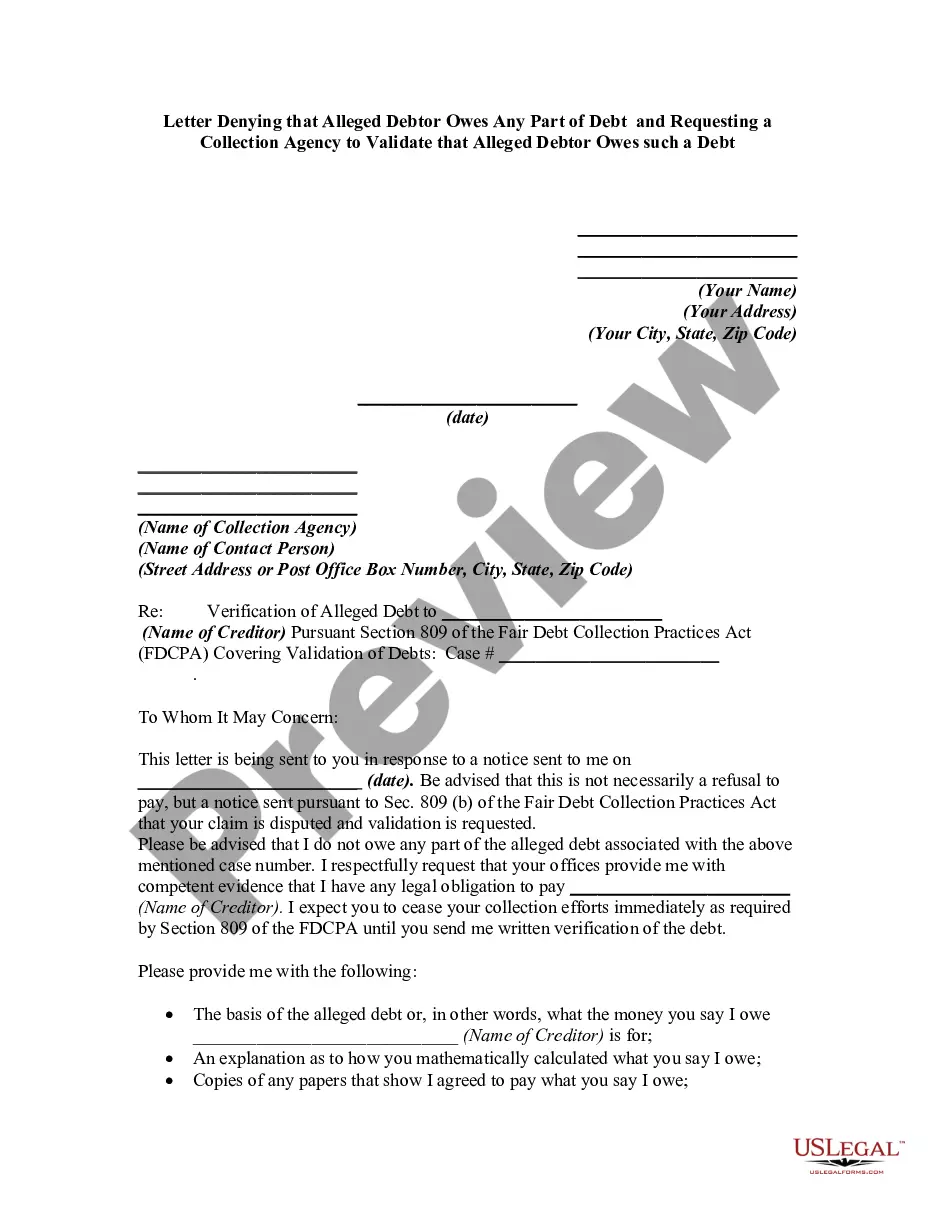

Second Letter Requesting a Collection Agency to Validate a Debt that You Allegedly Owe a Creditor

What is this form?

The Second Letter Requesting a Collection Agency to Validate a Debt that You Allegedly Owe a Creditor is a legal document designed for debtors to challenge the validity of debts claimed by collection agencies. This form serves as a follow-up communication, requiring the agency to provide verification that the debt is legitimate and actually owed. Unlike the initial request, this second letter emphasizes past violations of the Fair Debt Collection Practices Act (FDCPA) by the collection agency.

Key parts of this document

- Your details: Includes spaces to enter your name and address.

- Date: The date you are sending the letter.

- Agency details: Fields for the name of the collection agency and contact person.

- Case reference: Identification of the specific debt case related to the creditor.

- Verification request: A detailed request for the collection agency to verify the debt.

- Legal references: Cites the relevant section of the FDCPA and mentioned violations.

- Signature section: Provided for your printed name and signature, along with distribution to the creditor and appropriate state agency.

When to use this document

This form is useful when you have already requested verification of a debt from a collection agency but have not received a satisfactory response. If the agency has attempted to collect the alleged debt without providing the necessary documentation, using this second letter can help assert your rights under the FDCPA and demand compliance.

Intended users of this form

- Debtors who have received a debt collection notice from a collection agency.

- Individuals who previously requested debt validation but did not receive proper validation.

- Anyone needing to assert their rights under the Fair Debt Collection Practices Act.

How to complete this form

- Enter your personal information, including your name and address.

- Add the date when you are submitting the letter.

- Fill in the name of the collection agency and the contact person.

- Specify the creditor's name and related case number as referenced in previous communications.

- Detail the previous requests for verification and any collection attempts made by the agency.

- Sign the letter and distribute copies as indicated in the form.

Does this document require notarization?

This form does not typically require notarization to be legally valid. However, some jurisdictions or document types may still require it. US Legal Forms provides secure online notarization powered by Notarize, available 24/7 for added convenience.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Avoid these common issues

- Failing to include a specific case number, which may confuse the agency.

- Not providing a detailed description of previous communication attempts.

- Leaving the date blank, which may affect the validity of your claim.

- Forgetting to keep copies of the letter for your records.

Benefits of completing this form online

- Access to legally drafted templates created by licensed attorneys.

- Convenient online completion and immediate downloading for personal use.

- Editable fields that allow you to customize the form easily.

- Ensured compliance with legal requirements, reducing the risk of mistakes.

Legal use & context

- This form is designed for use under the Fair Debt Collection Practices Act.

- It provides you with a clear method to assert your rights against improper debt collection practices.

- Sending this letter may encourage compliance and proper verification from the collection agency.

Summary of main points

- This form is essential for challenging incorrect debt collections.

- Use it if previous requests for validation have gone unanswered.

- Maintain copies of all correspondence for your records and potential dispute.

Looking for another form?

Form popularity

FAQ

Debt collectors are legally required to send you a debt validation letter, which outlines what the debt is, how much you owe and other information. If you're still uncertain about the debt you're being asked to pay, you can send the debt collector a debt verification letter requesting more information.

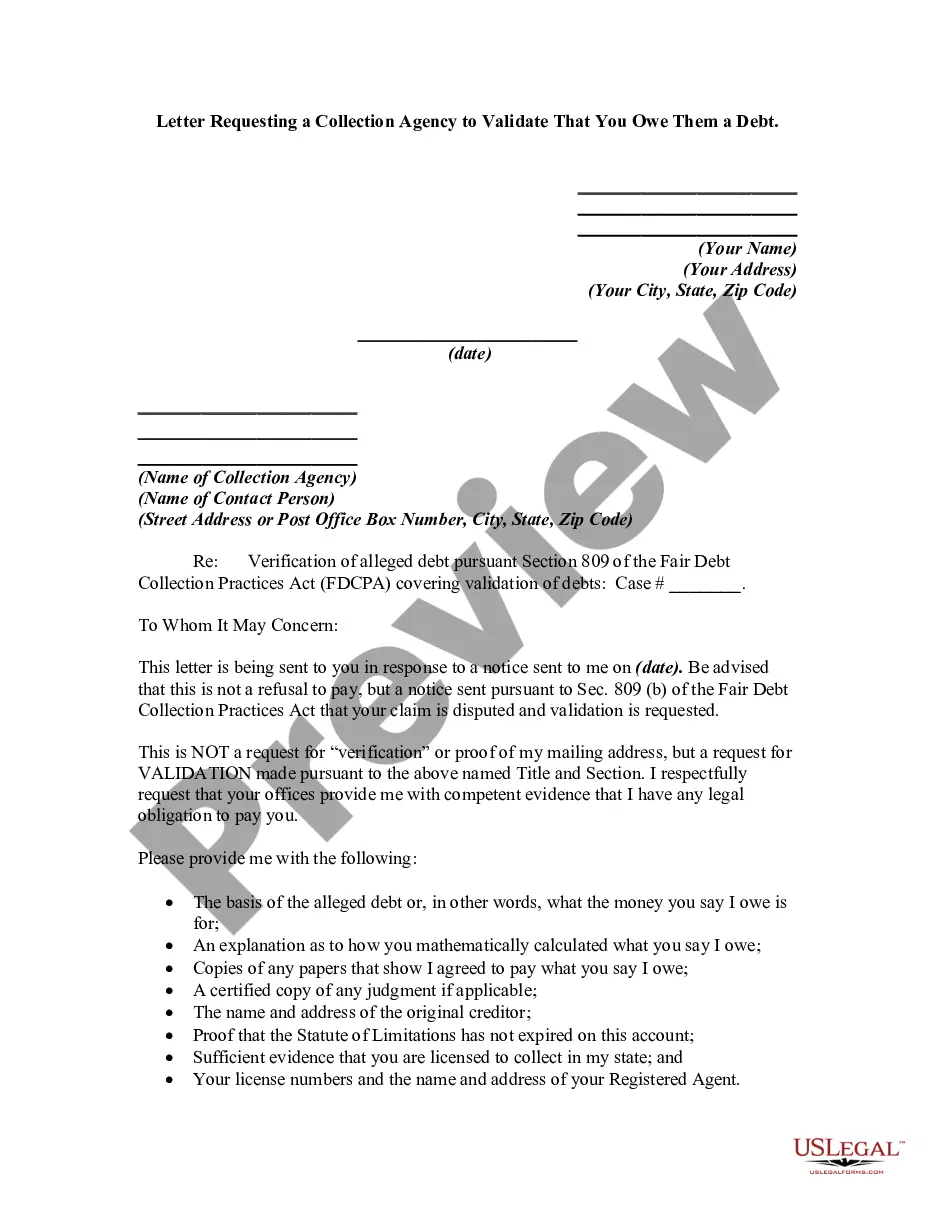

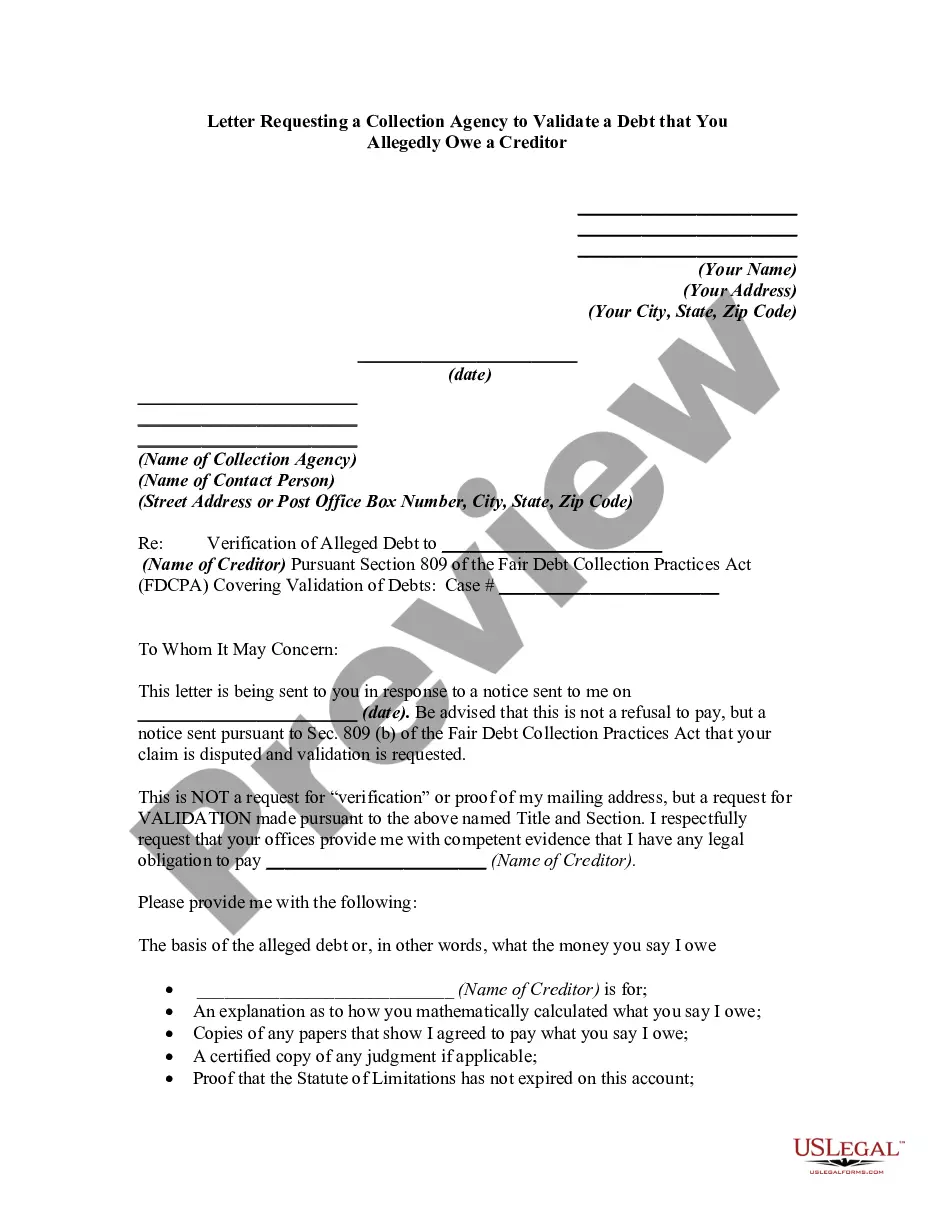

Your full name and address. The collections agency's name and address. A request for the amount of the debt claimed to be owed. A request for the name of the original creditor. A request for the judgment information (if applicable) A request for proof of the company's license.

If the collector completely fails to respond to the validation letter, again they have 30 days to do so, then legally they must cease collection efforts, and remove negative items placed by them on your credit report.

In general, if you want to escalate the issue with the debt collector, you should do so within 30 days of receiving the validation letter. This includes disputing that you owe the debt, requesting additional verification of the debt, or requesting the name and address of the original creditor.

A debt validation letter can be an effective tool for dealing with debt collectors.

The FDCPA gives you a set period of time to dispute debts with collection agencies, but you can still request a debt validation after 30 days.

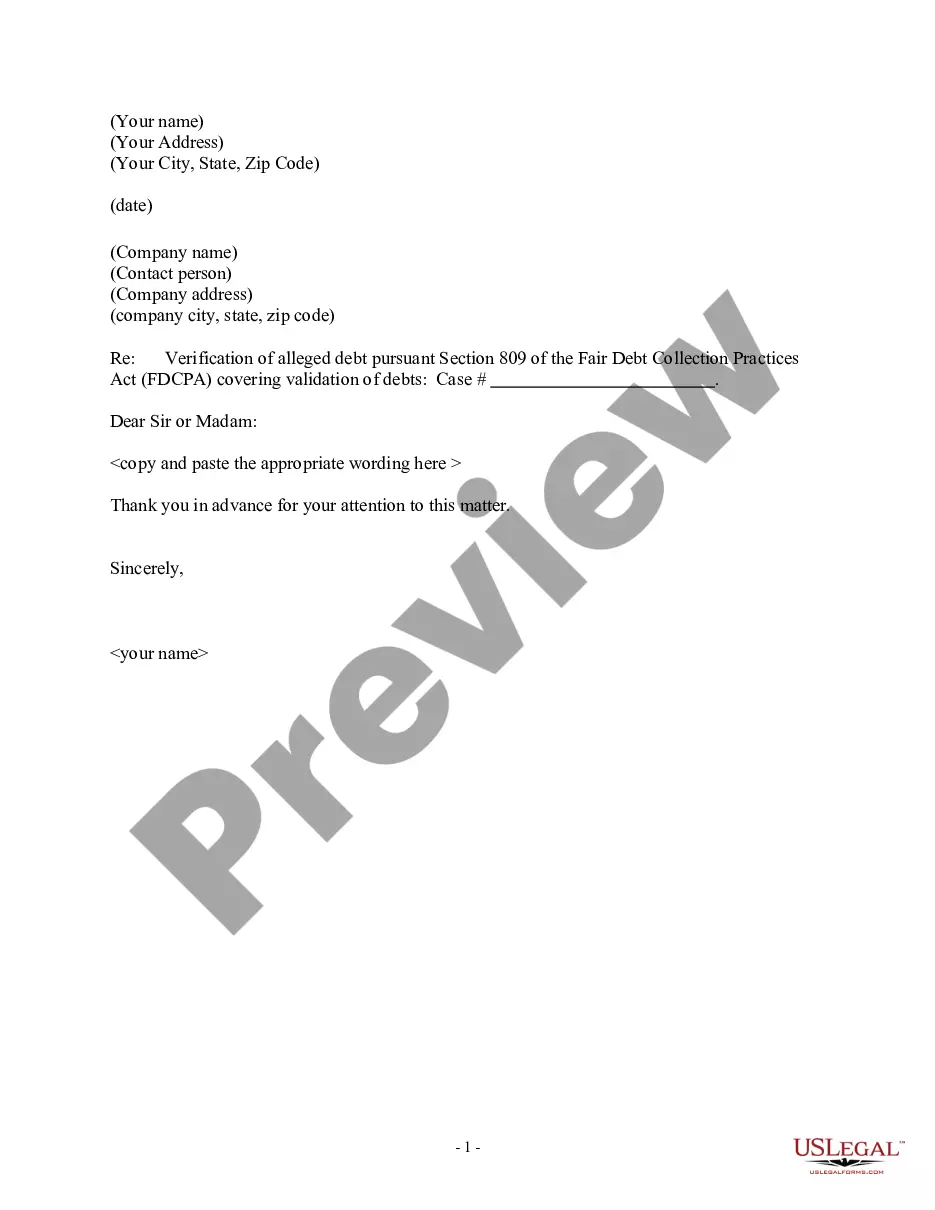

Debt validation is your federal right granted under the Fair Debt Collection Practices Act (FDCPA). To request debt validation, you must send a written request to the debt collector within 30 days of being contacted by the collection agency.

Debt validation is your federal right granted under the Fair Debt Collection Practices Act (FDCPA). To request debt validation, you must send a written request to the debt collector within 30 days of being contacted by the collection agency.

Under the Fair Debt collection Practices Act (FDCPA), I have the right to request validation of the debt you say I owe you. I am requesting proof that I am indeed the party you are asking to pay this debt, and there is some contractual obligation that is binding on me to pay this debt.