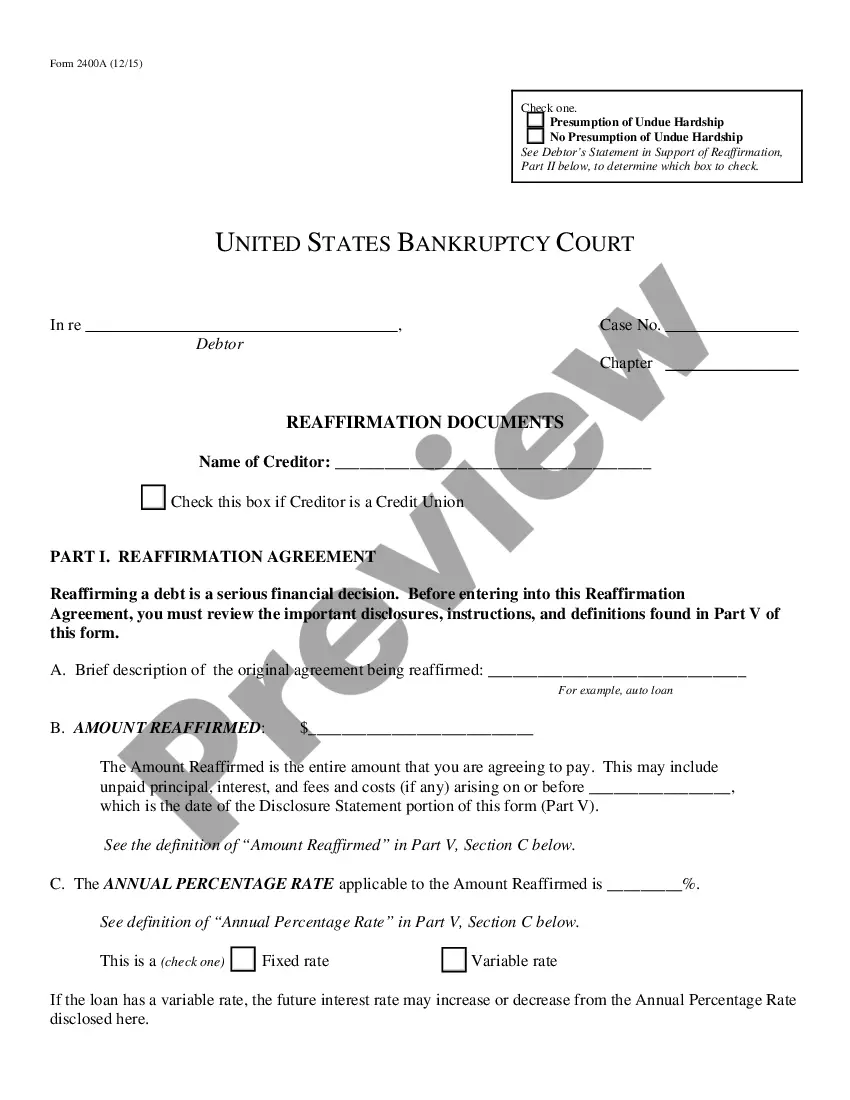

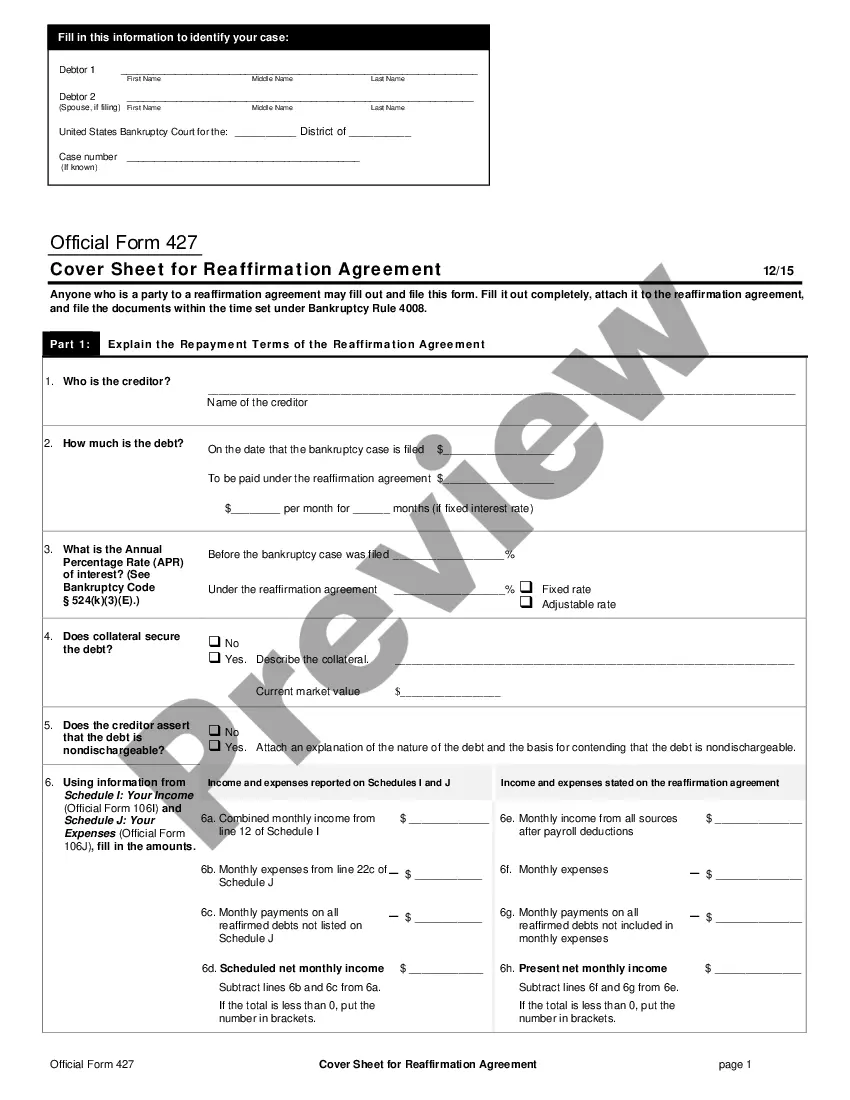

A Reaffirmation Agreement is a legally binding contract that reaffirms a debtor's responsibility for a specific debt such as a mortgage, car loan, or credit card debt. By signing a Reaffirmation Agreement, the debtor agrees to continue making payments on the debt and acknowledges that the debt is still owed and that the creditor can take action to collect the debt, such as filing a lawsuit to obtain a judgment. There are two types of Reaffirmation Agreement: voluntary and court-ordered. A voluntary Reaffirmation Agreement is a contract that the debtor and creditor enter into on their own terms. A court-ordered Reaffirmation Agreement is a contract that is ordered by the court in a bankruptcy proceeding.

Reaffirmation Agreement

Category:

State:

Multi-State

Control #:

US-B-2400AB-ALT

Format:

PDF

Instant download

This website is not affiliated with any governmental entity

Public form

Description

Reaffirmation Agreement

Free preview

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Built-in online Word editor

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Export easily

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

E-sign your document

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

Notarize online 24/7

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

Store your document securely

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

Reaffirmation Agreement: Key Concepts & Definitions

Reaffirmation Agreement refers to a legal document concluded between a creditor and the debtor in which the debtor agrees to continue paying a dischargeable debt after bankruptcy. This agreement is often used in the context of real estate and personal property that the debtor wishes to retain. A reaffirmation agreement ensures the continuation of the payment obligation in return for retaining ownership of the property.

- Real Estate: In the context of reaffirmation agreements, this refers to properties like homes or land that the debtor opts to keep by continuing to pay the corresponding debt.

- Reaffirming Debt: The process of committing to continue paying a debt that could otherwise be discharged in bankruptcy.

- Agreement Creditor: The creditor involved in a reaffirmation agreement, usually the original lender or debt holder.

- Official Form: Reaffirmation agreements are often formalized through legal documents specified by bankruptcy courts, principally the B240A form.

Step-by-Step Guide on Completing a Reaffirmation Agreement

- Assess the Situation: Determine if reaffirming the debt is in your financial interest. This often involves evaluating whether you can handle future payments without financial hardship.

- Discuss with Creditor: Negotiate the terms of the agreement with your creditor. Its crucial to secure terms that are manageable for you.

- Complete the Official Form: Fill out the required form provided by the court, typically the 'Reaffirmation Agreement Form' or B240A.

- Obtain Counsel: It is advisable to consult with a bankruptcy attorney before signing any reaffirmation agreement to ensure the terms are fair and do not lead to financial strain.

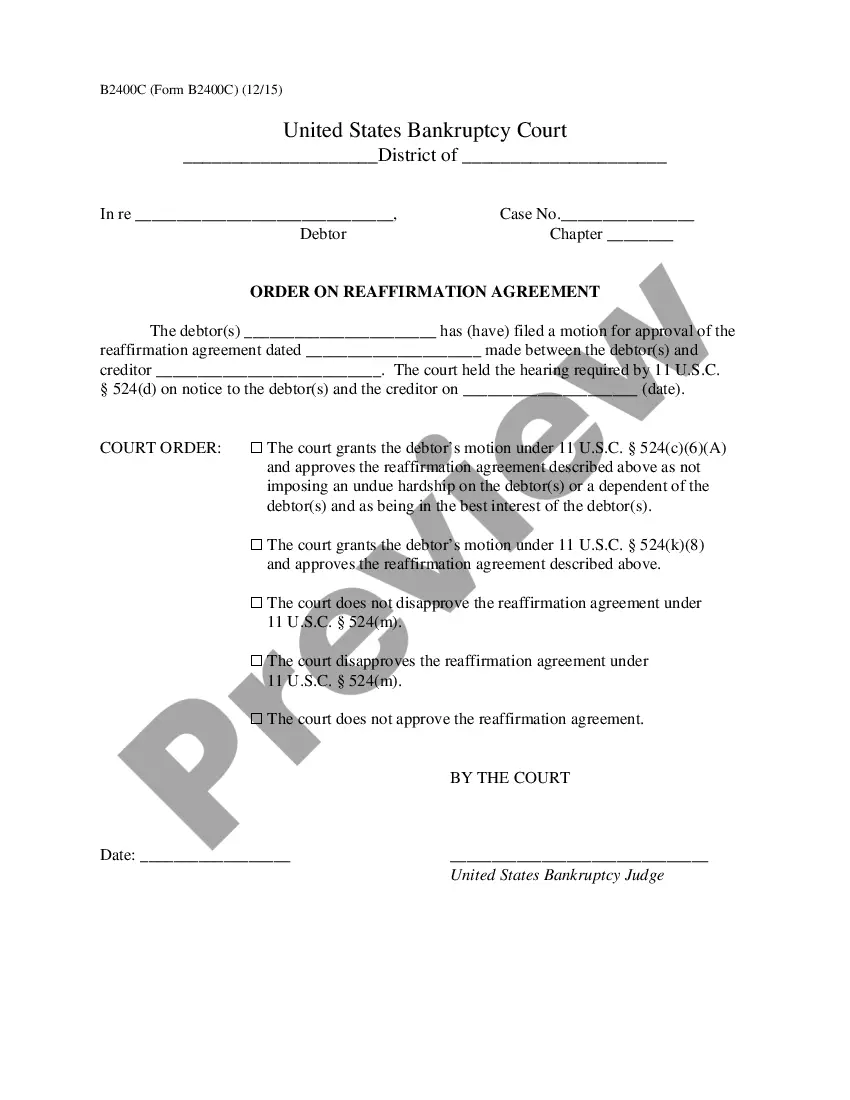

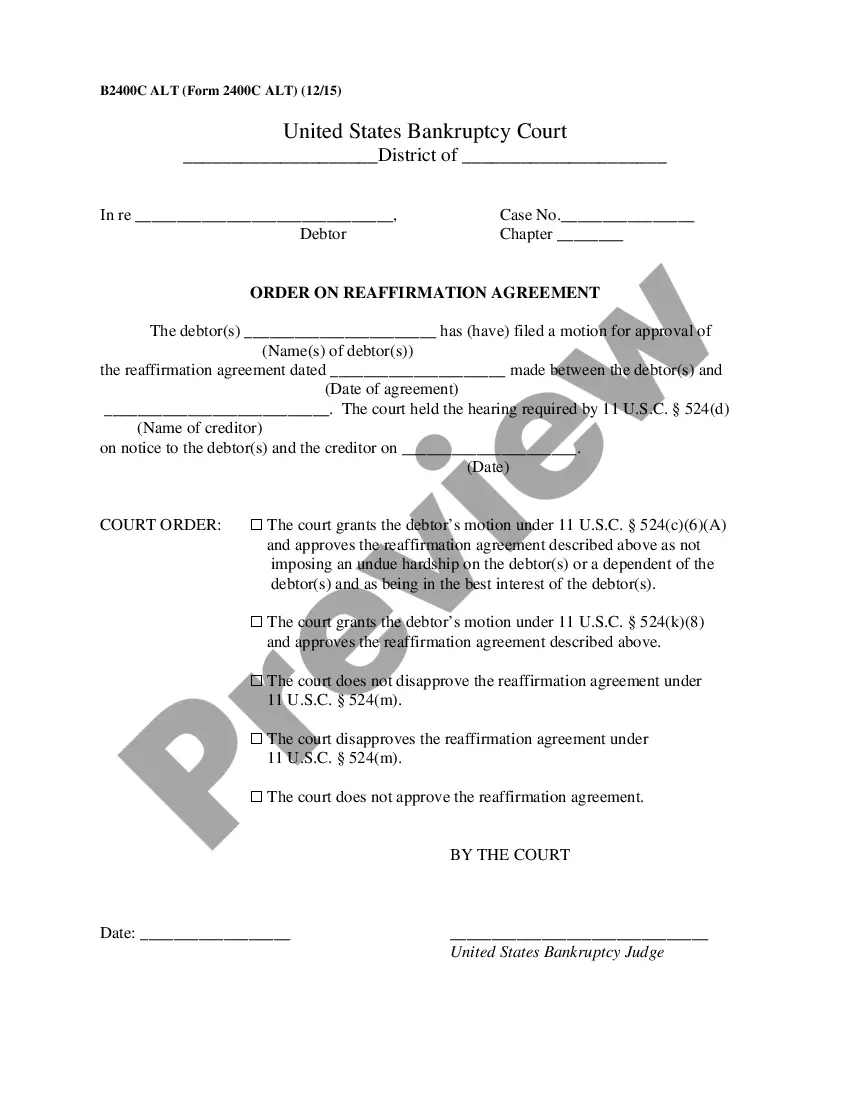

- Court Review: Once filed, the agreement must be reviewed and approved by the bankruptcy court, which also assesses your ability to make the payments outlined in the agreement.

Risk Analysis in Reaffirmation Agreements

Engaging in a reaffirmation agreement carries certain risks. The primary risk is the potential for financial strain or hardship that might occur if the debtors financial situation deteriorates, as they remain legally obligated to make the payments as agreed. Also, failing to comply with the terms can result in repossession of the secured property or other legal actions. It is essential for debtors to consider potential changes in their income and unexpected financial emergencies before entering such agreements.

Comparison Table of Reaffirmation Agreement vs. Discharge

| Criteria | Reaffirmation Agreement | Debt Discharge |

|---|---|---|

| Continuation of Payment | Obliged to continue payments | No further payments required |

| Legal Outcome | Retains ownership of property | Lose any secured assets |

| Risk | High risk of financial hardship | Reduces financial burden |

| Impact on Credit | Can improve credit if payments are made | Typically results in a lower credit score |

Best Practices for Managing Reaffirmation Agreements

To effectively manage reaffirmation agreements, it's advisable to:

- Ensure clarity of terms and seek legal advice.

- Maintain open communication with the creditor to renegotiate terms if needed.

- Regularly review financial status and prepare for potential adjustments.

- Keep thorough records of all payments and correspondence related to the agreement.

How to fill out Reaffirmation Agreement?

How much time and resources do you typically spend on drafting formal paperwork? There’s a better opportunity to get such forms than hiring legal experts or wasting hours searching the web for a proper blank. US Legal Forms is the leading online library that offers professionally drafted and verified state-specific legal documents for any purpose, including the Reaffirmation Agreement.

To obtain and complete a suitable Reaffirmation Agreement blank, adhere to these simple steps:

- Examine the form content to make sure it meets your state requirements. To do so, check the form description or use the Preview option.

- If your legal template doesn’t meet your needs, find another one using the search bar at the top of the page.

- If you already have an account with us, log in and download the Reaffirmation Agreement. Otherwise, proceed to the next steps.

- Click Buy now once you find the right document. Select the subscription plan that suits you best to access our library’s full service.

- Register for an account and pay for your subscription. You can make a payment with your credit card or through PayPal - our service is totally safe for that.

- Download your Reaffirmation Agreement on your device and fill it out on a printed-out hard copy or electronically.

Another benefit of our service is that you can access previously acquired documents that you safely store in your profile in the My Forms tab. Get them anytime and re-complete your paperwork as frequently as you need.

Save time and effort completing formal paperwork with US Legal Forms, one of the most trusted web solutions. Join us now!

Form popularity

FAQ

A reaffirmation agreement allows you to agree with a lender to keep your collateral after filing for bankruptcy. Common types of loans you may make a reaffirmation agreement for include home loans, auto loans or any other significant collateral you use regularly.

A reaffirmation of debt is helpful for individuals filing for bankruptcy who don't want to lose their home or car. By filing a reaffirmation of debt, they can continue to make regular payments without fear of losing their residence or vehicle in the Chapter 7 bankruptcy process.

A reaffirmation agreement is an agreement between a chapter 7 debtor and a creditor that the debtor will pay all or a portion of the money owed, even though the debtor has filed bankruptcy. In return, the creditor promises that, as long as payments are made, the creditor will not repossess or take back its collateral.

What Is a Reaffirmation Agreement? Reaffirmation agreements are a special feature of Chapter 7 bankruptcy. They give your creditors a chance to get you back on the hook for debt you would have otherwise discharged in the bankruptcy by allowing you to reaffirm, or re-sign, liability for a specific debt.

A reaffirmation agreement is where you agree to pay a debt even though you could have eliminated the debt in your bankruptcy case. When you reaffirm a debt, you continue to be legally responsible for paying it back. This gives the creditor some legal rights.

1. I will have reaffirmed the excess loan amount that I received only after I sign and return this form to my loan holder and it is processed. 2. After I have reaffirmed the excess loan amount, my school will determine what types and amounts of federal student financial aid I am eligible to receive.