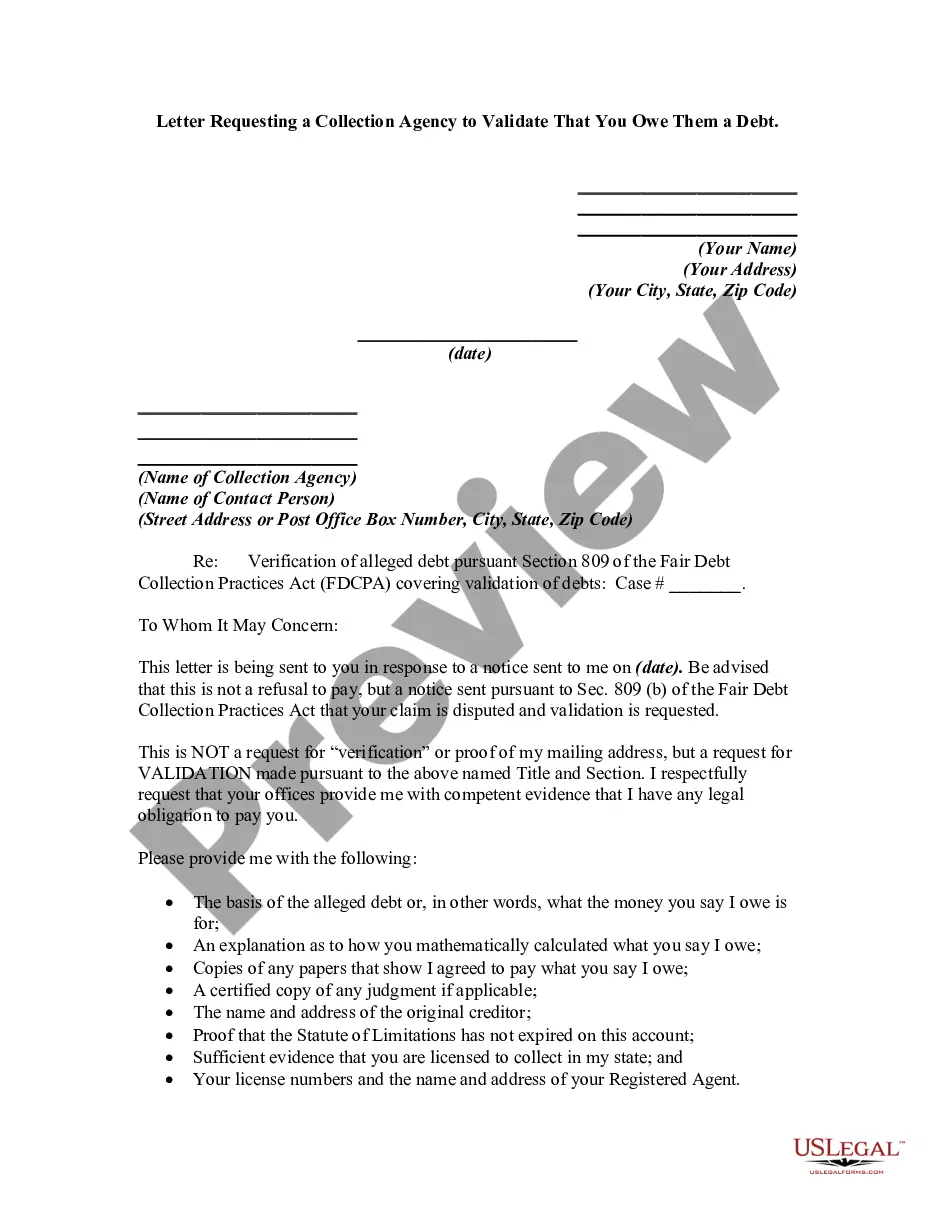

Letter Requesting a Collection Agency to Validate a Debt that You Allegedly Owe a Creditor

What this document covers

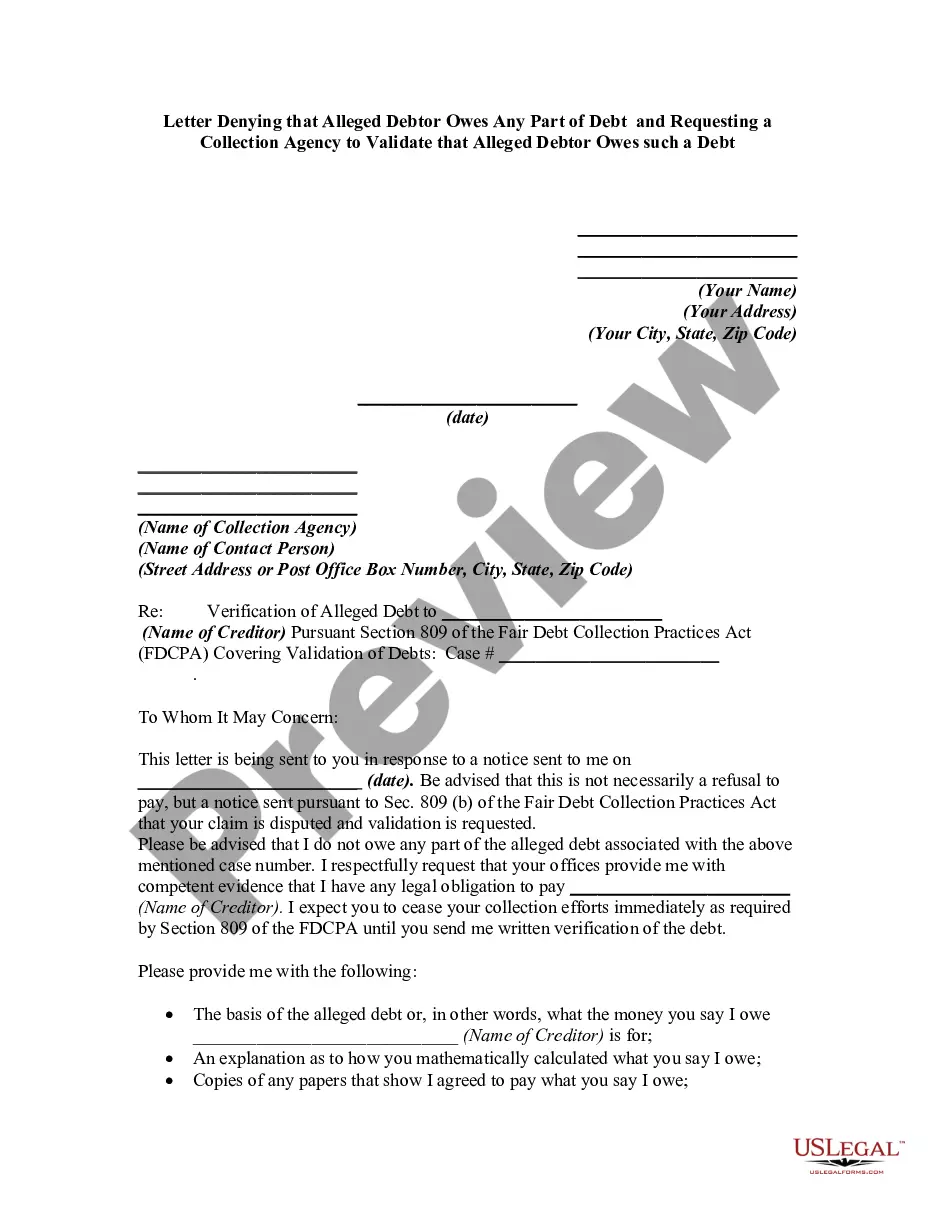

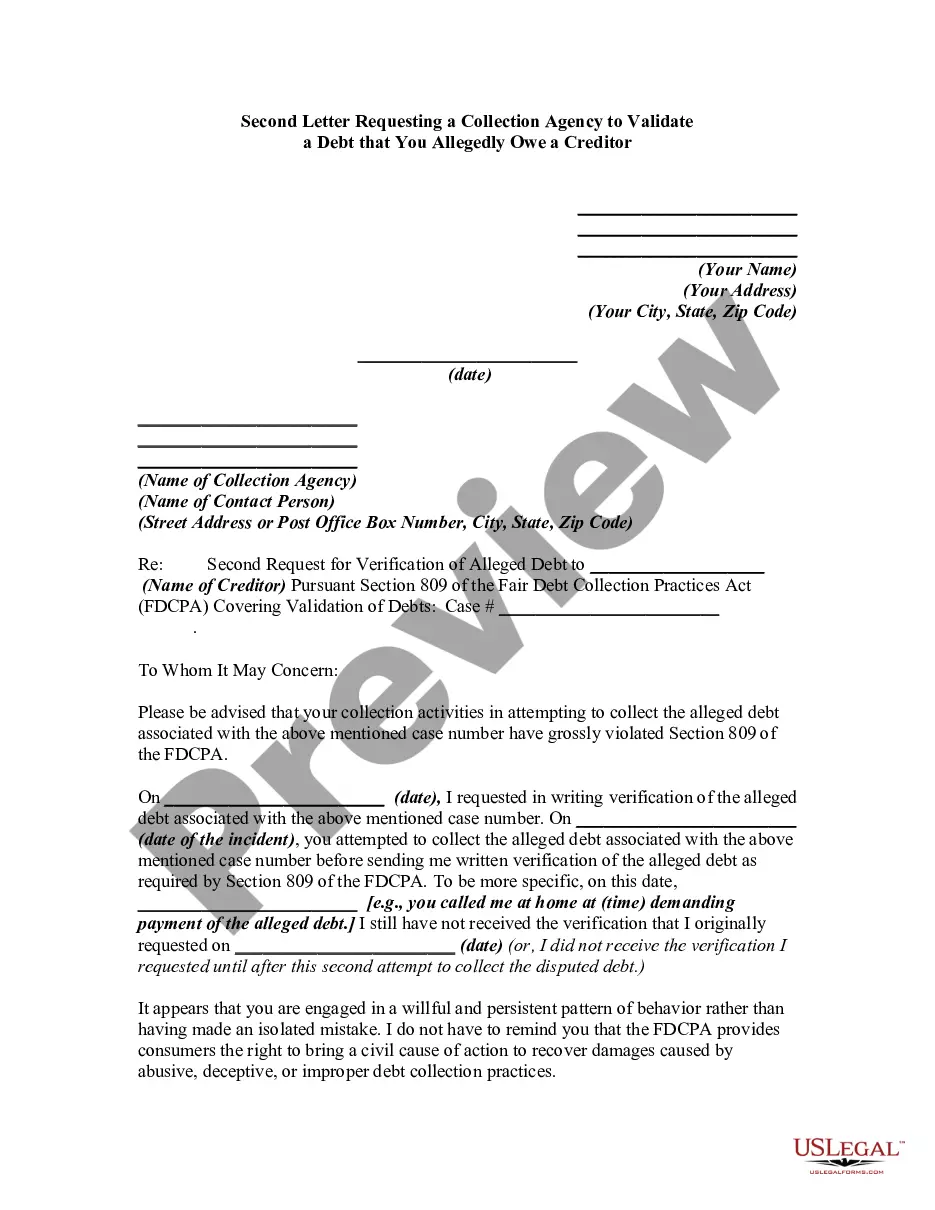

This form is a Letter Requesting a Collection Agency to Validate a Debt that You Allegedly Owe a Creditor. It serves as a formal communication to the collection agency, asking them to prove the legitimacy of the debt they claim you owe. This request is based on your rights under the Fair Debt Collection Practices Act (FDCPA), specifically Section 809, which allows you to dispute the validity of a debt.

Key parts of this document

- Your personal information, including name and address

- Date of the letter

- Details of the collection agency and contact person

- Specific request for validation of the alleged debt

- List of required documentation from the collection agency

- Statement regarding communication preferences and rights

When to use this document

Use this form when you receive a debt collection notice and you believe the debt is invalid or incorrect. It is particularly useful if you want the collection agency to provide proof of the debt's legitimacy before you take any further steps, such as making a payment or disputing the debt through other means.

Who can use this document

- Individuals who have been contacted by a debt collection agency

- Debtors who want to dispute the validity of a debt

- Those who wish to understand their rights under the FDCPA

- Anyone who wants to protect their credit report from inaccurate data

Instructions for completing this form

- Fill in your name and address at the top of the letter.

- Insert the date you are sending the letter.

- Provide details of the collection agency and the individual you are contacting.

- Clearly state the name of the creditor involved and the specific debt you are disputing.

- List the documentation you require from the agency for validation.

- Sign the letter and send it to the collection agency's address.

Notarization guidance

This form does not typically require notarization unless specified by local law. However, it is crucial to ensure that the letter is sent clearly and formally to prevent any issues with the collection agency.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Typical mistakes to avoid

- Failing to include all relevant personal information.

- Not specifying the debt or creditor in question.

- Omitting the request for specific documentation required for validation.

- Neglecting to sign and date the letter.

Why use this form online

- Convenient access to a template that can be easily customized.

- Professional drafting ensures legal validity and accuracy.

- Downloadable format allows for immediate use and printing.

Legal use & context

- This form is rooted in the Fair Debt Collection Practices Act, which protects consumers from unfair debt collection practices.

- Using this form properly shows that you are taking steps to ensure transparency in debt collection.

- It provides clear evidence of your dispute, which can be valuable in any legal matters that may arise.

Main things to remember

- This letter formally requests validation of a debt from a collection agency.

- It must be filled out accurately to protect your rights under the FDCPA.

- You should keep a record of all communications and documents sent.

- The form helps prevent possible inaccuracies on your credit report.

Looking for another form?

Form popularity

FAQ

In general, if you want to escalate the issue with the debt collector, you should do so within 30 days of receiving the validation letter. This includes disputing that you owe the debt, requesting additional verification of the debt, or requesting the name and address of the original creditor.

A debt validation letter can be an effective tool for dealing with debt collectors.

Debt collectors are legally required to send you a debt validation letter, which outlines what the debt is, how much you owe and other information. If you're still uncertain about the debt you're being asked to pay, you can send the debt collector a debt verification letter requesting more information.

Under the Fair Debt collection Practices Act (FDCPA), I have the right to request validation of the debt you say I owe you. I am requesting proof that I am indeed the party you are asking to pay this debt, and there is some contractual obligation that is binding on me to pay this debt.

Debt validation is your federal right granted under the Fair Debt Collection Practices Act (FDCPA). To request debt validation, you must send a written request to the debt collector within 30 days of being contacted by the collection agency.

The debt dispute letter should include your personal identifying information; verification of the amount of debt owed; the name of the creditor for the debt; and a request that the debt not be reported to credit reporting agencies until the matter is resolved or have it removed from the report, if it already has been

The FDCPA gives you a set period of time to dispute debts with collection agencies, but you can still request a debt validation after 30 days.

Debt validation is your federal right granted under the Fair Debt Collection Practices Act (FDCPA). To request debt validation, you must send a written request to the debt collector within 30 days of being contacted by the collection agency.

Ask the caller for their name, company, street address, telephone number, and if your state licenses debt collectors, a professional license number.