Account Stated between Partners

What this document covers

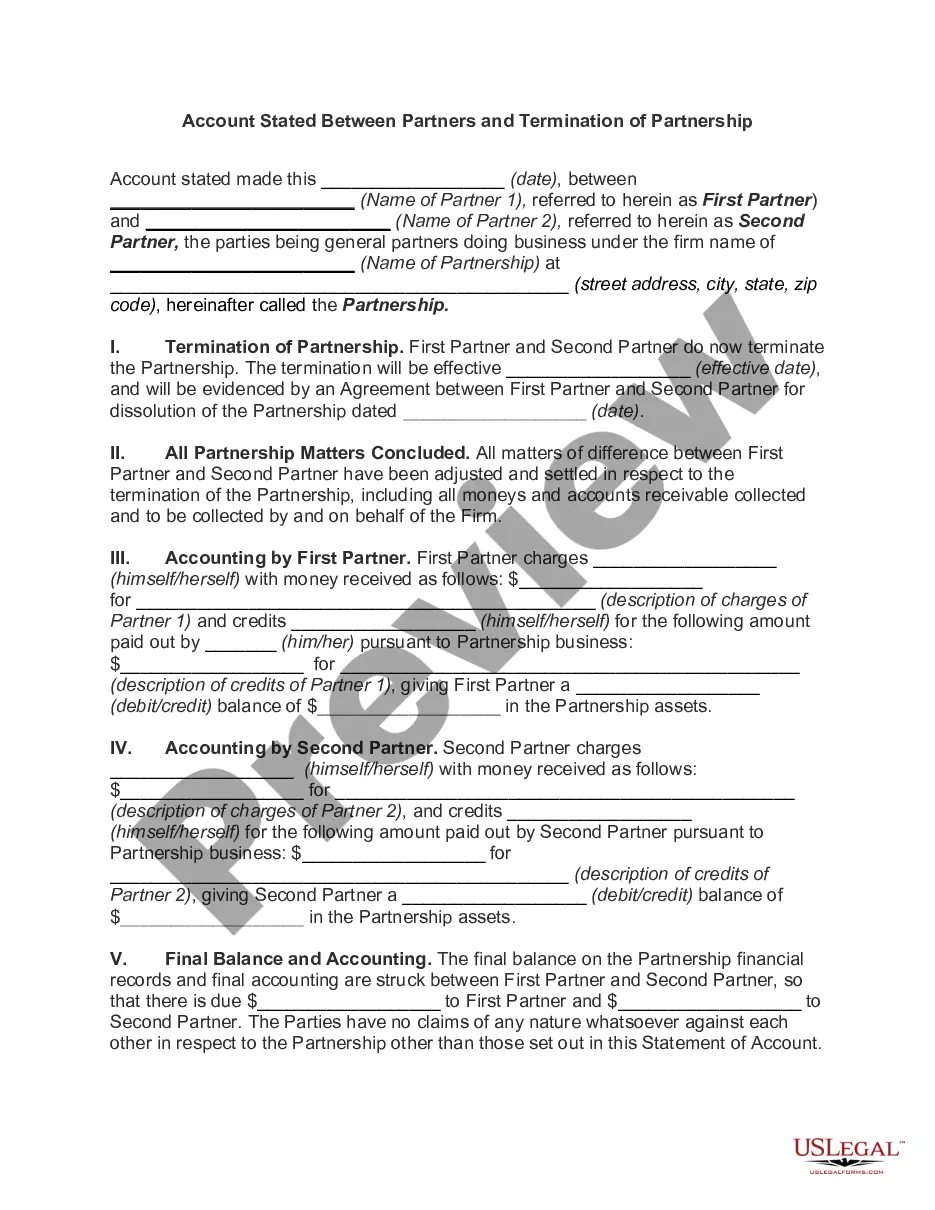

The Account Stated between Partners is a legal agreement that finalizes the financial relationship between two partners in a business partnership. It acknowledges the acceptance of an account's accuracy and confirms the balance owed by one partner to another. This form is essential for resolving any outstanding financial matters after the dissolution of a partnership, making it distinct from other general partnership agreements by focusing specifically on the settlement of accounts between the partners involved.

Main sections of this form

- Identification of the partners and the partnership's name and address.

- Effective date of partnership termination.

- Provisions for settling all accounts receivable and payable between partners.

- Final accounting details including balances owed or credits due.

- Governing law applicable to the agreement.

- Mandatory arbitration clause for resolving disputes.

Common use cases

This form should be used when partners decide to dissolve their business partnership and need to settle their financial obligations. It is applicable after all business matters have been settled, ensuring that any outstanding debts or credits between the partners are documented and agreed upon, preventing future disputes.

Who should use this form

This form is intended for:

- Business partners who are dissolving their partnership.

- Individuals seeking to document the final financial transactions between partners.

- Corporations or LLCs that operated as partnerships and need formal closure on their financial accounts.

Completing this form step by step

- Identify and fill in the names of the partners and the partnership.

- Enter the effective date for the termination of the partnership.

- Document any financial adjustments and provide detailed accounting of owed amounts.

- Ensure that both partners review the final balance and make any necessary corrections.

- Obtain the signatures of both partners to validate the agreement.

Is notarization required?

This form does not typically require notarization unless specified by local law. However, it is advisable to check state-specific regulations to ensure compliance and enforceability.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Mistakes to watch out for

- Failing to include all outstanding debts or credits, which can lead to disputes later.

- Not specifying the effective date of termination clearly.

- Neglecting to obtain signatures from both partners, making the agreement unenforceable.

- Forgetting to update any business stationery or documentation to reflect the dissolution of the partnership.

Benefits of using this form online

- Convenient access to a professionally drafted legal document tailored for partnerships.

- Editable format allows you to customize the agreement to fit your specific situation.

- Immediate download ensures you can finalize your partnership termination without delay.

- Complying with legal standards provides peace of mind for all parties involved.

Main things to remember

- The Account Stated between Partners serves to finalize financial relations after a partnership ends.

- Clear documentation of all financial obligations is critical to prevent future disputes.

- Both partners must review and sign the agreement to ensure it is legally binding.

Looking for another form?

Form popularity

FAQ

?An account stated has been defined as an agreement between parties who have had previous transactions that the account representing those transactions is true and that the balance stated is correct, together with a promise, express or implied, for the payment of such balance." "An account stated is merely a form of

12) How is Account Stated different from a breach of contract? An Account Stated establishes an implied contract whereas breach of contract traditionally refers to an expressly written contract. Account Stated is used when no contract exists, or when the plaintiff cannot prove the existence of the contract.

The elements of account stated are: (1) prior transactions between the parties which establish a debtor-creditor relationship; (2)an express or implied agreement between the parties as to the amount due; and (3) an express or implied promise from the debtor to pay the amount due.

Essentially, an account stated is a new contract under which the parties to prior transactions agree to a new balance due. 6. Thus, a claim for an account stated is based not on the original transactions between the parties, but on the new, agreed upon contractual balance.

Collections actions involving the sale of goods often include two varieties of ?account? claims in addition to traditional breach of contract theories: ?account stated? and ?open account.? Generally, an account stated claim alleges the failure to pay an agreed-upon balance, while an open account claim alleges an

Account stated refers to a document summarizing the amount a debtor owes a creditor. An account stated is also a cause of action in many states that allows a creditor to sue for payment.