Jury Instruction - Failure To File Tax Return

Overview of this form

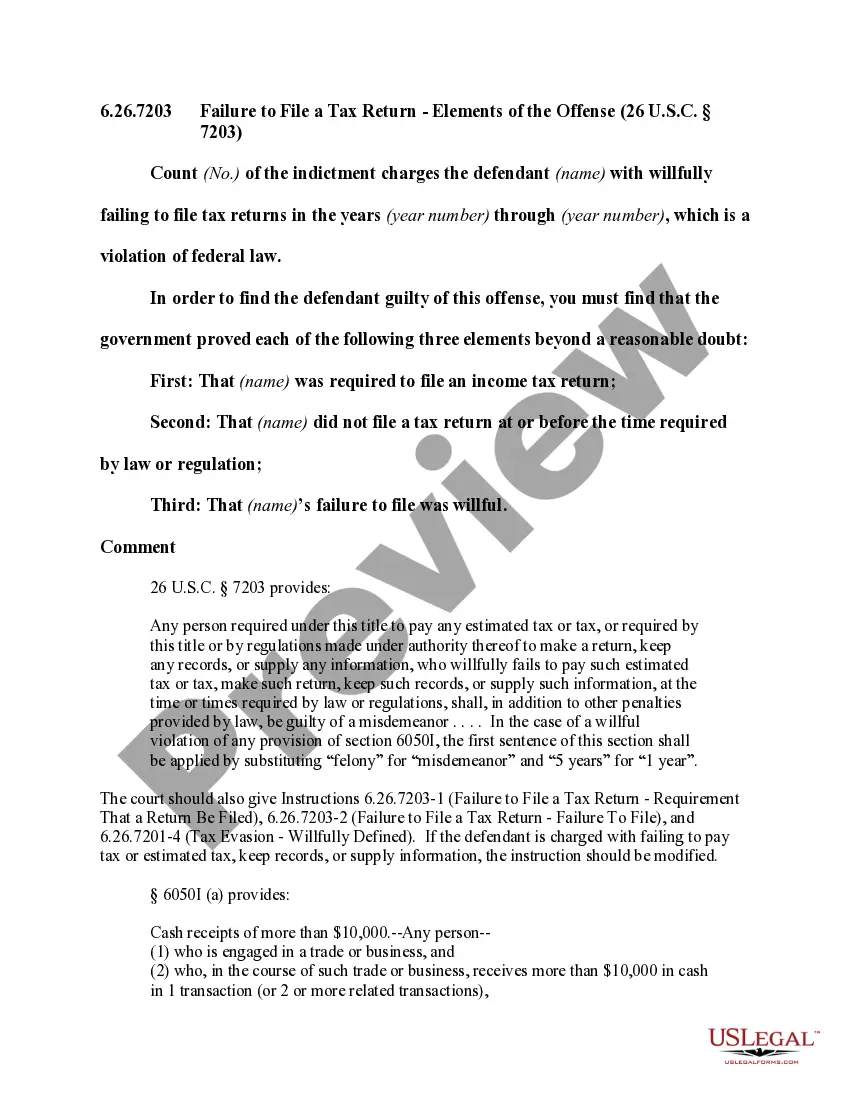

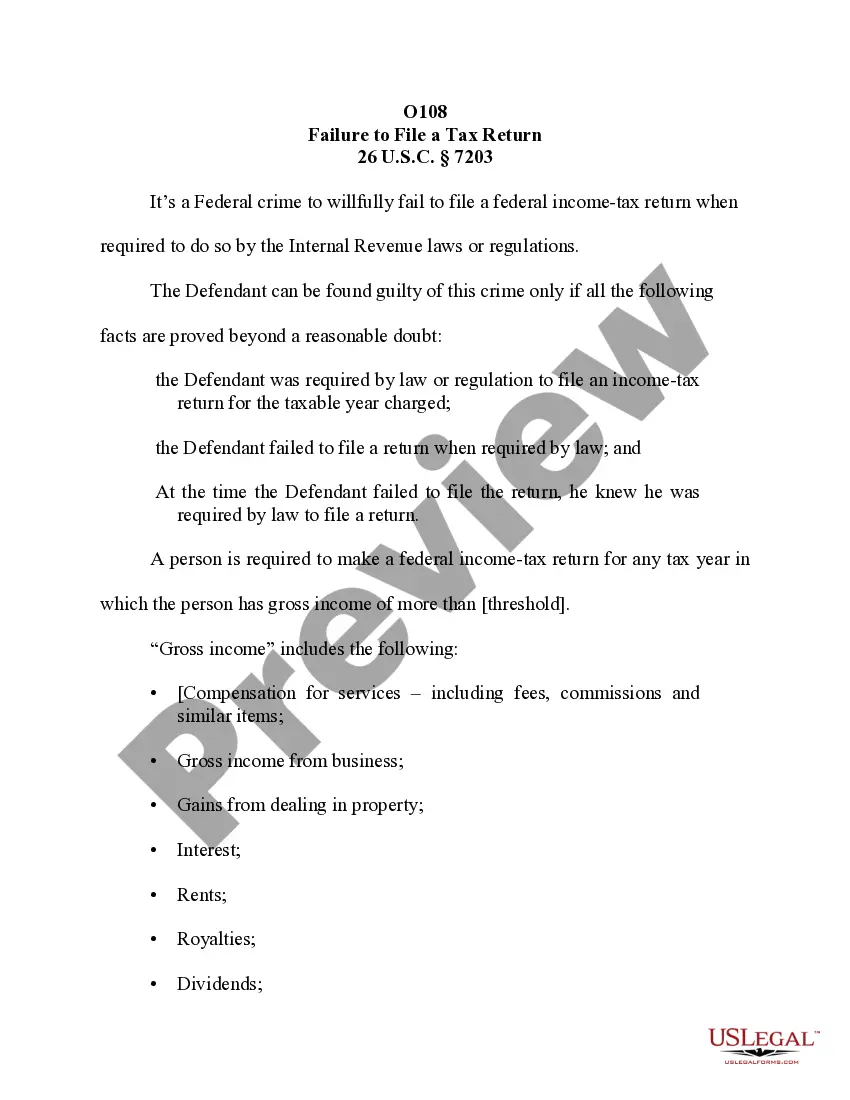

This Jury Instruction - Failure to File Tax Return form provides sample jury instructions that outline the legal standards for determining whether a defendant willfully failed to file a federal income tax return. Unlike other legal forms, this document is specifically designed to guide juries in understanding the criteria that must be proven for a conviction under Section 7203 of Title 26 of the United States Code.

Main sections of this form

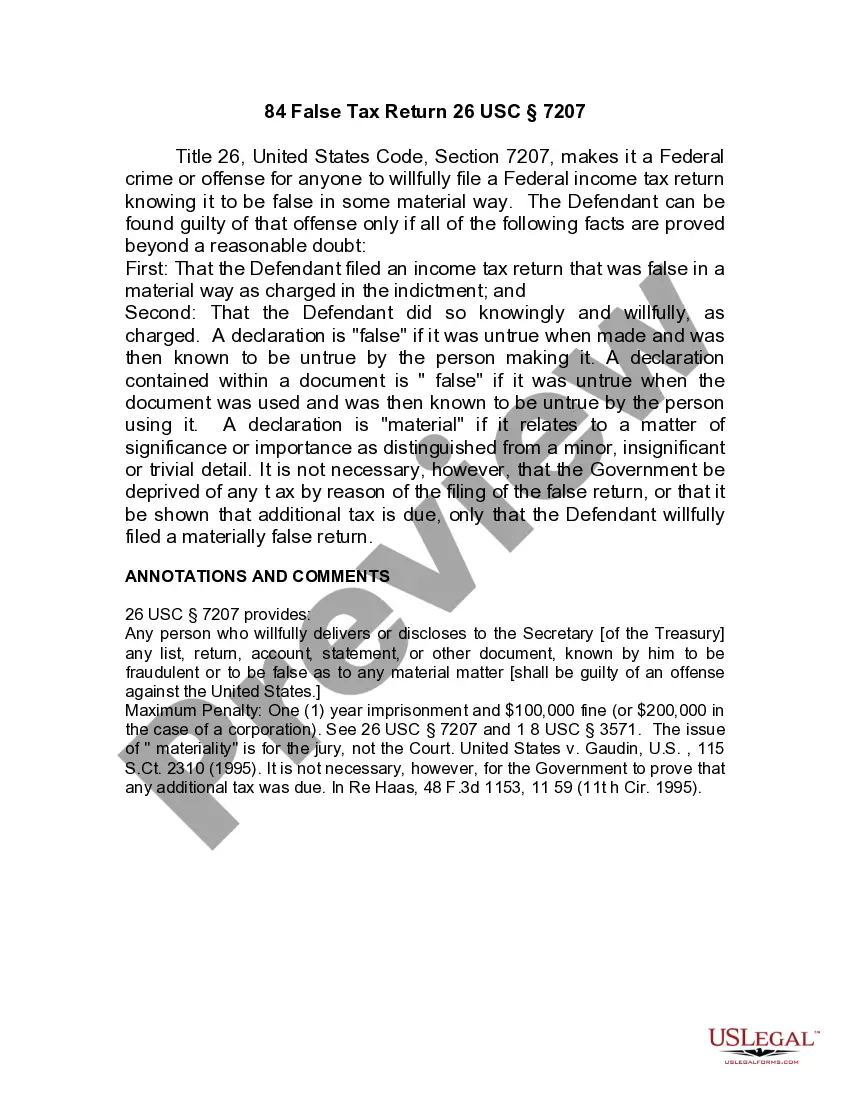

- Detailed definition of the crime of failure to file a tax return.

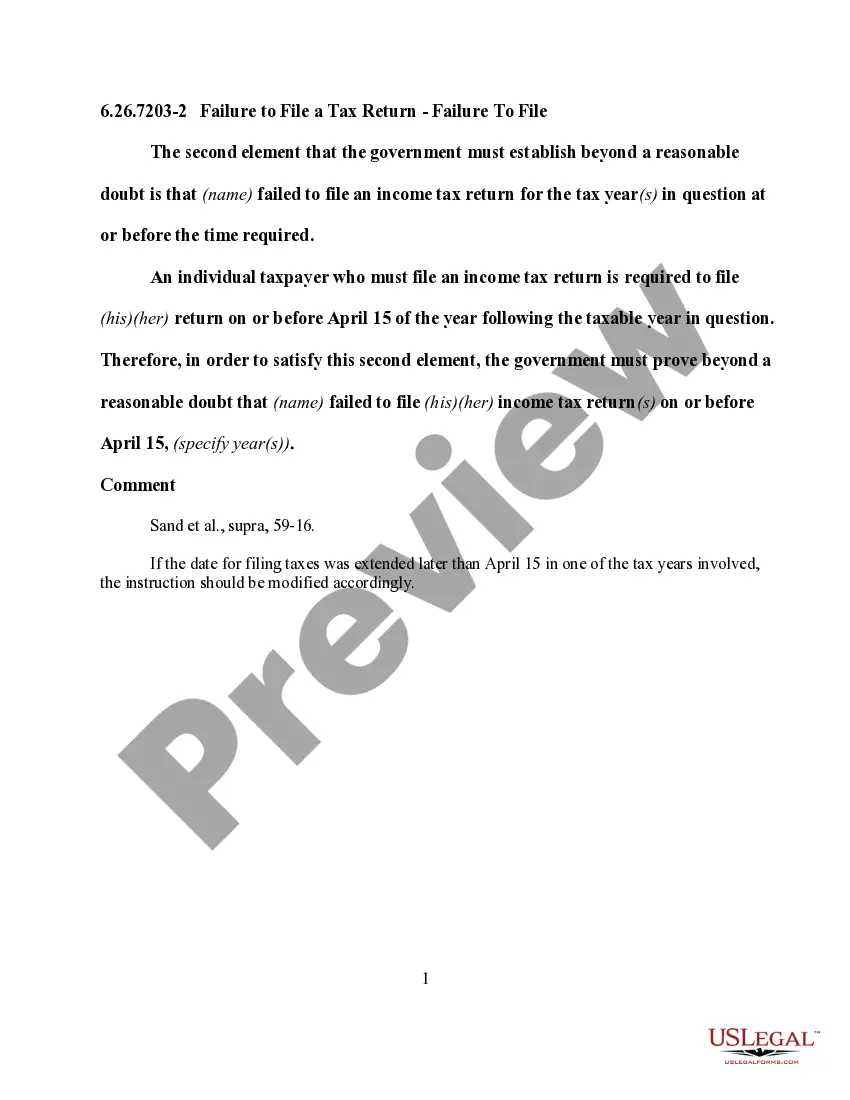

- Criteria that must be proven beyond a reasonable doubt: the requirement to file, the failure to file, and willfulness of the failure.

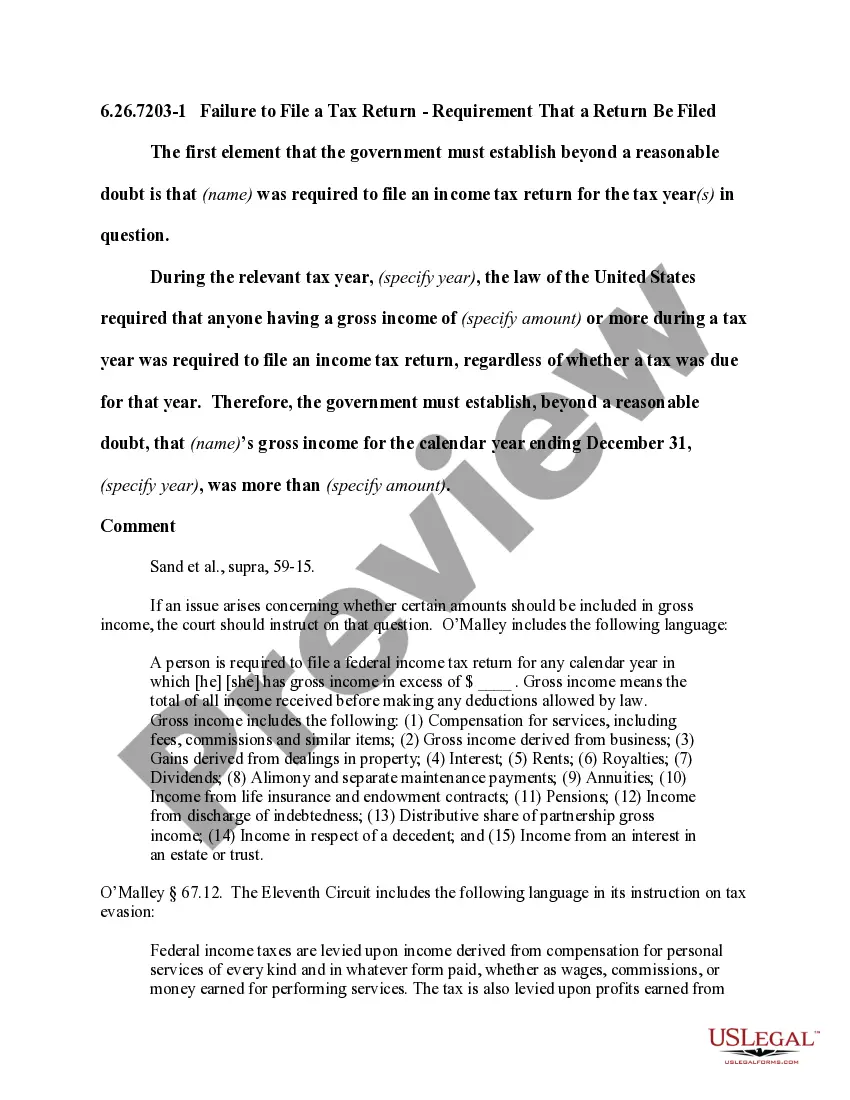

- Clarification of what constitutes gross income for filing requirements.

- Legal references to Title 26 USC Section 7203, including penalties.

When this form is needed

This form is necessary when preparing a jury for a trial involving allegations of willful failure to file a federal income tax return. It helps legal professionals present a clear framework regarding the prosecution's burden of proof and the essential elements that must be established to support a conviction.

Who needs this form

- Judges in federal tax-related cases.

- Prosecutors handling criminal tax cases.

- Defense attorneys representing individuals accused of tax-related offenses.

- Legal scholars studying tax law and jury instructions.

How to complete this form

- Read the statutory language of 26 USC Section 7203 carefully.

- Assess if the defendant was required to file a return based on their gross income.

- Determine if the defendant failed to file the return by the required deadline.

- Evaluate whether the failure to file was willful, considering the evidence presented.

- Present the jury instructions clearly to the jury before deliberations.

Does this form need to be notarized?

This form does not typically require notarization unless specified by local law. It is primarily intended for instructional use in court proceedings, rather than a standalone legal document that requires a signature.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Typical mistakes to avoid

- Failing to establish that the defendant's failure to file was willful.

- Not providing sufficient evidence of the defendant's gross income exceeding the filing threshold.

- Misinterpreting the statute requirements in jury instructions.

Benefits of completing this form online

- Convenience of downloading and completing the form at your own pace.

- Templates designed by licensed attorneys ensure accuracy and legal compliance.

- Easy access to revisions and modifications as needed for specific cases.

Legal use & context

- This form is key in federal criminal trials involving tax offenses, providing a structured framework for jury instruction.

- Understanding jurors' obligations can aid in fair decision-making processes.

- This document must be adapted to suit the specifics of each case and comply with any jurisdictional nuances.

Looking for another form?

Form popularity

FAQ

Will The IRS Catch It If I Have Made A Mistake? The IRS will most likely catch a mistake made on a tax return. The IRS has substantial computer technology and programs that cross-references tax returns against data received from other sources, such as employers.

Penalty for Tax Evasion in CaliforniaTax evasion in California is punishable by up to one year in county jail or state prison, as well as fines of up to $20,000. The state can also require you to pay your back taxes, and it will place a lien on your property as a security until you pay.

Line 12a reports the total amount of the distribution and line 12b reports the taxable portion, if any. Next to line 12b, write "rollover." If you're rolling the money from one tax-deferred account to another, such as from a 401(k) to another 401(k) or traditional IRA, the entire rollover is tax-free.

Tax evasion is an illegal activity in which a person or entity deliberately avoids paying a true tax liability. Those caught evading taxes are generally subject to criminal charges and substantial penalties. To willfully fail to pay taxes is a federal offense under the Internal Revenue Service (IRS) tax code.

Usually, tax evasion cases on legal-source income start with an audit of the filed tax return. In the audit, the IRS finds errors that the taxpayer knowingly and willingly committed.The IRS calls these behaviors badges of fraud. They're hot buttons that indicate tax evasion.

It is believed that the IRS can track such information as medical records, credit card transactions, and other electronic information and that it is using this added data to find tax cheats.

Failing to file a tax return can be classified as a federal crime punishable as a misdemeanor or a felony. Willful failure to file a tax return is a misdemeanor pursuant to IRC 7203.If you are charged with a criminal tax violation, the punishment can be severe and may include fines and jail time.

The basic rule for the IRS' ability to look back into the past and conduct a tax audit is that the agency has three years from your filing date to audit your tax filing for that year. However, taxpayers who fail to include all sources of their income may face a longer time period.

Unreported income: If you fail to report income the IRS will catch this through their matching process. It is required that third parties report taxpayer income to the IRS, such as employers, banks and brokerage firms.