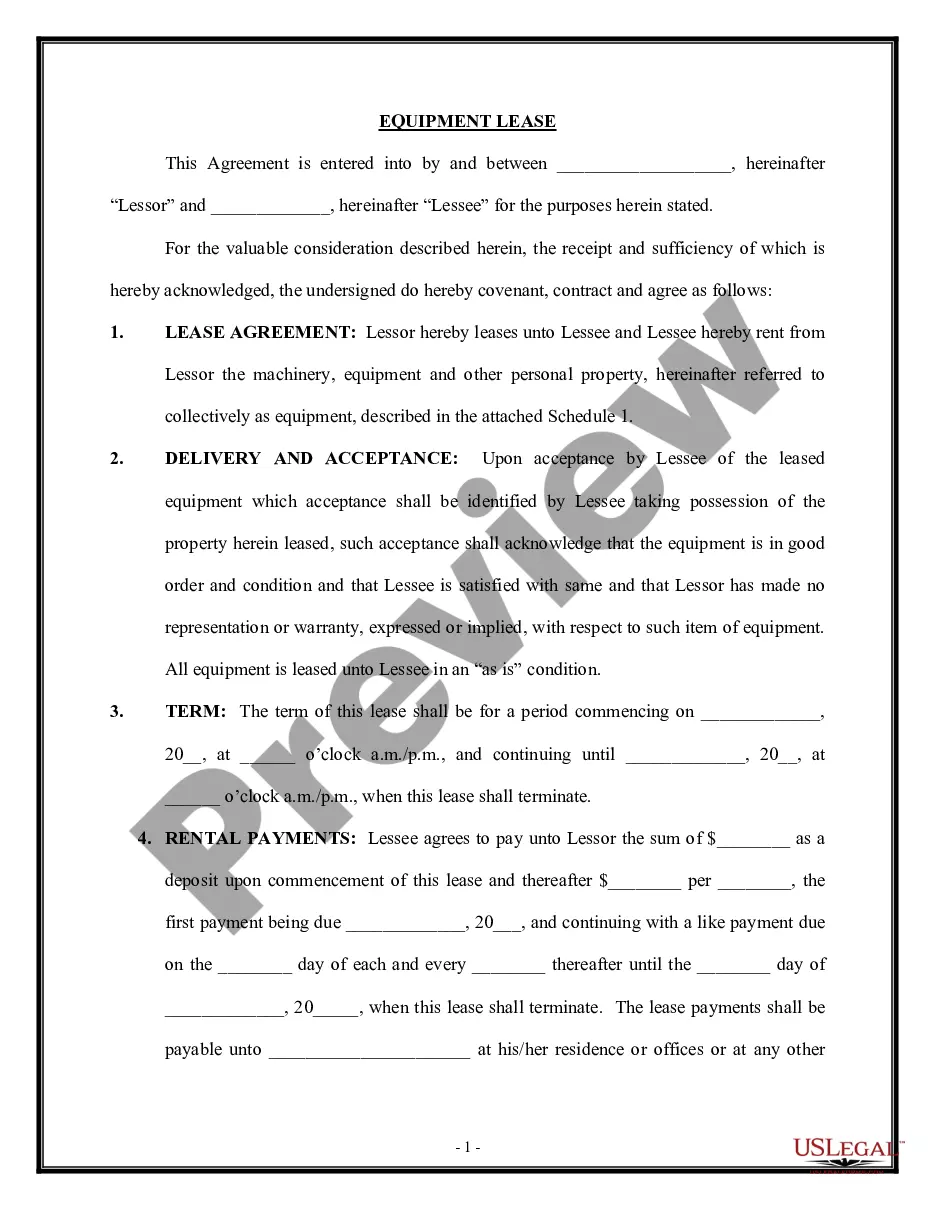

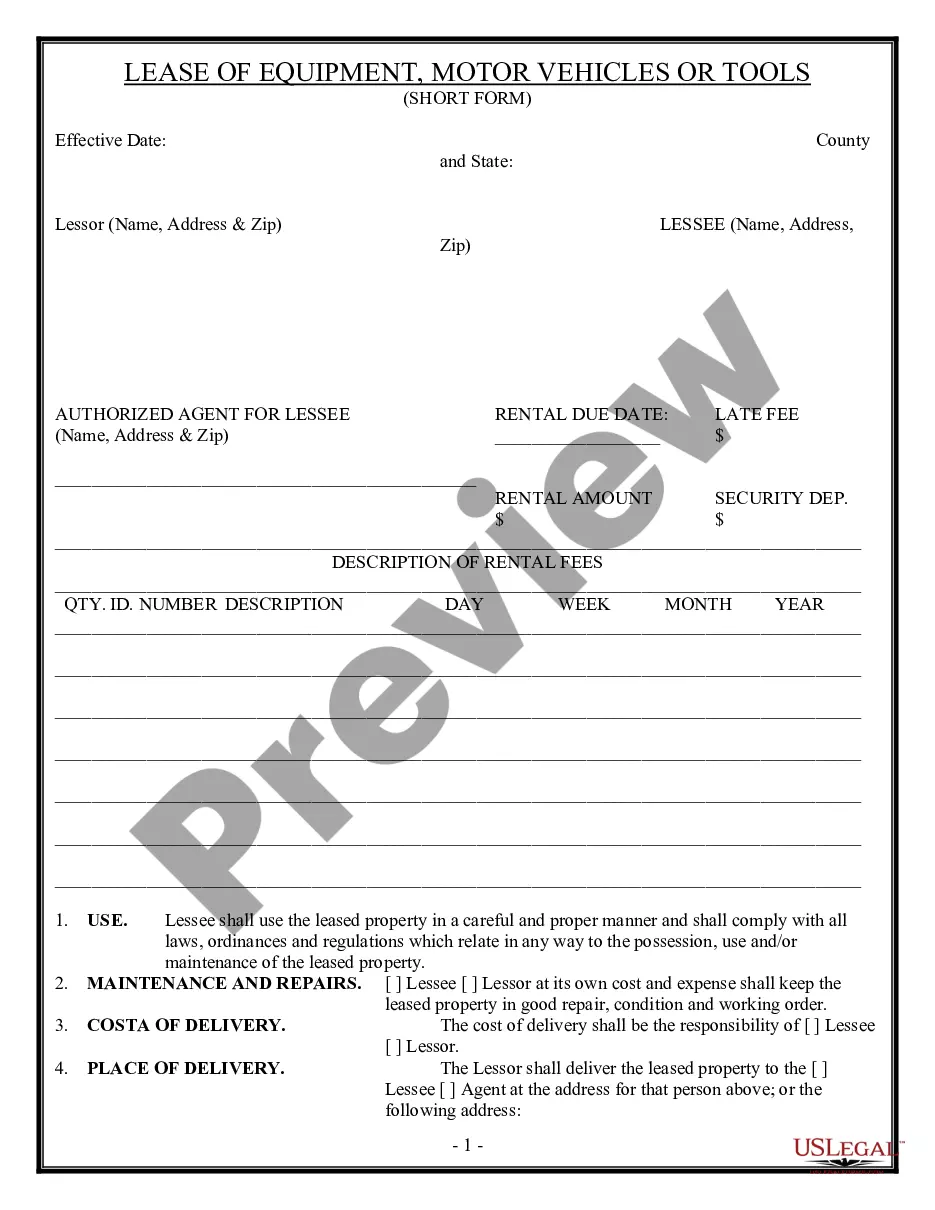

Lease of Industrial Plant and Equipment

Understanding this form

The Lease of Industrial Plant and Equipment is a legal document used to outline the terms of leasing an industrial facility and associated equipment. This form is essential for both lessors and lessees to clarify their rights, responsibilities, and liabilities. Unlike simpler rental agreements, this lease is specifically tailored for industrial use, addressing complex financial arrangements like gross sales-based rental payments and detailing maintenance obligations for the equipment.

Key components of this form

- Description of premises, including the location and purpose of the lease.

- Details about the lease term and rental payment structure, including minimum and additional rental based on sales.

- Conditions regarding maintenance, repairs, and alterations of the premises and equipment.

- Default clauses outlining the actions that may be taken if rental payments are not made.

- Governing law and dispute resolution through mandatory arbitration.

When to use this form

This form should be used when a business entity, such as a corporation, wishes to lease an industrial property and the associated machinery or equipment. Typical scenarios include manufacturing firms expanding their operations, companies needing temporary workspace for projects, or businesses seeking specialized equipment without the financial burden of purchasing it outright.

Who can use this document

- Business owners seeking to lease industrial facilities and equipment.

- Lessors who own industrial properties and equipment looking to establish formal leasing agreements.

- Counselors or legal representatives assisting businesses in property leasing arrangements.

Steps to complete this form

- Identify the parties involved by entering the names and addresses of the lessor and lessee.

- Describe the industrial premises and the specific equipment being leased.

- Specify the lease term, including the start and termination dates.

- Detail the rental amounts and the structure for any additional payment based on sales.

- Include any necessary approvals for alterations or subleases by obtaining written consent from the lessor as required.

Is notarization required?

This form does not typically require notarization unless specified by local law. However, having the lease notarized can provide an additional layer of legal assurance.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Typical mistakes to avoid

- Failing to include complete and accurate descriptions of the leased property and equipment.

- Not specifying the rental payment details clearly, including dates and amounts.

- Neglecting to update the lease terms if business conditions change.

Why use this form online

- Convenient access to a legally vetted template saves time and reduces errors.

- Editability allows customization to fit specific business needs.

- Reliable updates ensure compliance with current legal standards.

Looking for another form?

Form popularity

FAQ

The equipment account is debited by the present value of the minimum lease payments and the lease liability account is the difference between the value of the equipment and cash paid at the beginning of the year. Depreciation expense must be recorded for the equipment that is leased.

A lessee must capitalize a leased asset if the lease contract entered into satisfies at least one of the four criteria published by the Financial Accounting Standards Board (FASB). An asset should be capitalized if:The lease runs for 75% or more of the asset's useful life.

Assets being leased are not recorded on the company's balance sheet; they are expensed on the income statement. So, they affect both operating and net income.

Accounting Treatment Of Leased Asset The lease payments also include interest, and the lessee needs to record it separately. For instance, if in a lease payment of $1000, $200 is for the interest expense, then $800 would be a debit to the capital lease liability account and $200 to the interest account.

Unlike an outright purchase or equipment secured through a standard loan, equipment under an operating lease cannot be listed as capital. It's accounted for as a rental expense. This provides two specific financial advantages: Equipment is not recorded as an asset or liability.

Leasing companies can make money when a lessee requests for an upgrade to the equipment they currently have or request for the lease contract to be modified. If the upgrade does not have a stand-alone value or is not readily removable, the leasing company will pay for the upgrade.

The equipment account is debited by the present value of the minimum lease payments and the lease liability account is the difference between the value of the equipment and cash paid at the beginning of the year. Depreciation expense must be recorded for the equipment that is leased.

Calculate the present value of all lease payments; this will be the recorded cost of the asset. Record the amount as a debit to the appropriate fixed asset account, and a credit to the capital lease liability account.