Individual Notice of Preexisting Condition Exclusion

Understanding this form

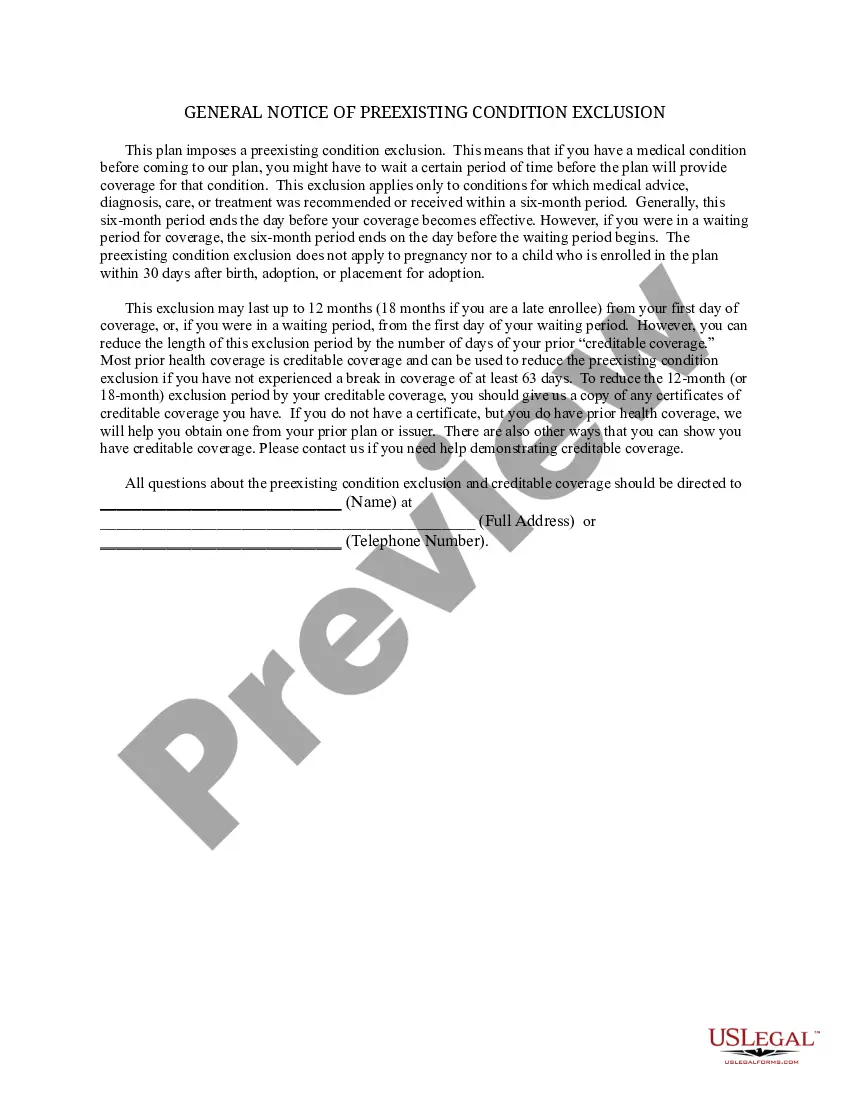

The Individual Notice of Preexisting Condition Exclusion is a legal document that informs you about any exclusions related to preexisting conditions under your group health plan. This form is crucial as it outlines how prior medical issues may affect your coverage and differs from general insurance policies by focusing specifically on preexisting conditions and their impact on eligibility for benefits.

Form components explained

- Identification of the individual and insurance provider.

- Details regarding preexisting condition exclusions.

- Duration of the exclusion period (in months, weeks, or days).

- Opportunities for the individual to submit evidence for reconsideration.

- Information on appeals and established procedures for disputing decisions.

When this form is needed

This form is utilized when an individual receives notice from their health insurance provider regarding exclusions for conditions that existed prior to the start of coverage. It is particularly relevant during the enrollment period when transitioning between plans or when a new employer's health plan is implemented.

Who this form is for

- Individuals enrolling in a group health plan who have preexisting conditions.

- Employees newly covered under an employer's health insurance plan.

- Late enrollees seeking clarification on their coverage exclusions.

Instructions for completing this form

- Enter the name and identification details of the individual and the insurance provider.

- Specify the preexisting conditions that are being excluded from coverage.

- Indicate the duration of the exclusion period and the final date it will apply.

- Provide any supporting evidence relating to previous insurance coverage.

- Complete the section for appealing the decision, if you believe it is unjust.

Does this form need to be notarized?

This form does not typically require notarization unless specified by local law. However, it's always best to consult your insurance provider for specific requirements pertaining to your case.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Avoid these common issues

- Failing to provide accurate dates for the preexisting condition period.

- Neglecting to include supporting documentation of previous coverage.

- Not adhering to the appeal procedures outlined in the form.

Benefits of completing this form online

- Instant access to a legally compliant template designed by licensed attorneys.

- The ability to fill out and edit the form easily and save time.

- Secure handling of sensitive information with integrated compliance measures.

- The Individual Notice of Preexisting Condition Exclusion provides crucial details on how prior health issues may affect your insurance coverage.

- Filling this form accurately ensures you understand your rights and obligations regarding health insurance exclusions.

- Always check for state-specific regulations that may impact the terms of your health coverage.

Looking for another form?

Form popularity

FAQ

No, pre-existing diseases need to be declared while buying health insurance because your policy is underwritten based on your health declaration. In case the same is not disclosed, we reserve the right to cancel the policy on grounds of misrepresentation. Furthermore, we shall not be liable for claims if any.

Yes. Under the Affordable Care Act, health insurance companies can't refuse to cover you or charge you more just because you have a pre-existing condition that is, a health problem you had before the date that new health coverage starts.

Under current law, health insurance companies can't refuse to cover you or charge you more just because you have a pre-existing condition that is, a health problem you had before the date that new health coverage starts.

Health insurers can no longer charge more or deny coverage to you or your child because of a pre-existing health condition like asthma, diabetes, or cancer. They cannot limit benefits for that condition either. Once you have insurance, they can't refuse to cover treatment for your pre-existing condition.

HIPAA (Health Insurance Portability and Accountability Act) protects you if you have a pre-existing condition in several ways.The new group plan can, however, exclude you from coverage for that particular pre-existing condition for up to 12 months. This is a compromise that HIPAA brought about.

Insurers then use your permission to snoop through old records to look for anything that they might be able to use against you. If you have a pre-existing condition, they'll try to deny your claim on the grounds that you were already injured and their insured had nothing to do with it.

Under current law, health insurance companies can't refuse to cover you or charge you more just because you have a pre-existing condition that is, a health problem you had before the date that new health coverage starts.

Conditions for Exclusion HIPAA allows insurers to refuse to cover pre-existing medical conditions for up to the first twelve months after enrollment, or eighteen months in the case of late enrollment.