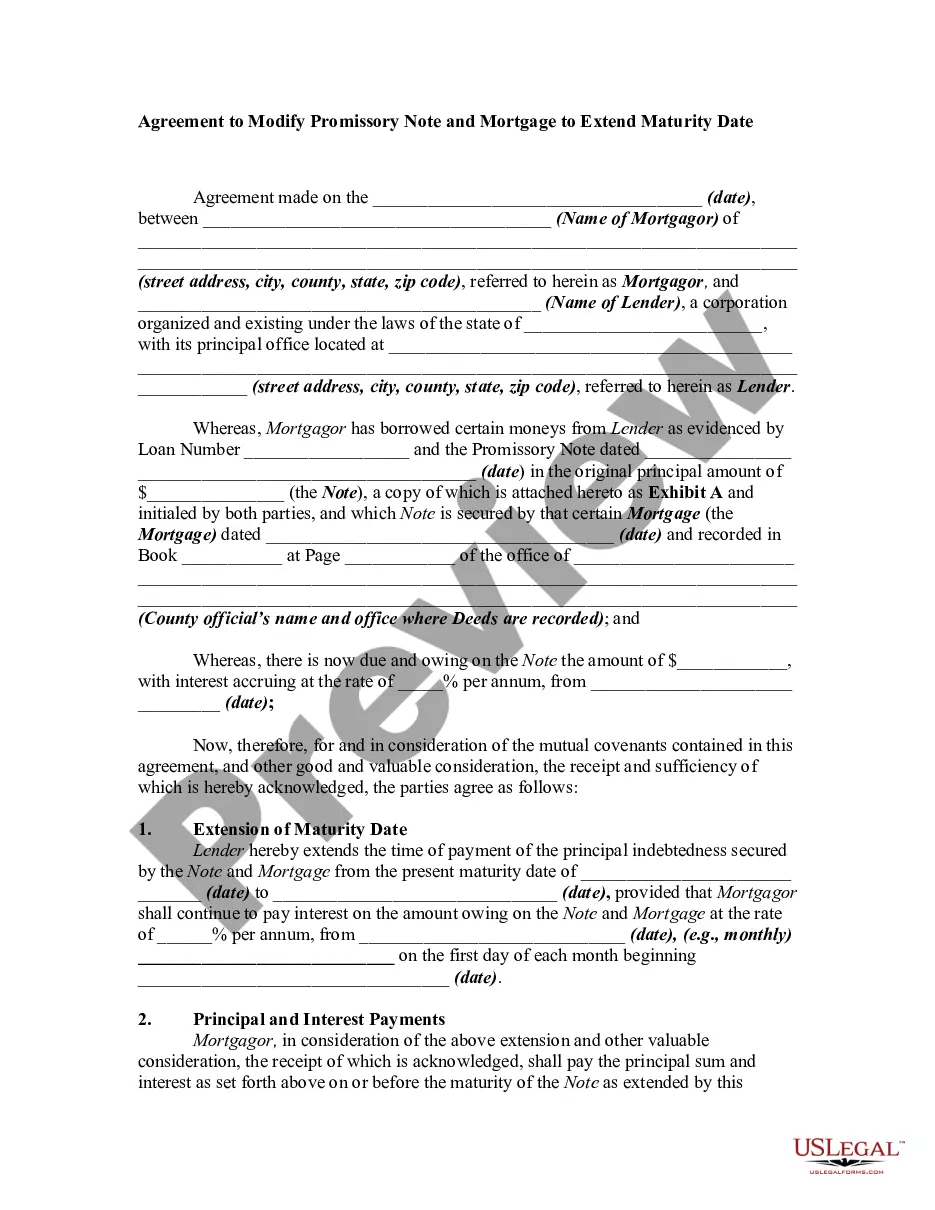

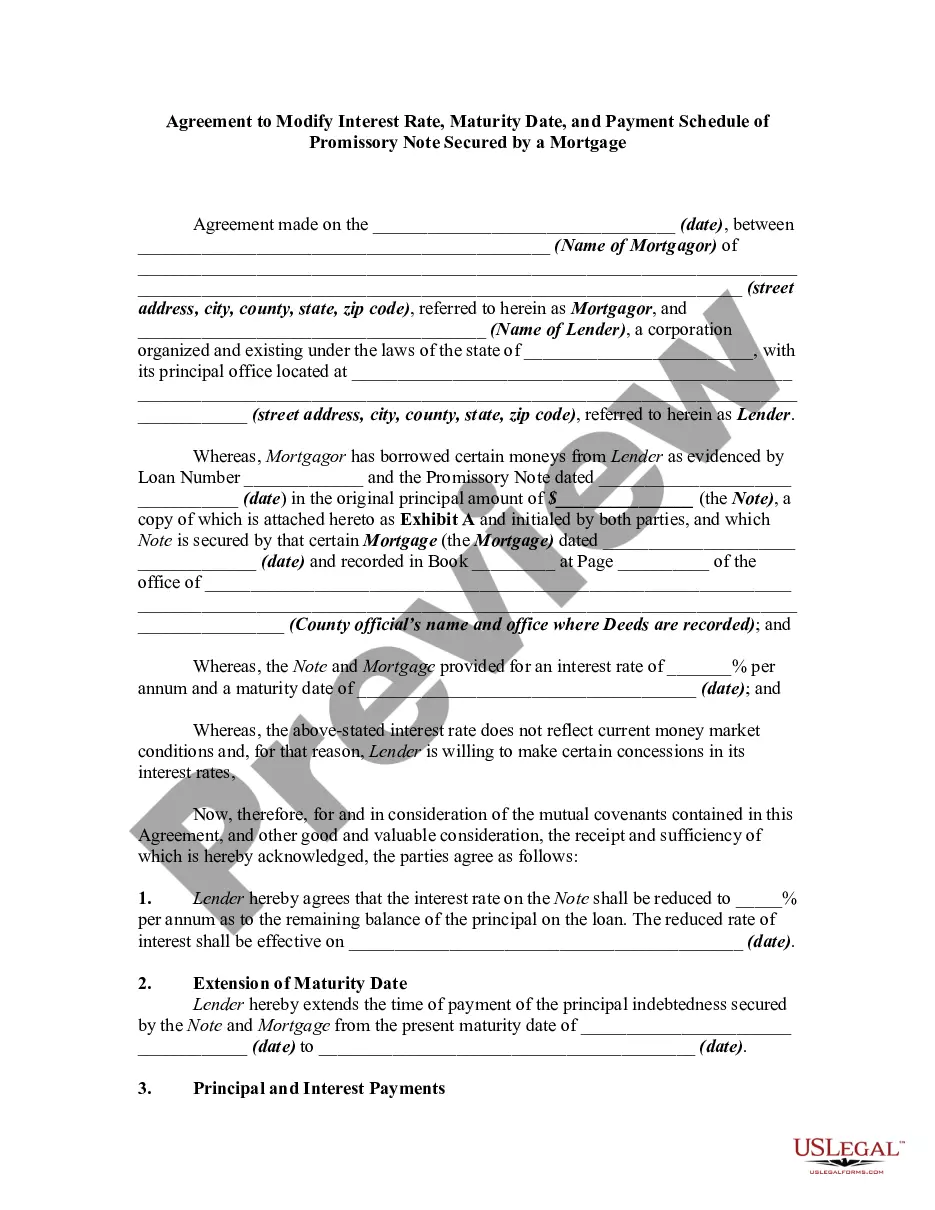

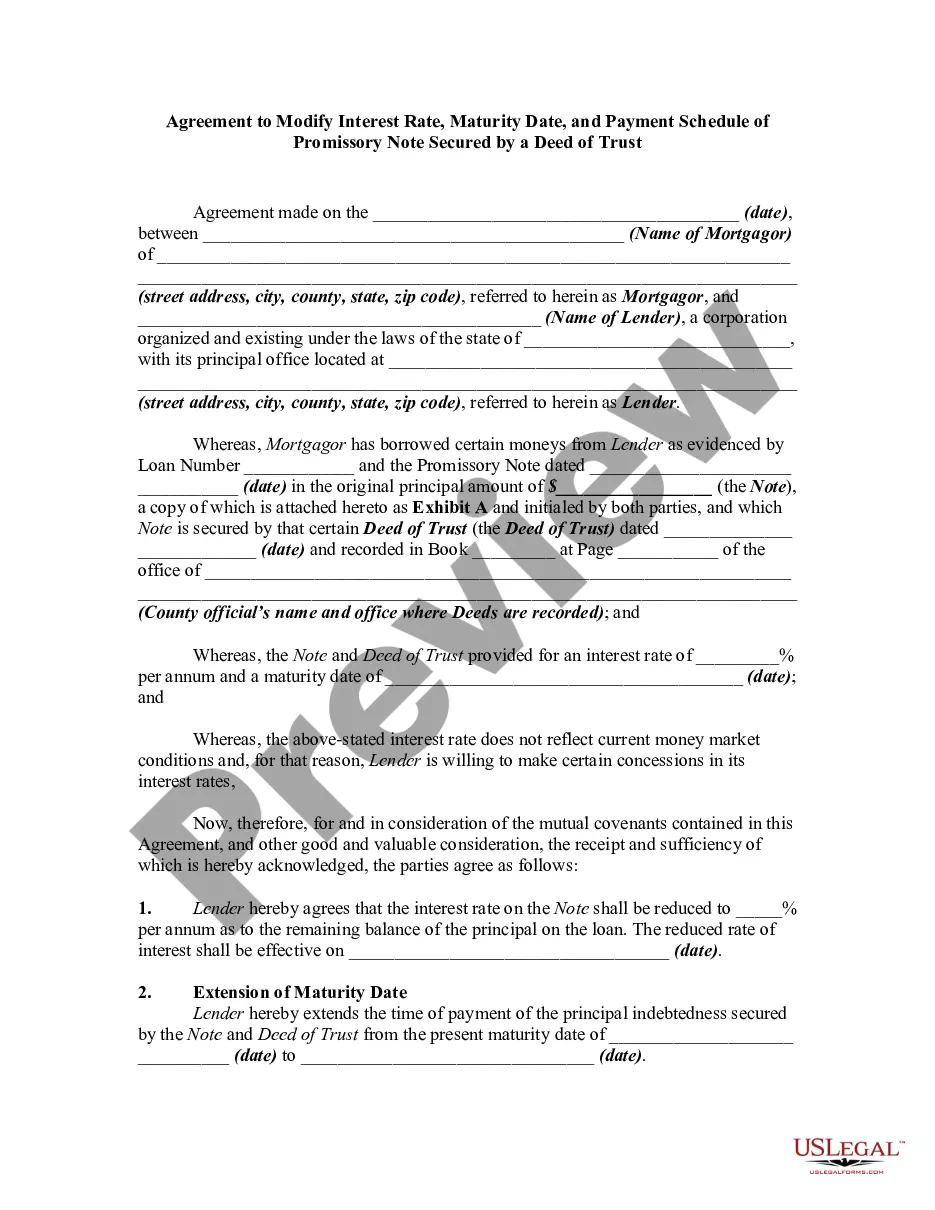

Agreement to Modify Interest Rate on Promissory Note Secured by a Mortgage

Overview of this form

The Agreement to Modify Interest Rate on Promissory Note Secured by a Mortgage is a legal document that modifies the terms of a loan agreement by adjusting the interest rate on the promissory note. It is essential for situations where the original interest rate no longer reflects current market conditions, allowing both the mortgagor and lender to reach an amicable agreement. This form ensures both parties consent to the new terms and protects their rights under the revised agreement.

Key components of this form

- Date of agreement and names of the parties involved

- Loan number and details of the original promissory note

- Original interest rate and the new modified interest rate

- Effective date of the new interest rate

- Disclaimer stating that other terms remain unchanged

- Governing law and notice provisions

Common use cases

This form should be used in circumstances where a lender agrees to lower the interest rate on a promissory note secured by a mortgage to better align with current economic conditions. It is useful for borrowers seeking financial relief and for lenders looking to maintain a good relationship with their clients while still ensuring they are compensated fairly for their loans.

Who can use this document

- Mortgagors (borrowers) seeking a reduction in their loan's interest rate

- Lenders who are open to revising loan terms for customer retention

- Attorneys preparing legal documents related to mortgage modifications

Completing this form step by step

- Identify and enter the date of the agreement.

- Fill in the names and addresses of both the mortgagor and lender.

- Specify the loan number and attach a copy of the original promissory note.

- Indicate the previous and new interest rates, including the effective date of the new rate.

- Have both parties sign and date the agreement, and ensure all signatures are notarized if required.

Notarization requirements for this form

This document requires notarization to meet legal standards. US Legal Forms provides secure online notarization powered by Notarize, allowing you to complete the process through a verified video call, available 24/7.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Avoid these common issues

- Failing to include the effective date of the new interest rate.

- Not having both parties sign the agreement.

- Neglecting to record the document with the local register of deeds.

Why complete this form online

- Easy access to a customizable template designed by licensed attorneys.

- Quick downloading and editing to fit specific needs.

- Convenient options for digital storage and sharing.

Legal use & context

- The modification agreement is legally binding once signed and notarized.

- Both parties must adhere to the modified terms to maintain enforceability.

- Understanding state-specific laws related to mortgage agreements is essential for compliance.

Main things to remember

- The form allows modification of the interest rate on a secured loan.

- It requires signatures from both the lender and the borrower.

- Notarization is necessary for the document to be legally recognized.

Looking for another form?

Form popularity

FAQ

If your modification is temporary, you'll likely need to return to the original terms of your mortgage and repay the amount that was deferred before you can qualify for a new purchase or refinance loan.

When you take a loan modification, you change the terms of your loan directly through your lender. Most lenders agree to modifications only if you're at immediate risk of foreclosure. A loan modification can also help you change the terms of your loan if your home loan is underwater.

Starting the Document. Write the date at the top of the page. Write the Terms of the Loan. State the purpose of the personal payment agreement and the terms for returning the money. Date the Document. Statement of Agreement. Sign the Document. Record the Document.

The Promissory Note is hereby modified and amended by deleting the last sentence of the first paragraph of the Promissory Note in its entirety, and replacing it with the following: All outstanding principal and interest shall be due and payable on June 3, 2012 (the Due Date).

You have to be suffering a financial hardship. You have to show you cannot afford your current mortgage payments. You have to be able to show that you can stay current on a modified payment schedule.

To secure a promissory note means that you identify some specific property and attach it to the note. Then, if the borrower defaults on the loan, you will be able to repossess the collateral as compensation for the loan.

Either way, it stays on your report for seven years.

The Loan shall be evidenced and governed by a new promissory note (the New Note) which amends and restates in its entirety, but does not extinguish, the Note. Anything to the contrary notwithstanding, if any inconsistency exists between the Loan Agreement and the New Note, the New Note shall control.

Loan modification is when a lender agrees to alter the terms of a homeowner's mortgage to help them avoid default and keep their house during times of financial hardship. The goal of a mortgage loan modification is to reduce the borrower's payments so they can afford their loan month-to-month.