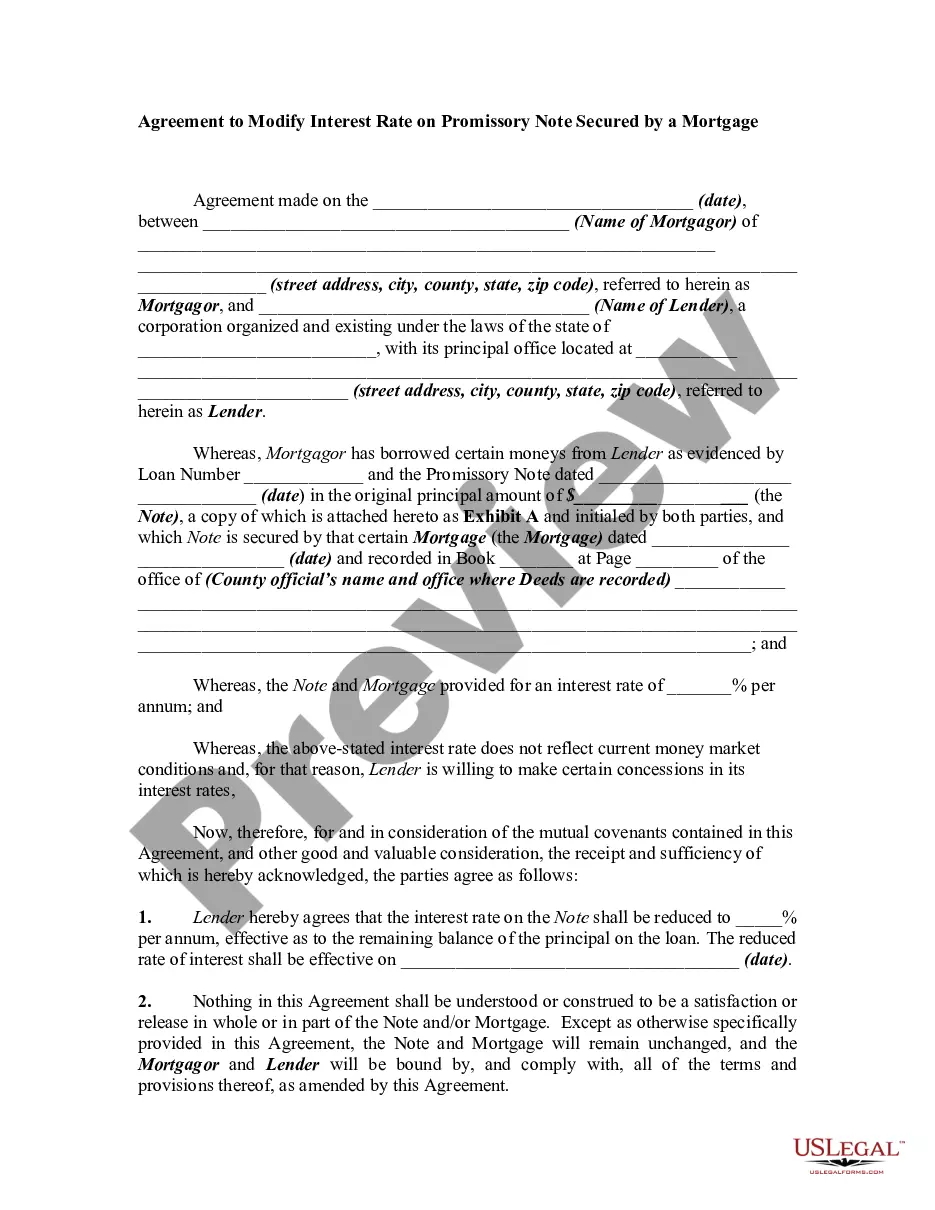

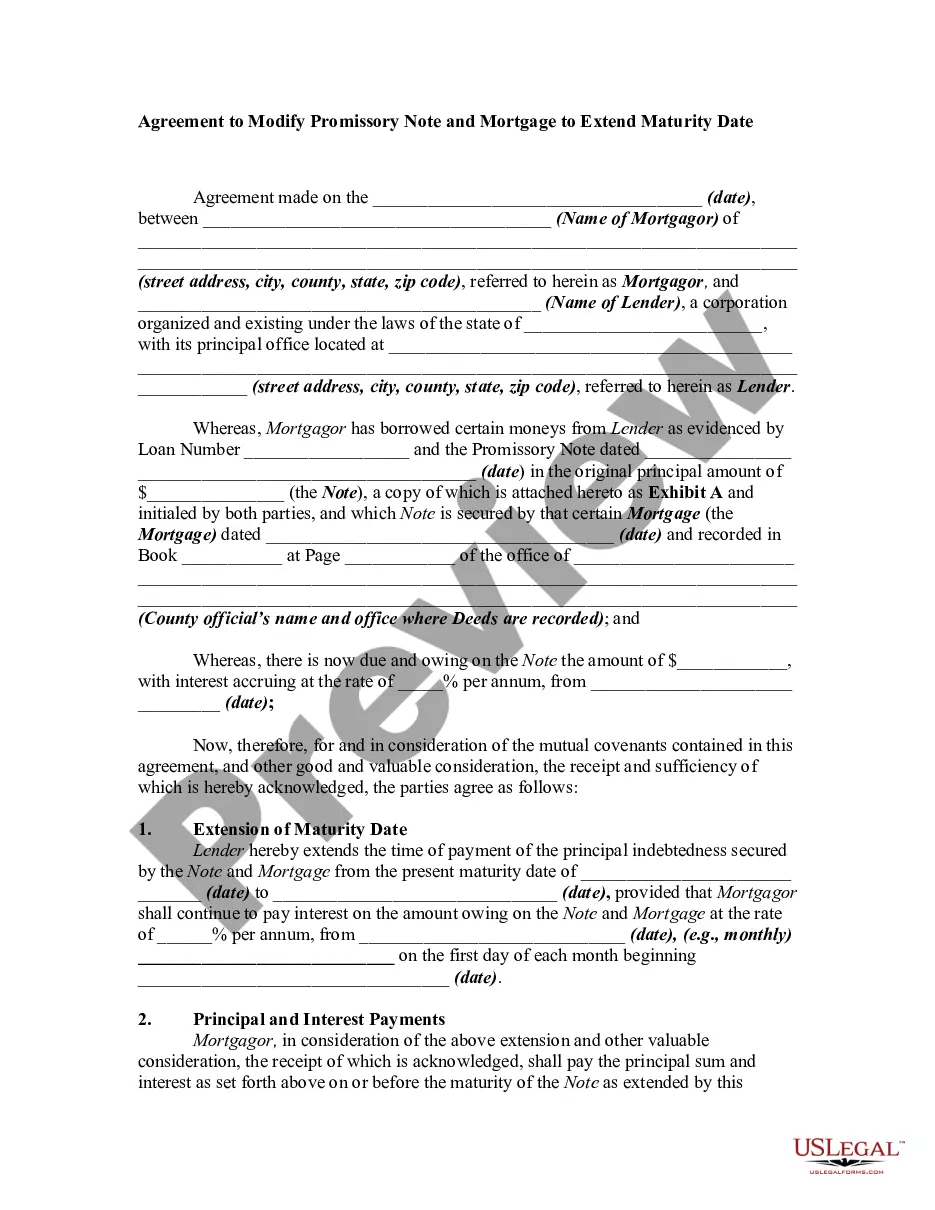

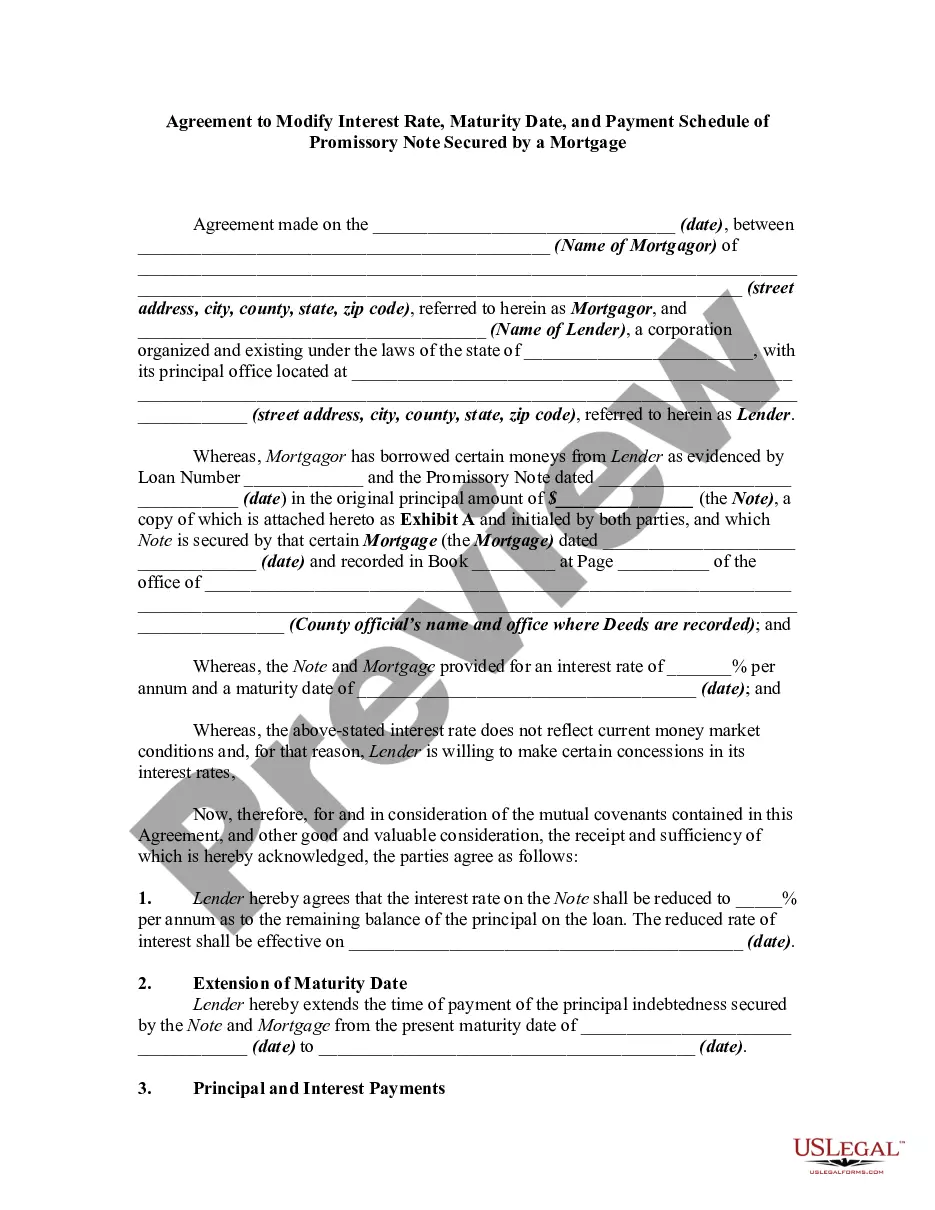

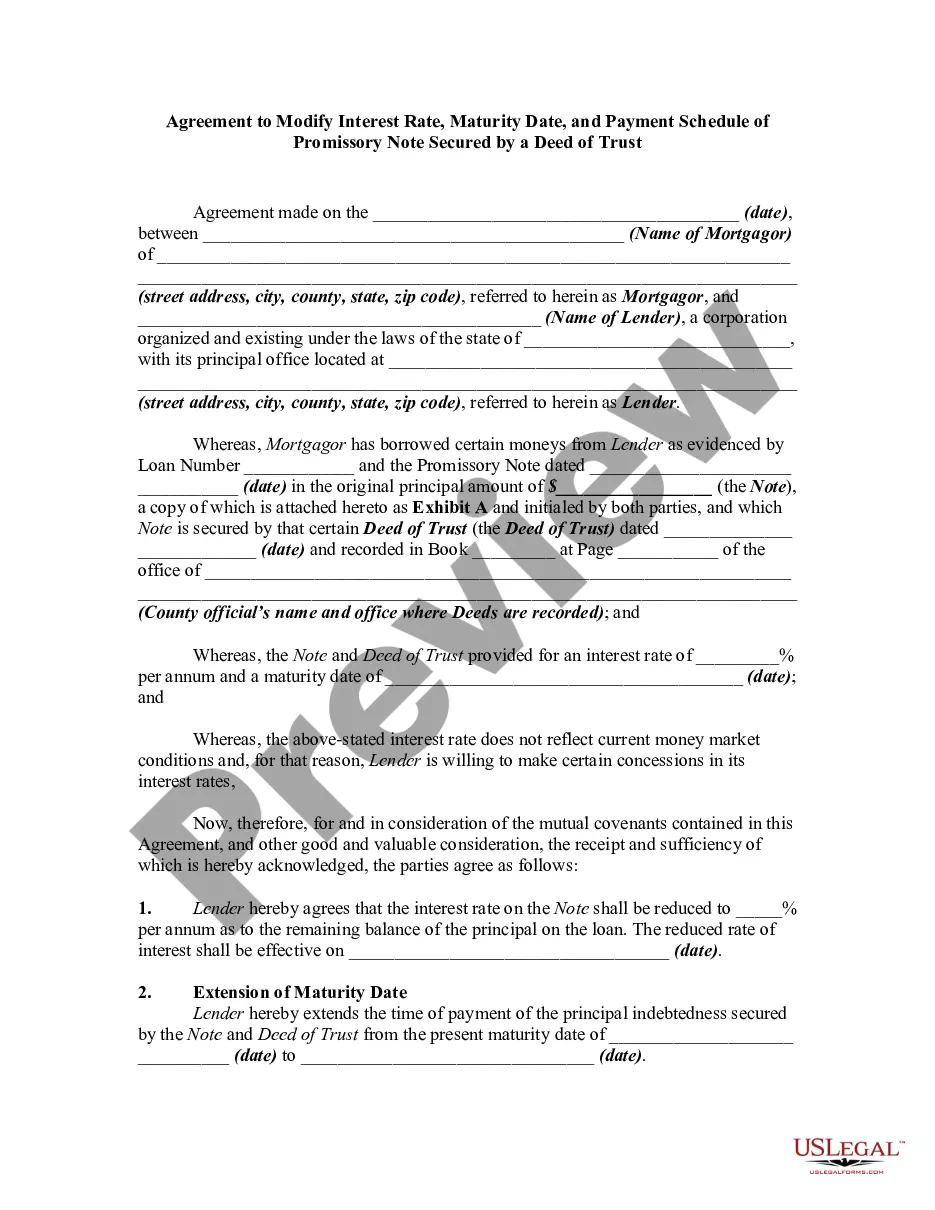

Agreement to Modify Promissory Note Secured by a Mortgage

About this form

The Agreement to Modify Promissory Note Secured by a Mortgage is a legal document that allows parties to modify the terms of an existing loan agreement and mortgage. This form sets out new interest rates, payment schedules, and other pertinent details related to the loan. Unlike a standard promissory note or mortgage, this agreement specifically addresses changes to an already existing loan, making it crucial when market conditions or financial situations require adjustments.

Key components of this form

- Identification of the mortgagor (borrower) and lender, including their addresses.

- The original promissory note details, including loan number and principal amount.

- New interest rate and updated maturity date of the loan.

- Details on monthly installment payments and their due dates.

- Clauses stating that the original mortgage is not satisfied nor released.

- Governing law and notice provisions for both parties.

Common use cases

This form is used when the mortgagor and lender agree to change the terms of a loan secured by a mortgage. Common scenarios include cases where interest rates have decreased, a borrower is experiencing financial hardship, or both parties wish to extend the repayment period. It is a necessary step to ensure that both parties have a clear understanding of the new terms as it pertains to the existing mortgage.

Who this form is for

- Borrowers (mortgagors) who wish to modify their existing mortgage terms.

- Lenders looking to accommodate borrowers in changing financial circumstances.

- Real estate attorneys or agents assisting clients in the loan modification process.

- Individuals or entities with a vested interest in the loan agreement, including co-signers or guarantors.

Instructions for completing this form

- Identify and enter the date of the agreement at the top of the document.

- Fill in the name and address of the mortgagor and the lender.

- Provide details about the existing promissory note and mortgage, including their original terms.

- Specify the new interest rate and the new maturity date for the loan.

- Outline the payment schedule, including the number and amount of monthly installments.

- Ensure both parties sign the document and have it notarized if required by state law.

Does this document require notarization?

To make this form legally binding, it must be notarized. Our online notarization service, powered by Notarize, lets you verify and sign documents remotely through an encrypted video session.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Avoid these common issues

- Failing to accurately update all relevant financial terms within the agreement.

- Not having both parties sign and date the document.

- Incorrectly identifying the original loan or mortgage details.

- Neglecting to notarize the form if required by state laws.

Why complete this form online

- Convenience of completing the form at any time from anywhere.

- Editability allows users to customize terms before finalizing.

- Access to templates prepared by licensed attorneys for accuracy and legality.

- Instant access to downloadable forms that can be printed and signed.

Looking for another form?

Form popularity

FAQ

The mortgage modification agreement is a legal document between a lender and borrower to change an existing loan's terms. A typical modification may include reducing the interest rate, extending the repayment term, lowering monthly payments, or even forgiving part of the debt.

Amendments to a promissory note may only be made with consent from the lender and will be considered binding by all parties involved. Amendments can be made for significant changes and should be done in a formal manner to minimize liability and confusion with the contract moving forward.

Secured promissory notes The property that secures a note is called collateral, which can be either real estate or personal property. A promissory note secured by collateral will need a second document. If the collateral is real property, there will be either a mortgage or a deed of trust.

True, The borrower signs a promissory note pledging to repay the debt and gives the lender a mortgage, which is security for the property. When a property is mortgaged, the owner must execute both a promissory note and a security instrument.

A home mortgage secures a promissory note with the title to the property as collateral. This is done in case the lender ever needs to foreclose and sell the property because the homeowner did not make loan payments. Your lender will keep the original promissory note until your loan is paid off.

A promissory note is a document between the lender and the borrower in which the borrower promises to pay back the lender, it is a separate contract from the mortgage. The mortgage is a legal document that ties or "secures" a piece of real estate to an obligation to repay money.

A home mortgage secures a promissory note with the title to the property as collateral. This is done in case the lender ever needs to foreclose and sell the property because the homeowner did not make loan payments. Your lender will keep the original promissory note until your loan is paid off.

Promissory notes can be secured using a financing statement, deed of trust, or a mortgage. If a promissory note includes these terms, then it is a secured promissory note. So, the inclusion of collateral is the only real difference between secured promissory notes and unsecured promissory notes.