Sale of Partnership to Corporation

What this document covers

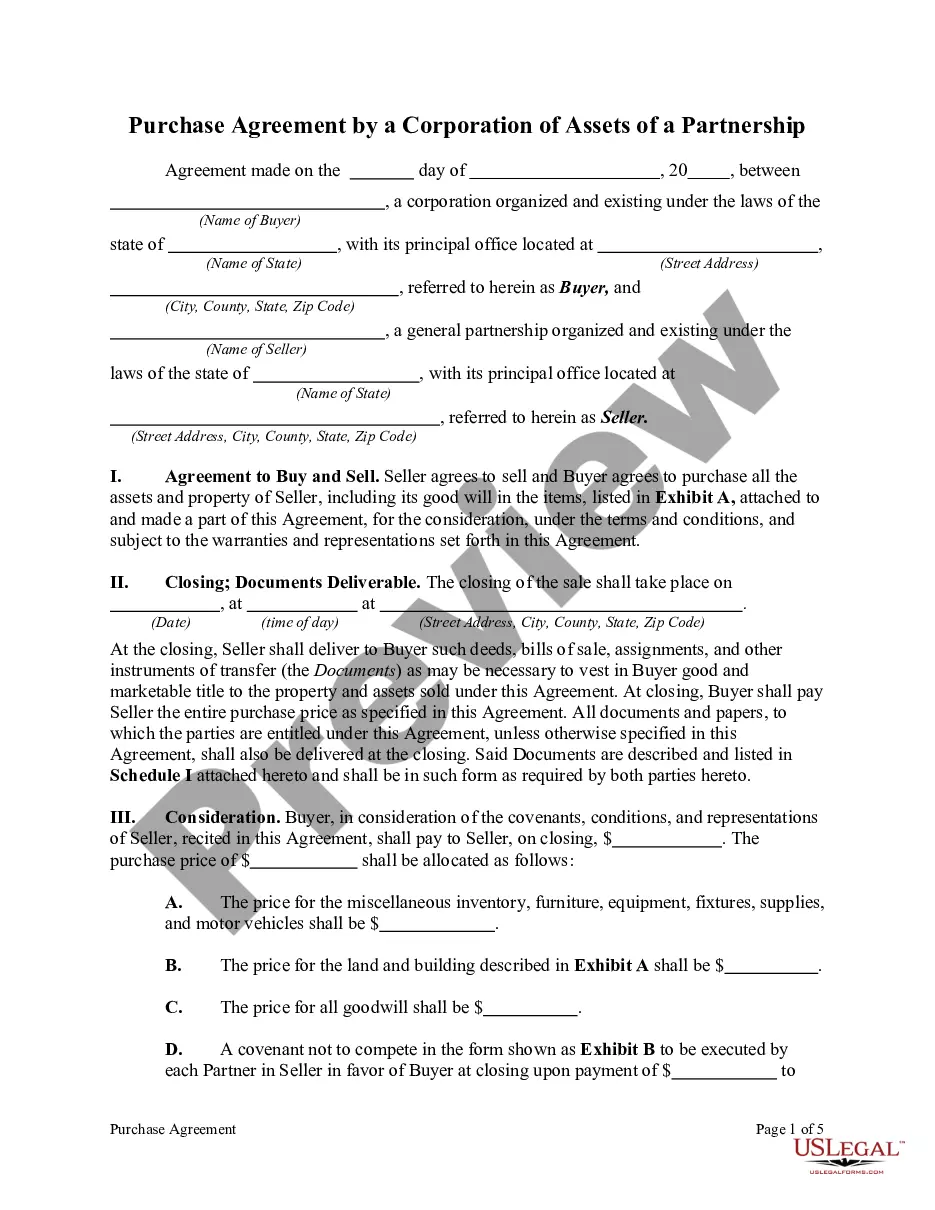

The Sale of Partnership to Corporation form is a legal document that facilitates the transfer of ownership of a partnership's assets to a corporation. This form is specifically designed for situations where a partner seeks to sell their interest in a partnership to a corporate entity. It includes critical provisions to ensure a smooth transaction while providing clear terms for both the buyer and seller, making it distinct from other partnership transfer agreements.

Form components explained

- Identifies the buyer (corporation) and seller (partnership) involved in the sale.

- Details the purchase price and payment method for the partnership assets.

- Outlines conditions precedent that must be met before the sale is finalized.

- Includes warranties from the seller regarding their authority to sell and the state of partnership assets.

- Establishes the closing date for the transaction.

When to use this form

This form should be used when a partnership is being sold in its entirety to a corporation. It is particularly applicable in a variety of scenarios, such as succession planning, business restructuring, or when partners decide to liquidate their interests in favor of a corporate entity. Utilizing this form helps clarify the terms of the sale and protects the interests of both parties involved.

Who should use this form

This form is intended for:

- Partners of a partnership looking to sell their interests to a corporation.

- Corporations interested in acquiring partnership assets.

- Legal representatives assisting clients with the sale of partnership interests.

How to complete this form

- Identify and fill in the names and addresses of both the buyer and seller.

- Specify the total purchase price and the method of payment (e.g., cashier's check).

- Outline the conditions that must be satisfied before the sale is finalized.

- Complete the warranties section, ensuring all partners agree to the sale terms.

- Set and confirm the closing date for the transaction.

Notarization guidance

Notarization is generally not required for this form. However, certain states or situations might demand it. You can complete notarization online through US Legal Forms, powered by Notarize, using a verified video call available anytime.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Avoid these common issues

- Failing to disclose all partnership liabilities can lead to legal issues post-sale.

- Not ensuring all partners sign the agreement, which can invalidate the contract.

- Omitting important details regarding the allocation of the purchase price.

Benefits of using this form online

- The form can be easily downloaded and customized to fit specific requirements.

- Access to legal form templates drafted by licensed attorneys ensures trusted content.

- Convenient editing options allow users to fill out their details seamlessly.

Quick recap

- The Sale of Partnership to Corporation form is essential for transferring partnership assets to a corporation.

- Always ensure all partners agree and sign the agreement to avoid conflicts.

- Review state-specific requirements to guarantee legal compliance.

Looking for another form?

Form popularity

FAQ

Partnerships are not taxed on the company's income, but each partner is taxed on their individual share of business profits.Most businesses begin as sole-proprietorships or partnerships, and eventually incorporate to protect the owners.

Partnerships file Form 8308 to report the sale or exchange by a partner of all or part of a partnership interest where any money or other property received in exchange for the interest is attributable to unrealized receivables or inventory items (that is, where there has been a section 751(a) exchange).

The sale of an entire partnership business generally takes one of two forms: the partners sell all of their partnership interests, or. the partnership sells some or all of its assets, and distributes the cash and any remaining property to the partners.

A partner may withdraw from a partnership by either sale or liquidation of their interest. The former is taxable. The seller-partner will recognize ordinary income to the extent that the gain from the sale of their interest is attributable to unrealized receivables and inventory.

An LLC can transition to a corporation, but conversion might mean more paperwork and taxes. If the owners of your LLC agree, you can convert your company to a corporation. Some states have a streamlined process that allows you to easily transition your LLC to a corporation.

As stated above, conversion from a partnership to a corporate status can be done by liquidating (dissolving) the current business entity or by transferring ownership of the current entity over to the corporation.Second, the partnership may liquidate by contributing partnership assets to the new corporate entity.

By default, LLCs with more than one member are treated as partnerships and taxed under Subchapter K of the Internal Revenue Code.And, once it has elected to be taxed as a corporation, an LLC can file a Form 2553, Election by a Small Business Corporation, to elect tax treatment as an S corporation.

Buyouts over time agree that the purchasing partner will pay the bought out partner a predetermined amount over time until their ownership has been fully purchased. Similarly, an earn-out pays the partner out over time but requires the partner to stay with the company during a defined transition period.

For federal tax purposes, you can simply make an election for the LLC to be taxed as an S Corporation. All you need to do is fill out a form and send it to the IRS. Once the LLC is classified for federal tax purposes as a Corporation, it can file Form 2553 to be taxed as an S Corporation.