Letter Denying Consumer Credit and Notice of Rights under Equal Credit Opportunity Act

What this document covers

The Letter Denying Consumer Credit and Notice of Rights under Equal Credit Opportunity Act is a formal communication from a creditor to a consumer when an application for credit is denied. This letter serves not only to inform the applicant of the adverse action but also outlines their rights under federal law. Unlike generic denial letters, this form adheres to specific requirements set forth by the Fair Credit Reporting Act and the Equal Credit Opportunity Act, ensuring that consumers are properly informed about their rights and the reasons for the denial.

Form components explained

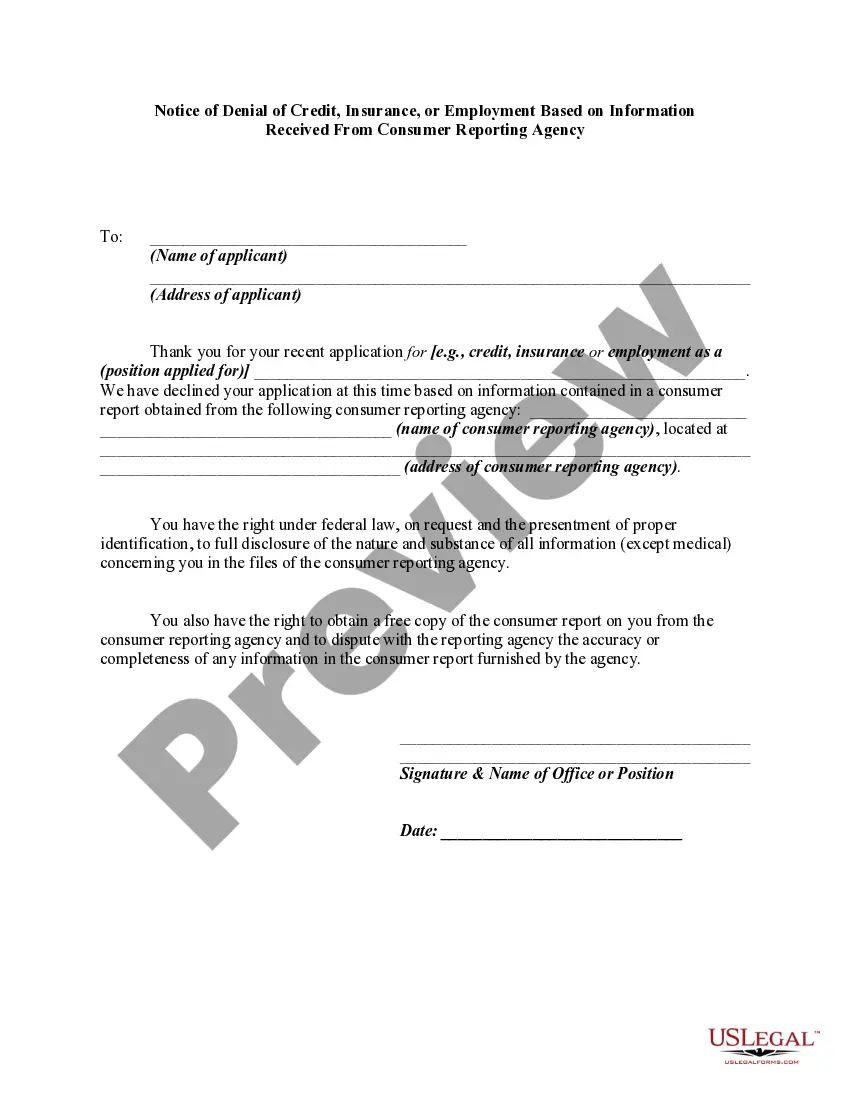

- Name and address of the creditor.

- Date of the letter.

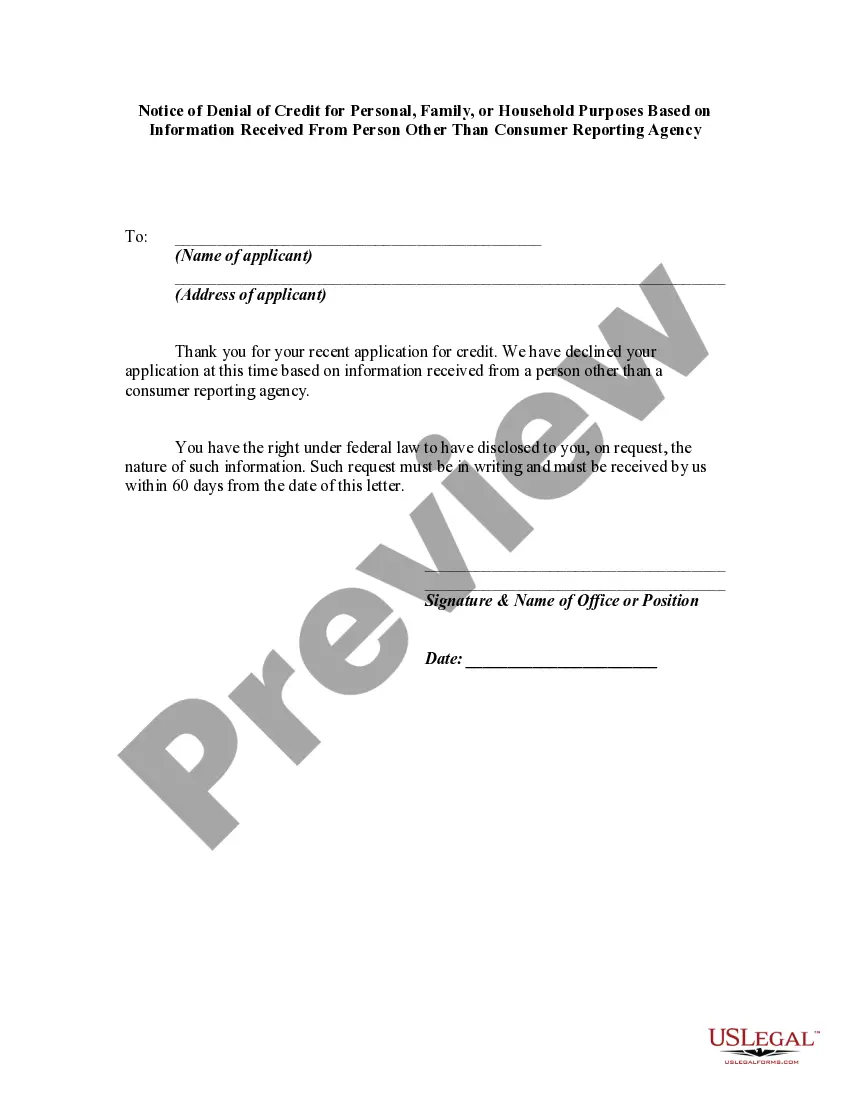

- Details of the credit application and its outcome.

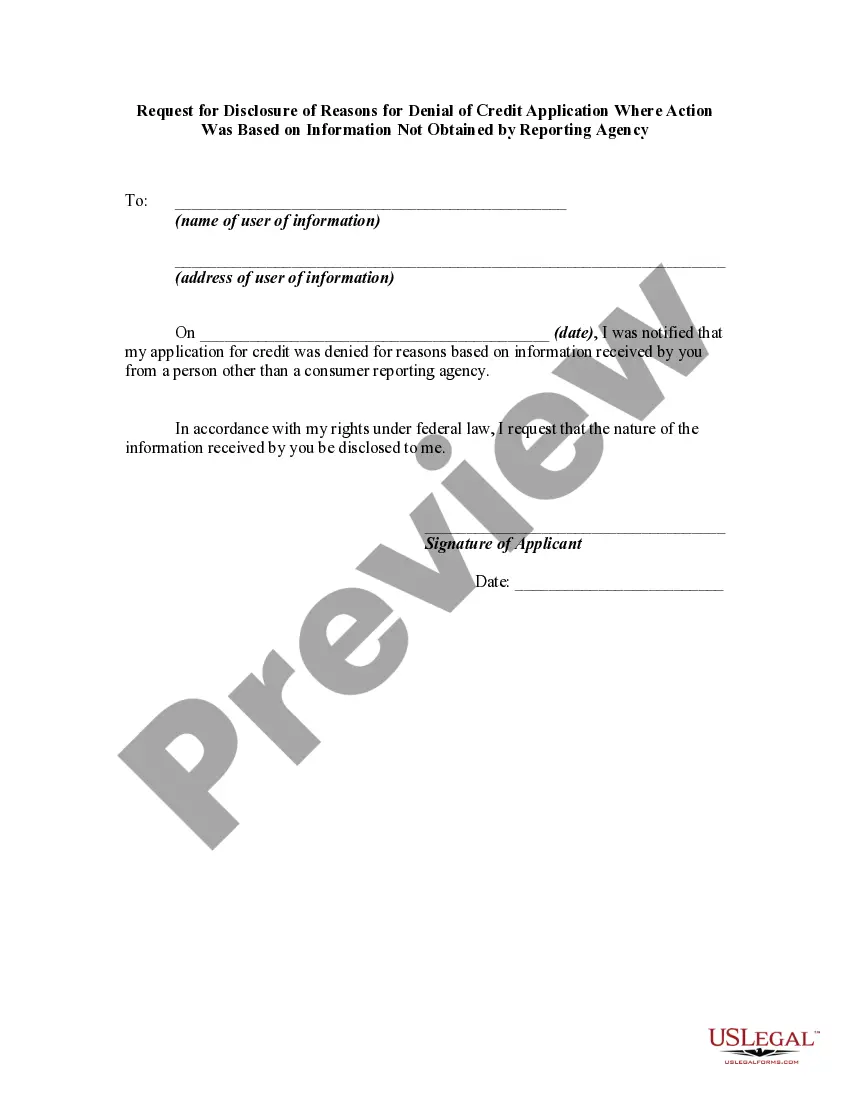

- Information on how to request a statement of reasons for the denial.

- Contact details of the consumer reporting agency used.

- Notice of consumer rights under the Equal Credit Opportunity Act.

Common use cases

This form should be used when a creditor denies a consumer's application for credit, insurance, or employment based on information from a consumer report. It ensures compliance with legal requirements to notify the consumer of their rights and the reasons for the denial.

Who should use this form

- Creditors who handle consumer credit applications.

- Any financial institutions that use consumer reports for decision-making.

- Employers who deny job applications based on consumer report information.

- Insurance companies that decline applications based on consumer reports.

Completing this form step by step

- Fill in the name and address of your organization at the top of the letter.

- Insert the date on which you are sending the letter.

- Specify the type of credit for which the application was submitted.

- Clearly state the reason for denial and offer a point of contact for further information.

- Provide the name, address, and contact number of the consumer reporting agency.

- Include the necessary signature and title of the person sending the letter.

Notarization guidance

This form does not typically require notarization to be legally valid. However, some jurisdictions or document types may still require it. US Legal Forms provides secure online notarization powered by Notarize, available 24/7 for added convenience.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Common mistakes to avoid

- Failing to include the consumer reporting agency's contact information.

- Not specifying the reasons for the denial clearly enough.

- Neglecting to inform the consumer about their rights under federal law.

- Sending the letter without the required signature, making it unofficial.

Benefits of using this form online

- Convenient access to a professionally drafted legal document.

- Editability allows for customization to fit your specific needs.

- Reliability, as the form is created by licensed attorneys compliant with federal regulations.

- Quick download ensures you can act promptly in notifying consumers.

Legal use & context

- This letter fulfills legal obligations under the Fair Credit Reporting Act and Equal Credit Opportunity Act.

- It offers consumers transparency regarding the reasons for denial and their legal rights.

- Proper use of this form helps protect creditors from potential legal claims of discrimination.

What to keep in mind

- This form is essential for notifying applicants of adverse credit decisions.

- It informs consumers of their rights to dispute inaccuracies in their consumer reports.

- Using this form ensures compliance with federal laws regarding credit denial notifications.

Looking for another form?

Form popularity

FAQ

Prohibits creditors from discriminating against credit applicants on the basis of race, color, religion, national origin, sex, marital status, age, because an applicant receives income from a public assistance program, or because an applicant has in good faith exercised any right under the Consumer Credit Protection

The Federal Trade Commission (FTC), the nation's consumer protection agency, enforces the Equal Credit Opportunity Act (ECOA), which prohibits credit discrimination on the basis of race, color, religion, national origin, sex, marital status, age, or because you get public assistance.

When you apply for a loan or credit card, the ECOA gives you certain rights.You have the right to keep your accounts after you change your name, marital status, reach a certain age, or retire, unless the creditor has evidence that you're not willing or able to pay.

It prohibits credit discrimination on the basis of race, color, religion, national origin, sex, marital status, age or because a person receives public assistance in whole or in part. It also makes it unlawful to discriminate against anyone who has exercised any rights under the Consumer Credit Protection Act.

ECOA Notice is a disclosure statement that a lender, under certain circumstances, is required to send to a person who requests for an extension of credit.ECOA stands for Equal Credit Opportunity Act and is one of the key fair lending and consumer protection legislation.

This Act (Title VII of the Consumer Credit Protection Act) prohibits discrimination on the basis of race, color, religion, national origin, sex, marital status, age, receipt of public assistance, or good faith exercise of any rights under the Consumer Credit Protection Act.

The Federal Trade Commission (FTC), the nation's consumer protection agency, enforces the Equal Credit Opportunity Act (ECOA), which prohibits credit discrimination on the basis of race, color, religion, national origin, sex, marital status, age, or because you get public assistance.

Adverse action notices under the ECOA and Regulation B are designed to help consumers and businesses by providing transparency to the credit underwriting process and protecting against potential credit discrimination by requiring creditors to explain the reasons adverse action was taken.

The Equal Credit Opportunity Act (ECOA), 15 U.S.C. § 1691 et seq. , which is implemented by Regulation B (12 CFR Part 1002 ), applies to all creditors, including credit unions. When originally enacted, ECOA gave the Federal Reserve Board responsibility for prescribing the implementing regulation.