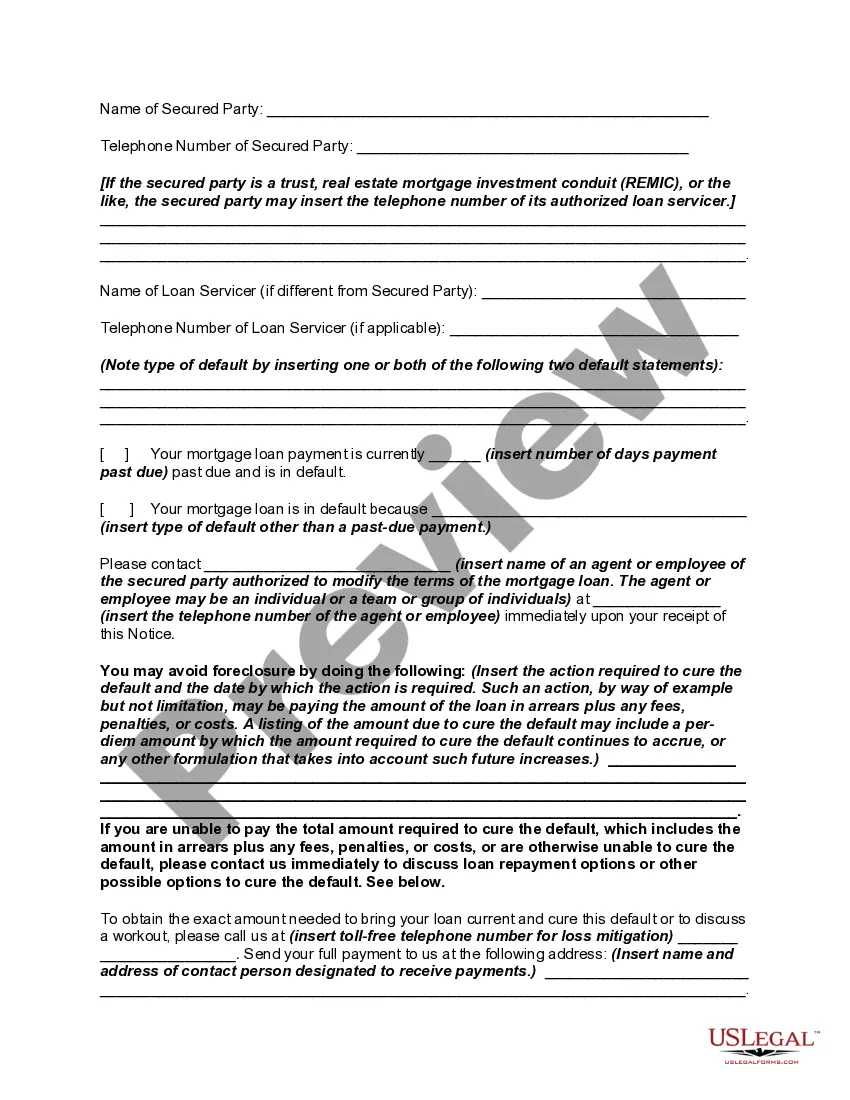

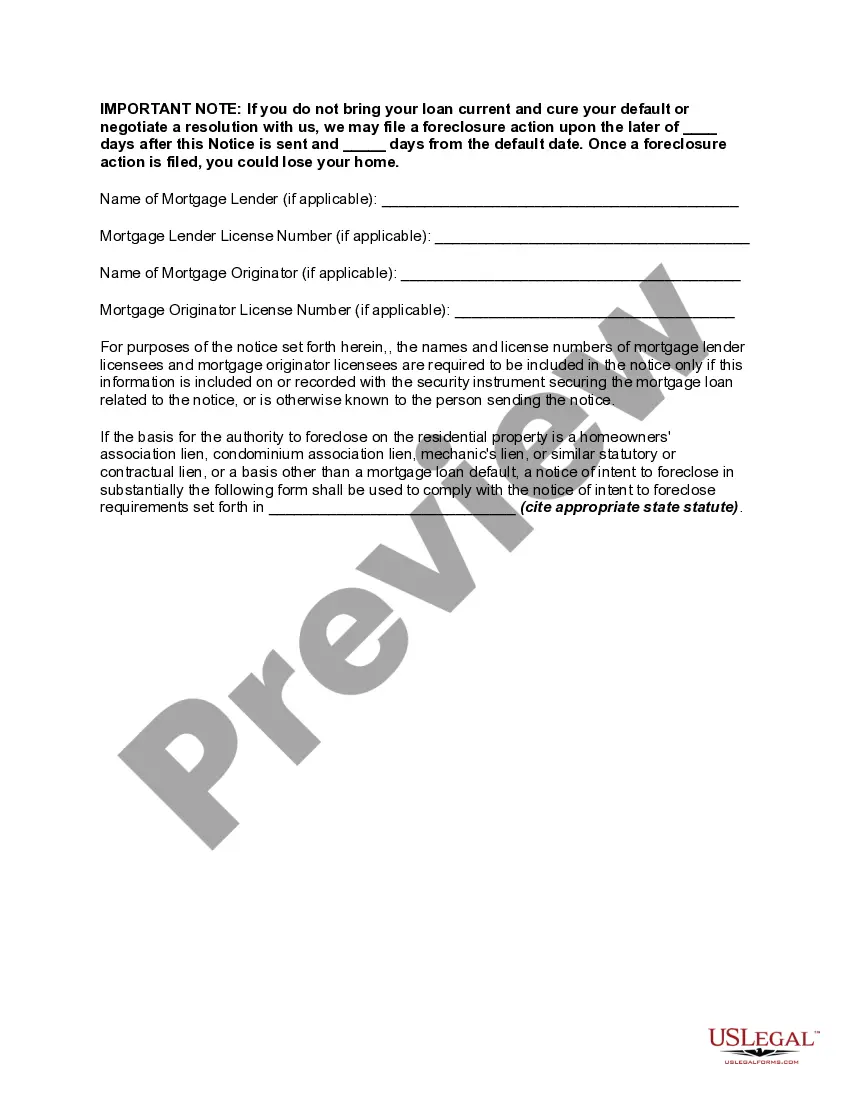

A number of states have enacted measures to facilitate greater communication between borrowers and lenders by requiring mortgage servicers to provide certain notices to defaulted borrowers prior to commencing a foreclosure action. The measures serve a dual purpose, providing more meaningful notice to borrowers of the status of their loans and slowing down the rate of foreclosures within these states. For instance, one state now requires a mortgagee to mail a homeowner a notice of intent to foreclose at least 45 days before initiating a foreclosure action on a loan. The notice must be in writing, and must detail all amounts that are past due and any itemized charges that must be paid to bring the loan current, inform the homeowner that he or she may have options as an alternative to foreclosure, and provide contact information of the servicer, HUD-approved foreclosure counseling agencies, and the state Office of Commissioner of Banks.

Notice Of Intent To Foreclose Form

Description Notice Of Foreclosure Letter

How to fill out What Does A Foreclosure Notice Look Like?

Aren't you sick and tired of choosing from numerous samples every time you want to create a Notice of Intent to Foreclose - Mortgage Loan Default? US Legal Forms eliminates the lost time numerous Americans spend searching the internet for suitable tax and legal forms. Our skilled group of attorneys is constantly upgrading the state-specific Forms collection, so it always provides the proper documents for your situation.

If you’re a US Legal Forms subscriber, just log in to your account and click on the Download button. After that, the form can be found in the My Forms tab.

Visitors who don't have an active subscription need to complete easy steps before having the ability to get access to their Notice of Intent to Foreclose - Mortgage Loan Default:

- Use the Preview function and look at the form description (if available) to be sure that it’s the appropriate document for what you’re trying to find.

- Pay attention to the applicability of the sample, meaning make sure it's the appropriate sample to your state and situation.

- Use the Search field on top of the web page if you need to look for another file.

- Click Buy Now and select a convenient pricing plan.

- Create an account and pay for the service using a credit card or a PayPal.

- Get your template in a required format to finish, print, and sign the document.

As soon as you have followed the step-by-step recommendations above, you'll always have the capacity to log in and download whatever file you will need for whatever state you want it in. With US Legal Forms, finishing Notice of Intent to Foreclose - Mortgage Loan Default templates or other legal documents is easy. Get started now, and don't forget to look at your examples with accredited lawyers!