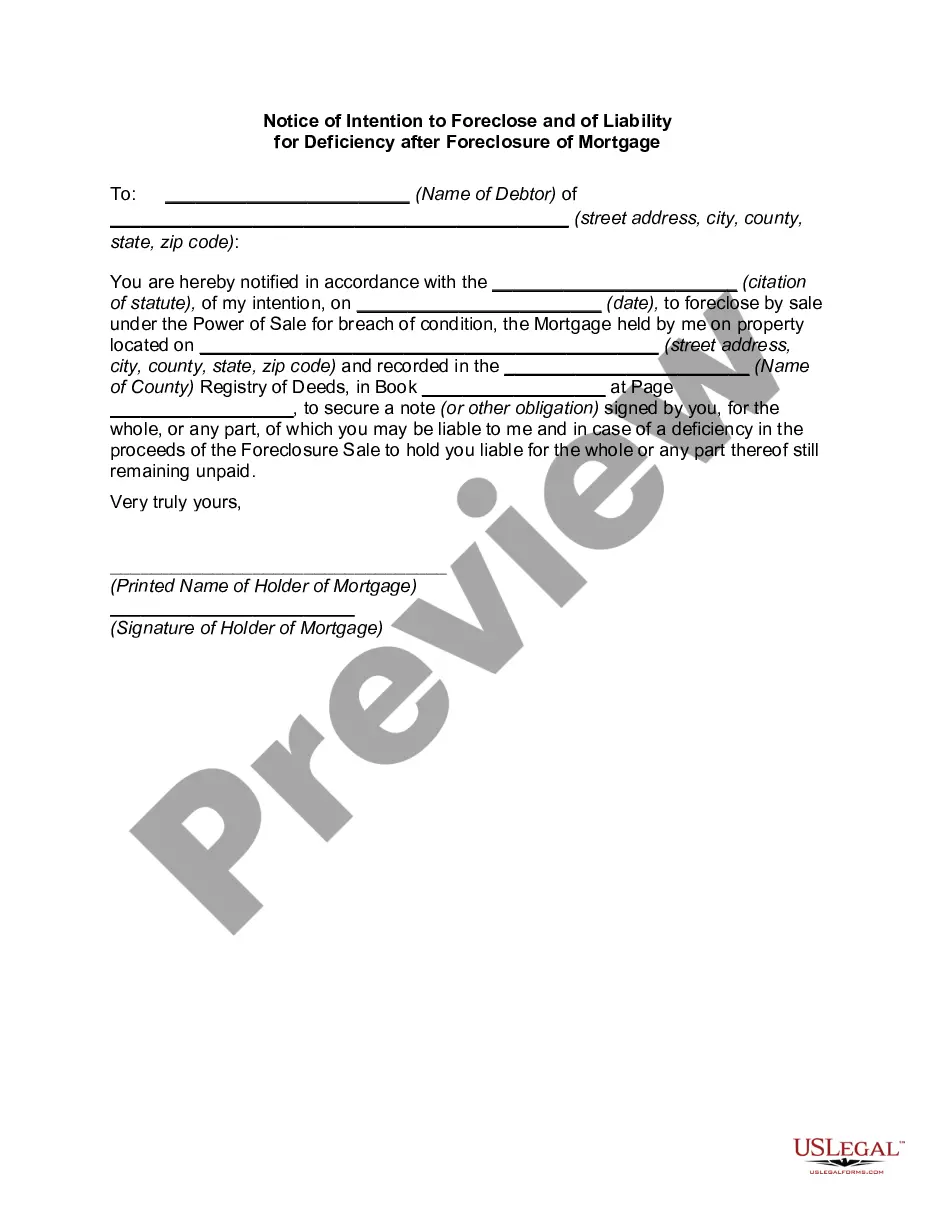

Notice of Foreclosure Sale - Intent to Foreclose

Overview of this form

The Notice of Foreclosure Sale - Intent to Foreclose is a legal document that a mortgage lender uses to officially inform a borrower about the impending foreclosure of their property. This notice is typically required by state law and aims to ensure that borrowers are aware of the status of their mortgage prior to the initiation of foreclosure proceedings. The form details important information regarding amounts owed, the property involved, and potential alternatives to foreclosure, making it distinct from other foreclosure-related documents.

Form components explained

- Names of interested parties involved in the mortgage.

- Citation to the relevant state statute governing the foreclosure process.

- Date and details of the original mortgage agreement.

- Specific information regarding the foreclosure sale, including date, time, and location.

- Details of the default, including amounts due and interest rates.

- Legal description of the property being foreclosed upon.

Common use cases

This form is needed when a lender intends to foreclose on a property due to the borrower's failure to make timely mortgage payments. It is typically used in circumstances where state law mandates that borrowers must receive written notice prior to the commencement of foreclosure proceedings. Using this form can help borrowers understand their situation and explore alternatives to foreclosure.

Who needs this form

The following parties should use the Notice of Foreclosure Sale - Intent to Foreclose:

- Mortgage lenders or servicers initiating foreclosure on a property.

- Borrowers who have defaulted on their mortgage payments and need to understand their legal standing.

- Real estate professionals involved in foreclosure processes.

How to prepare this document

- Identify and list the names of all interested parties related to the mortgage.

- Enter the citation to the applicable state statute that governs the notice.

- Specify the date and details of the original mortgage agreement.

- Provide the foreclosure sale date, time, and location.

- Detail the amounts owed, including principal, interest, and any additional charges.

- Include a legal description of the foreclosed property.

Does this form need to be notarized?

This form must be notarized to be legally valid. US Legal Forms provides secure online notarization powered by Notarize, allowing you to complete the process through a verified video call.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Common mistakes

- Failing to include all required names of interested parties.

- Omitting the citation to the relevant state statute.

- Incorrectly stating the amounts due or not providing a breakdown of charges.

- Not signing and dating the form appropriately.

Why use this form online

- Convenient downloading and printing options for immediate use.

- Editability allows for customization tailored to your specific situation.

- Access to forms created by licensed attorneys ensures reliability and compliance with legal standards.

Looking for another form?

Form popularity

FAQ

The borrower defaults on the loan. The lender issues a notice of default (NOD). A notice of trustee's sale is recorded in the county office. The lender tries to sell the property at a public auction.

Foreclosure is what happens when a homeowner fails to pay the mortgage.If the owner can't pay off the outstanding debt, or sell the property via short sale, the property then goes to a foreclosure auction. If the property doesn't sell there, the lending institution takes possession of it.

The auction notice, or Notice of Sale, is your final notice that the lender intends to sell the property at auction. The county prints the location, time and date of the trustee's auction on the Notice of Sale. It also contains the name and contact information for the trustee in charge of the sale.

The California foreclosure process can last up to 200 days or longer. Day 1 is when a payment is missed; your loan is officially in default around day 90. After 180 days, you'll receive a notice of trustee sale. About 20 days later, your bank can then set the auction.

You can stop the foreclosure process by informing your lender that you will pay off the default amount and extra fees. Your lender would prefer to have the money much more than they would have your home, so unless there are extenuating circumstances, this should work.

Phase 1: Payment Default. Phase 2: Notice of Default. Phase 3: Notice of Trustee's Sale. Phase 4: Trustee's Sale. Phase 5: Real Estate Owned (REO) Phase 6: Eviction. The Bottom Line.

How long it takes for your home to foreclose once you receive notice of lis pendens will depend on the state. In California, it might take a minimum of 120 days, and 180 days in Florida, while in New York it can take as long as 15 months after the notice is filed.

An intent to foreclose is a notice you receive from your lender advising you that if you do not bring your mortgage current, the lender will file a foreclosure notice against your home.

Phase 1: Payment Default.Phase 2: Notice of Default.Phase 3: Notice of Trustee's Sale.Phase 4: Trustee's Sale.Phase 5: Real Estate Owned (REO)Phase 6: Eviction.The Bottom Line.