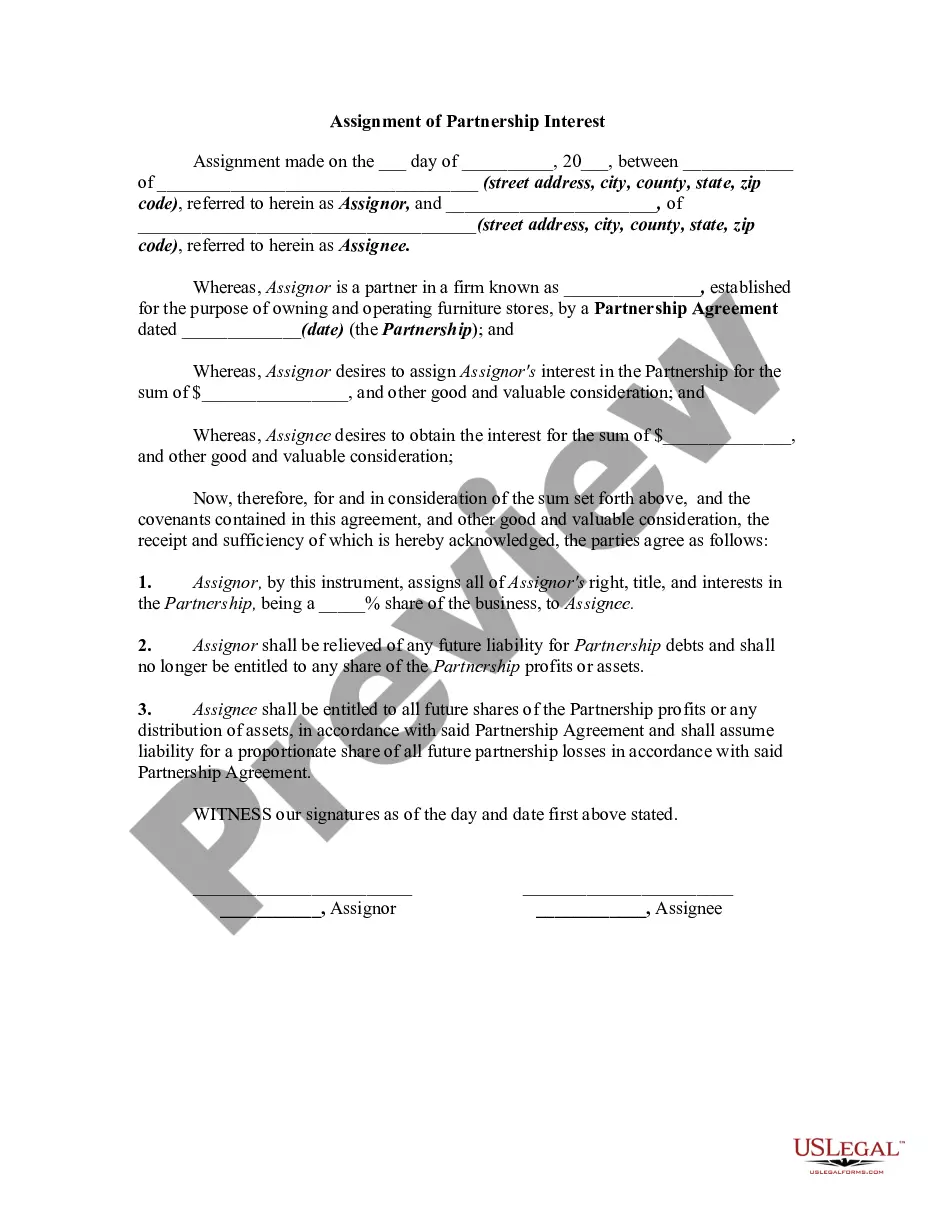

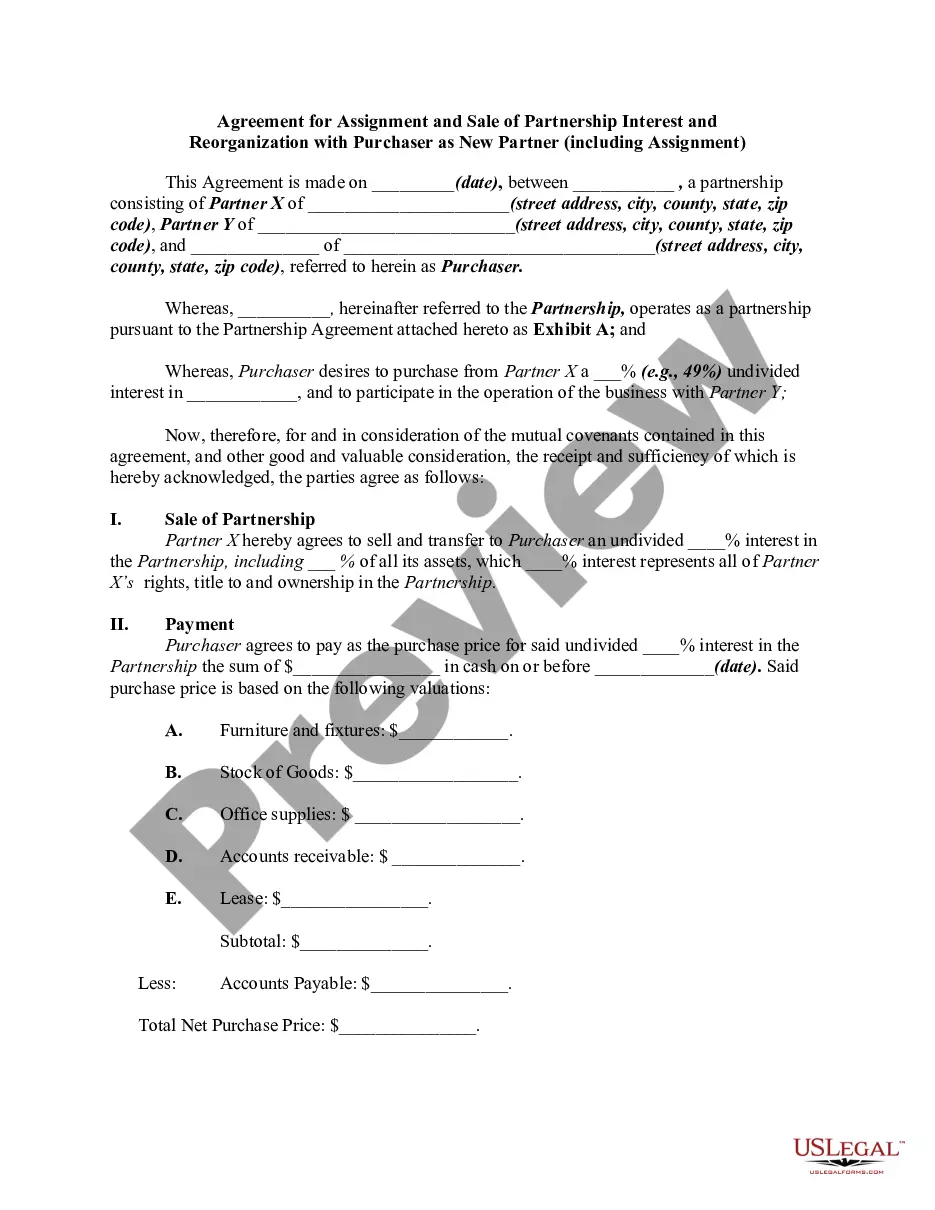

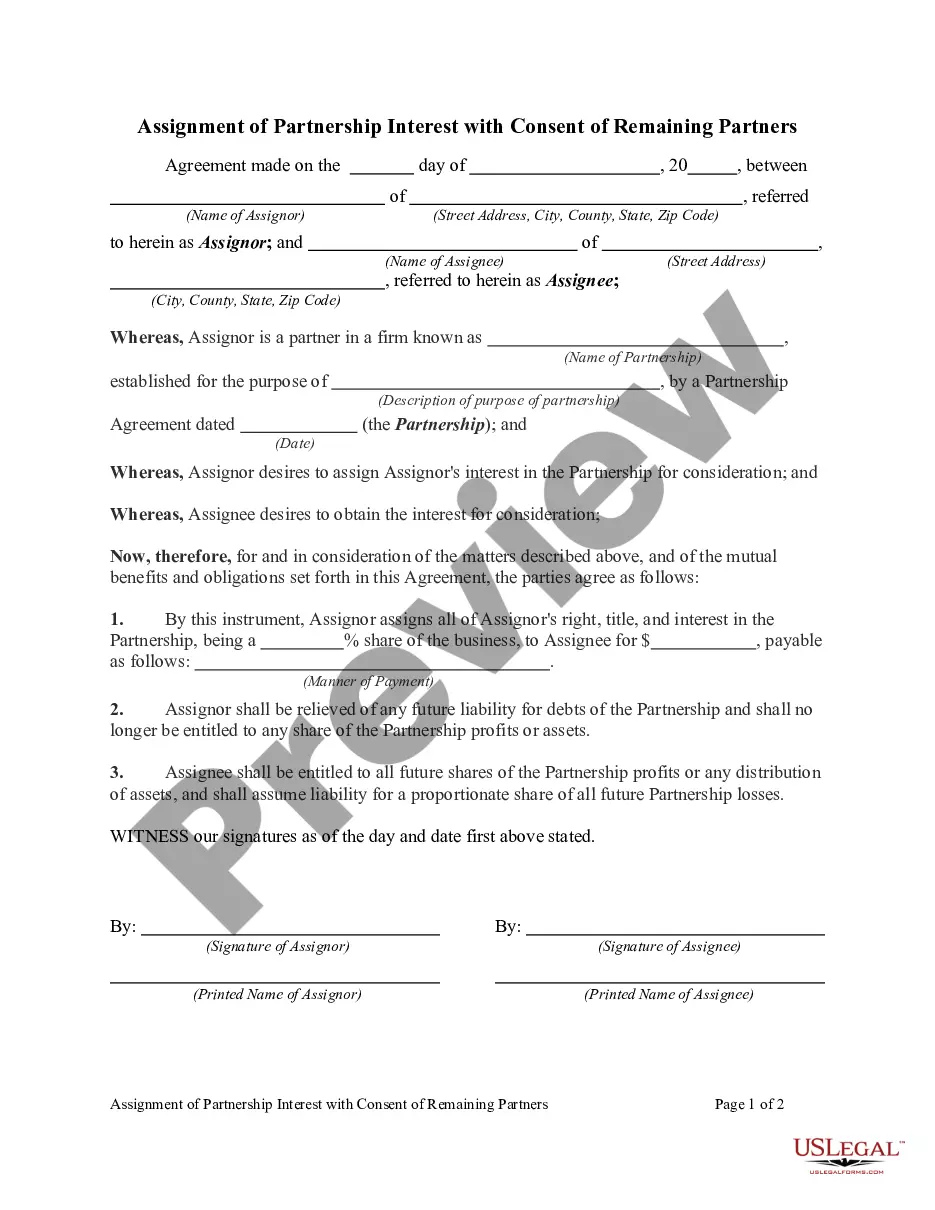

Assignment of Partnership Interest to a Corporation with Consent of Remaining Partners

Overview of this form

The Assignment of Partnership Interest to a Corporation with Consent of Remaining Partners is a legal document that facilitates the transfer of a partner's interest in a partnership to a corporation. This form ensures that the remaining partners consent to this assignment, thereby maintaining harmony within the partnership. It serves a different purpose than an outright sale or transfer of business interests, as it specifically involves both the interests of the assignee and the existing partners.

Form components explained

- Identification of the assignee and the partnership.

- Details of the consideration given for the partnership interest.

- Agreement to share future profits and losses.

- Consent statement from the remaining partners.

- Signatures of all parties involved, indicating their agreement.

Situations where this form applies

This form is essential when a partner wishes to transfer their partnership interest to a corporation. It is used when the partnership structure requires the consent of the remaining partners, ensuring their agreement to the change. This scenario may arise during business expansions, mergers, or when a partner departs and a corporation takes their place.

Who can use this document

This form should be used by:

- Partners in a partnership who wish to reevaluate their business structure.

- Corporations intending to acquire a partnership interest.

- Remaining partners who must consent to the assignment of interest.

Steps to complete this form

- Identify all parties involved, including the transferor, assignee, and remaining partners.

- Specify the terms of the partnership interest being transferred.

- State the consideration being offered for the interest.

- Obtain written consent from all remaining partners.

- Ensure that all parties sign and date the document in the appropriate sections.

Is notarization required?

This form does not typically require notarization unless specified by local law. However, verifying your stateâs requirements is advisable to ensure legal validity.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Mistakes to watch out for

- Failing to obtain proper consent from all remaining partners, which can invalidate the transfer.

- Not clearly defining the terms of the partnership interest or consideration offered.

- Missing signatures or dates, which can lead to disputes later on.

Benefits of completing this form online

- Convenient access to the form allows quick completion at any time.

- Editable fields enable users to customize the document easily.

- Reliable templates prepared by licensed attorneys ensure legal compliance.

Quick recap

Key takeaways:

- This form allows for the assignment of partnership interest to a corporation with consent from remaining partners.

- It is essential for preventing disputes and clarifying profit-sharing and liabilities.

- Ensure all parties consent and sign to validate the transfer legally.

Looking for another form?

Form popularity

FAQ

An Assignment of Partnership Interest is a legal document that transfers the rights to receive benefits from an original business partner (Assignor) to a new business partner (Assignee).Assignee: name and address of the new partner receiving the business interest.

Types of Partnership General Partnership, Limited Partnership, Limited Liability Partnership and Public Private Partnership.

An assignment of interest is a transfer of a limited liability company (LLC) owner's interest in the LLC. The most common reasons for an LLC owner to transfer their interest in an LLC are to leave the LLC, to pay off a debt, or to secure a loan.

Partnership Interests If assigned, however, the person receiving the assigned interest does not become a partner. Rather, the assignee only receives the economic rights of the partner, such as the right to receive partnership profits.

Termination when only one partner remains The partnership form also ceases to exist if a transfer of partnership interests occurs and only one partner remains. For example, a partnership terminates when a 60% partner acquires the interests of two other partners who each have a 20% interest in the partnership (Regs.

A partner's interest in a partnership is considered personal property that may be assigned to other persons. In addition, an assignment of the partner's interest does not give the assignee any right to participate in the management of the partnership.

The federal income tax rules for partnership payments to buy out an exiting partner's interest are tricky, but they also open up tax planning opportunities. Payments made by a partnership to liquidate (or buy out) an exiting partner's entire interest are covered by Section 736 of the Internal Revenue Code.

A limited partner's interest in the partnership is personal property. A limited partner's interest is assignable. A substituted limited partner is a person admitted to all the rights of a limited partner who has died or has assigned his interest in a partnership.