Notice of Intent to Foreclose - Mortgage Loan Default

Understanding this form

The Notice of Intent to Foreclose - Mortgage Loan Default is a formal document that informs borrowers of default on their mortgage loans. This form serves as a crucial preliminary step in the foreclosure process, allowing borrowers to understand their default status and explore options to avoid foreclosure. By providing specific details about amounts owed and potential solutions, this form helps facilitate communication between lenders and borrowers, which is essential in navigating mortgage challenges.

What’s included in this form

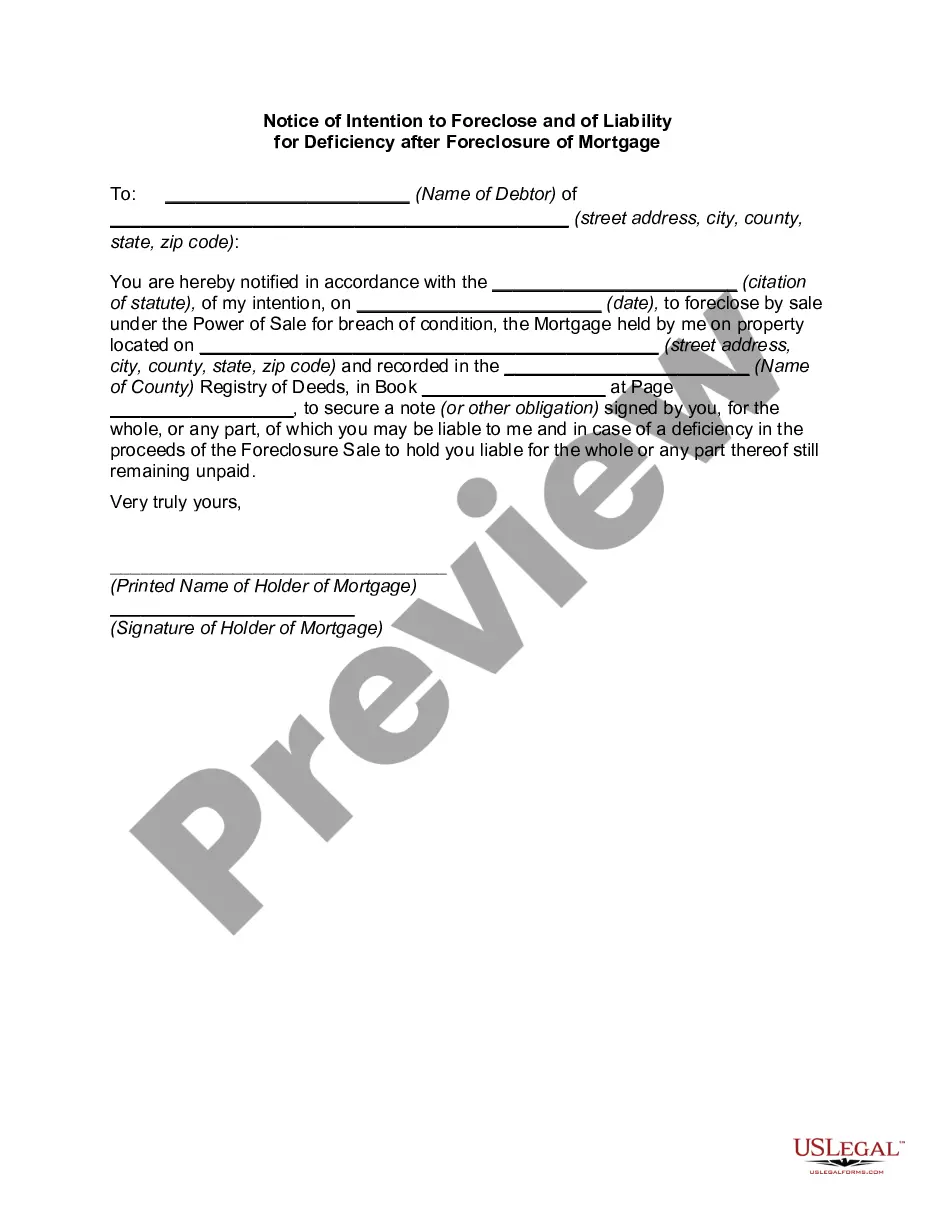

- Date of notice and address of the property affected.

- Names and mailing addresses of borrowers and record owners.

- Mortgage loan number and lien position of the mortgage.

- Total amount required to cure the default, including itemized charges.

- Contact details for the secured party and loan servicer.

- Instructions on how to remedy the default and avoid foreclosure.

When to use this form

This form should be used when a borrower is in default on their mortgage loan and the lender intends to initiate foreclosure proceedings. The notice provides borrowers with critical information about their loan status, amounts past due, and the steps needed to avoid losing their property. Utilizing this form ensures compliance with state laws requiring notification before foreclosure actions can commence.

Intended users of this form

- Borrowers who have received notifications of default on their mortgage loan.

- Lenders and mortgage servicers preparing to communicate intent to foreclose.

- Real estate and loan professionals assisting clients with mortgage issues.

Completing this form step by step

- Identify and enter the date of the notice and the property address.

- List the names and addresses of the borrower and record owner.

- Provide the mortgage loan number and specify the lien position.

- Include the total amount required to cure the default and itemize charges.

- Detail contact information for both the secured party and any loan servicer.

- Clearly state the necessary actions required to cure the default and the deadline to take those actions.

Notarization guidance

This form does not typically require notarization unless specified by local law. However, it is always advisable to check specific state requirements to ensure compliance with any legal standards that may apply.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Avoid these common issues

- Failing to include the correct property address.

- Not providing complete contact information for the secured party or loan servicer.

- Omitting important details about the amount due and how it can be cured.

- Using outdated templates that do not comply with current state laws.

Why use this form online

- Convenient access to legally compliant templates.

- Easy to customize with specific borrower and property details.

- Quick download options for immediate use.

- Assurance that forms are drafted in accordance with state-specific regulations.

Looking for another form?

Form popularity

FAQ

The notice of default doesn't affect your credit file, but when the account defaults this will be recorded.If the debt is regulated by the Consumer Credit Act, you must be sent a default notice warning letter and have time to act on it before the default is recorded on your credit file.

If you cannot work out a doable solution with the mortgage lender, or you ignore their notices completely, you will then go into foreclosure. Typically, this happens once your payment becomes 120 days past due.The IRS views any financial loss on the part of the lender for your mortgage as taxable income for you.

A notice of default is typically the final action lenders take before activating the lien and seizing the collateral for foreclosure. A notice of default is usually filed with the state court in which the lien is recorded followed by a hearing to activate the perfected lien recorded with the mortgage closing.

A notice of default is the first step to a bank or mortgage lender's foreclosure process.If the mortgage is not paid up to date, the lender will seize the home. A notice of default is also known as a reinstatement period, notice of public auction, or notice of foreclosure.

You can stop the foreclosure process by informing your lender that you will pay off the default amount and extra fees. Your lender would prefer to have the money much more than they would have your home, so unless there are extenuating circumstances, this should work.

A default occurs when a borrower does not make his or her mortgage loan payment and falls behind. When this happens, he or she risks the home heading into the foreclosure process. Usually, the foreclosure process is started within thirty days after the due date is not met.

After the lender files the Notice of Default, you get 90 days to bring your past-due bill current. After the 90 days pass, the lender files a Notice of Sale with the clerk. The Notice of Sale displays the location, date and time of the sale. It lists the trustee's name and contact information.