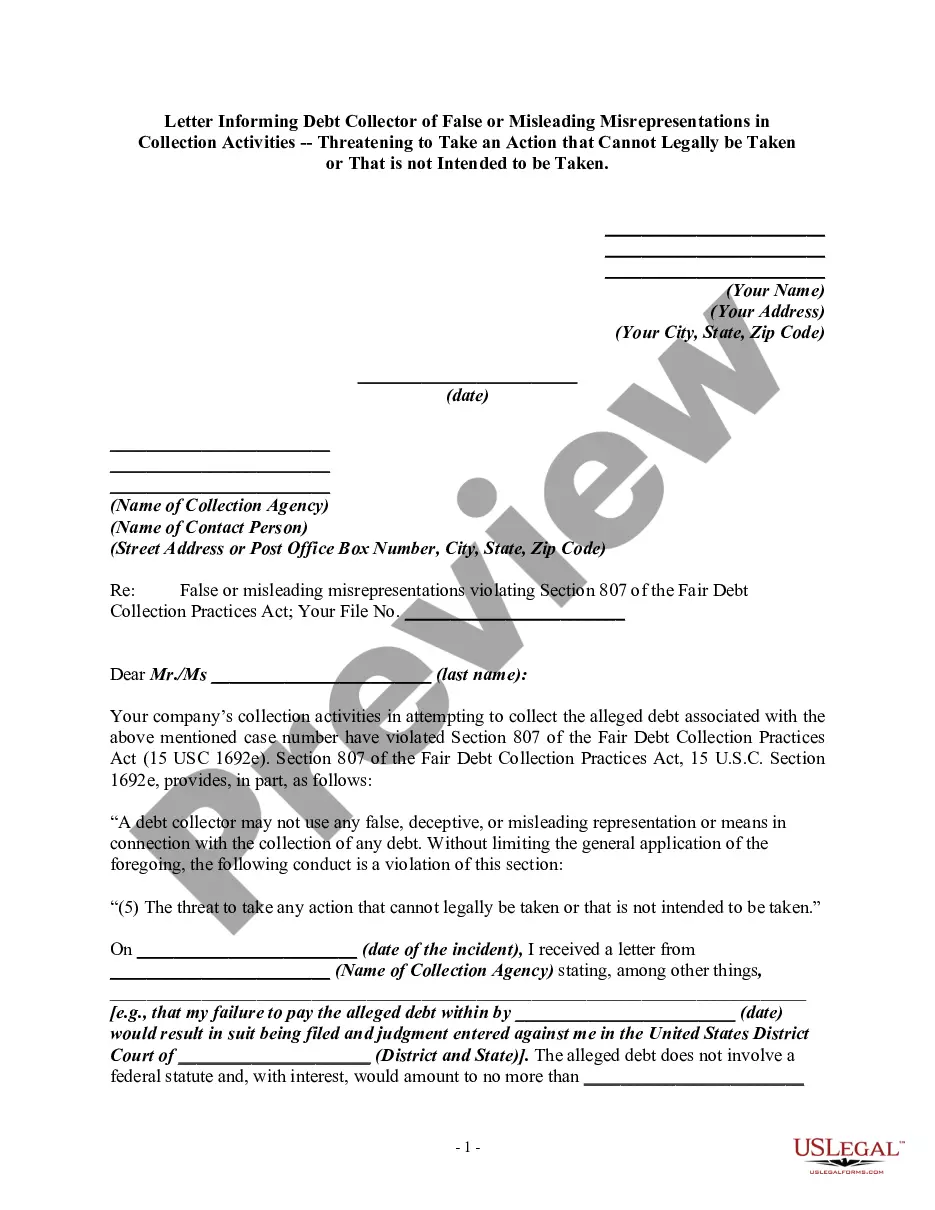

- Sender's contact information: Includes your name, address, and the date.

- Recipient's contact information: Includes the company name and the contact person.

- Case reference: A section to specify the associated case number.

- Description of the violation: Detail how the debt collector violated the FDCPA.

- Request for cessation: A statement requesting the debt collector to stop the harmful behavior.

- Signatures: Includes space for your signature and printed name to authenticate the notice.

Situations where this form applies

This form should be used if you have received communication from a debt collector that includes false threats or misleading information regarding your debt. Common scenarios include receiving a call where a collector claims they will take legal action against you without the intent or authority to do so or if they threaten to report your debt inaccurately.

Who this form is for

- Consumers who believe a debt collector has violated the FDCPA.

- Individuals seeking to protect their rights against abusive debt collection practices.

- Anyone who has experienced misleading threats from debt collectors.

How to prepare this document

- Identify your full name and address at the top of the form.

- Fill in the date you are sending the notice.

- Provide the debt collector's name and address accurately.

- Include the case number related to the alleged debt.

- Clearly describe the violation in your own words.

- Sign the letter to validate your notice.

Is notarization required?

This form usually doesn’t need to be notarized. However, local laws or specific transactions may require it. Our online notarization service, powered by Notarize, lets you complete it remotely through a secure video session, available 24/7.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Typical mistakes to avoid

- Failing to provide specific examples of the violations.

- Not keeping a copy of the notice for your records.

- Sending the notice without certified mail, which can limit proof of delivery.

Why complete this form online

- Convenience of filling out and downloading the form from home.

- Instant access to the correct legal wording to ensure compliance.

- Easy editing options if personal information or details change.

Legal use & context

- This form is a necessary step in addressing violations of the FDCPA.

- Using this form helps establish a record of the collector's misconduct.

- Consumers may leverage this notice in legal proceedings if violations continue.

Key takeaways

- This notice empowers you to assert your rights against misleading debt collection practices.

- Documenting the violation is essential for potential legal actions.

- Using this form can significantly encourage compliance from debt collectors.

Looking for another form?

Form popularity

FAQ

No. Debt collectors are prohibited from deceiving or misleading you while trying to collect a debt. Debt collectors are generally prohibited under federal law from using any false, deceptive, or misleading misrepresentation in collecting a debt.

If the debt holder still doesn't pay whomever is collecting the debt, the creditor can file a lawsuit against the debt holder in civil court. However, the creditor is less likely to do so if the balance owed is under $1,000, or if the debt is settled.

Under the FDCPA, a debt collector cannot threaten to sue you to force faster payment of a debt. More often than not, when a collection agent or lawyer threatens to sue, it is to frighten you into making larger payments or establishing an impractical and financially infeasible payment schedule.

Sue the Debt Collector in State Court The consumer may bring a lawsuit against the debt collector in state court. In the lawsuit, you must prove that the debt collector violated the FDCPA. If successful, you may be able to collect $1,000 in statutory damages, and possibly more if you suffered harm from the violations.

If you believe a debt collector is harassing you, you can submit a complaint with the CFPB online or by calling (855) 411-CFPB (2372). You can also contact your state's attorney general .

You may be able to sue a creditor or credit reporting agency if there is wrong information on your credit report that is not being removed.

Write a letter disputing the debt. You have 30 days after receiving a collection notice to dispute a debt in writing. Dispute the debt on your credit report. Lodge a complaint. Respond to a lawsuit. Hire an attorney.

You have the right to sue the collection agency if they act improperly for one year from the improper action. You can sue for lost wages and other expenses incurred, including legal and court costs. Also, the judge is allowed to award you up to $1,000 in punitive damages.

Debt collectors cannot harass or abuse you. They cannot swear, threaten to illegally harm you or your property, threaten you with illegal actions, or falsely threaten you with actions they do not intend to take. They also cannot make repeated calls over a short period to annoy or harass you.