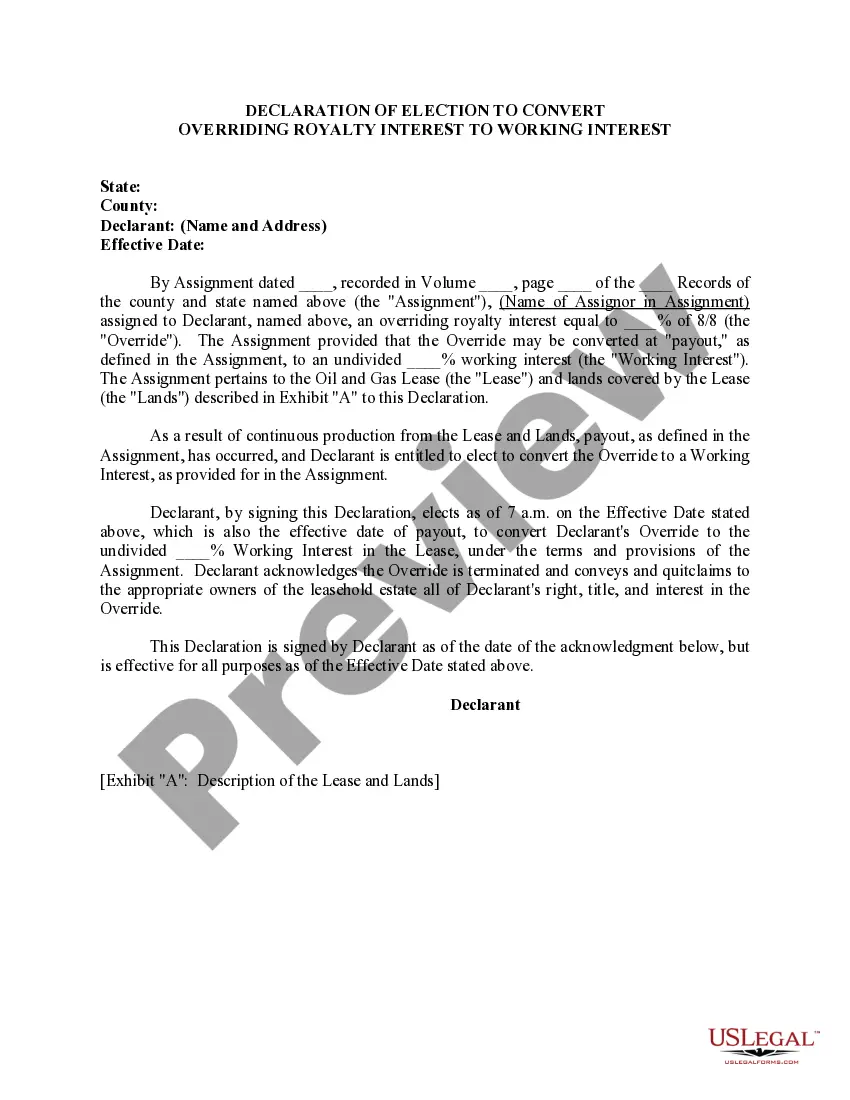

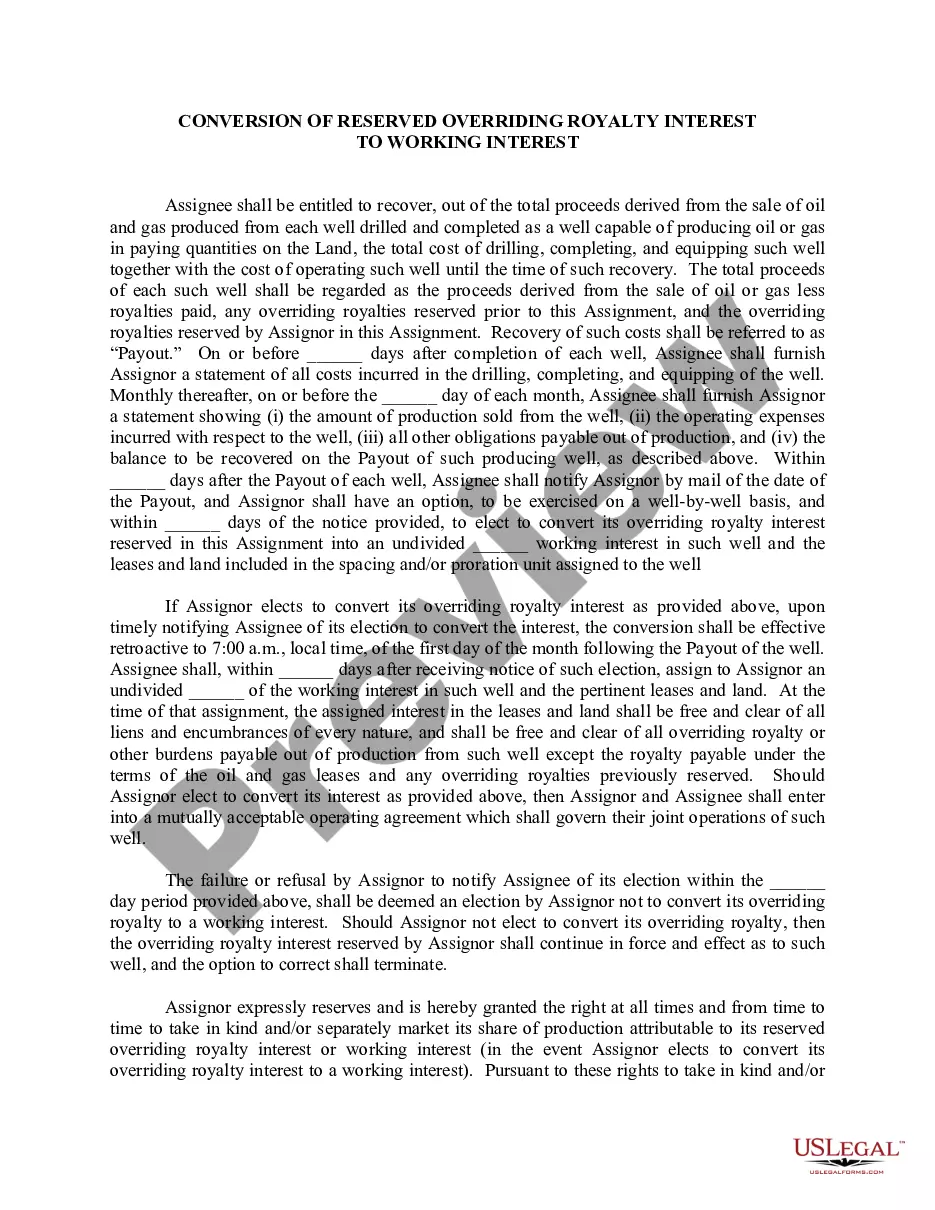

Declaration of Election by Lessor to Convert Royalty Interest to Working Interest

About this form

The Declaration of Election by Lessor to Convert Royalty Interest to Working Interest is a legal document used by lessors to convert a reserved royalty interest to a working interest in an oil and gas lease. This form specifies the decision to convert a portion of the royalty interest to an undivided working interest once payout has been achieved, as defined within the lease. This form is essential for lessors who wish to formalize their election to convert interests, ensuring clarity and legal validity in the arrangement with lessees.

Key parts of this document

- Declarant information: Name and address of the lessor.

- Lease details: Information about the original oil and gas lease, including date and recording details.

- Royalty interest: Specification of the reserved fraction or percentage royalty interest.

- Working interest election: Declaration of the portion of the royalty interest being converted to a working interest.

- Effective date: The date this declaration is effective for all purposes.

- Acknowledgment clause: An acknowledgment of reduction in royalty payments post-conversion.

Situations where this form applies

This form should be used when the declarant, as the lessor, wishes to formally elect to convert a reserved royalty interest to a working interest, following the occurrence of payout as detailed in the original lease. It is typically utilized after continuous production has occurred on the leased land, allowing the lessor to benefit from a working interest in addition to the royalty interest they initially reserved.

Who needs this form

- Lessees who are parties to an oil and gas lease and have reserved royalty interests.

- Property owners who wish to convert their interests following payout.

- Legal representatives acting on behalf of lessors needing to document this conversion.

Completing this form step by step

- Identify the parties involved: Write the names and addresses of the declarant and lessee.

- Provide lease details: Enter the date of the original lease and its recording information.

- Specify the royalty interest: Indicate the fraction or percentage of the royalty interest reserved.

- Declare your election: Clearly state the portion of royalty interest being converted to a working interest.

- Set the effective date: Provide the date the declaration will take effect.

- Sign and date the declaration: Ensure all parties sign the document.

Notarization guidance

Notarization is generally not required for this form. However, certain states or situations might demand it. You can complete notarization online through US Legal Forms, powered by Notarize, using a verified video call available anytime.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Typical mistakes to avoid

- Failing to enter the correct lease recording details.

- Not specifying the correct fraction or percentage for both royalty and working interest.

- Overlooking to provide an effective date or mistakenly using the wrong date.

- Not having all necessary signatures on the form.

Why complete this form online

- Convenience: Download and complete the form at your own pace without needing to visit a law office.

- Editability: Easily make changes as needed, ensuring accuracy before submission.

- Reliable guidance: Access forms created by licensed attorneys to ensure legal compliance.

Quick recap

- The form is essential for formally converting a royalty interest to a working interest in oil and gas leases.

- Ensure all details, including dates and signatures, are accurate for legal validity.

- Understand the implications of this conversion, such as changes in royalty payments.

Looking for another form?

Form popularity

FAQ

Since royalties count as taxable income, you must report royalties on your federal income tax return. Royalty income is listed line 17 of Form 1040. According to the Internal Revenue Service, you must generally fill out and attach Schedule E to your 1040 to report royalty income.

Royalties are reported to the owner of the property (either intellectual, artistic or real) in Box 2 of Form 1099-Misc.In this situation the royalty is an investment and not considered earned income. To Enter Royalty Income in TaxSlayer Pro, from the Main Menu of the Tax Return (Form 1040) select: Income Menu.

Net revenue is the amount that is shared among the property owners. To determine net revenue interest, multiply the royalty interest by the owner's shared interest. For example, if you have a 5/16 royalty, your net royalty interest would be 25% multiplied by 5/16, which equals 7.8125% calculated to four decimal places.

Usually long-term capital gains is usually related to a sale of property, if you receive income on this royalty each and every year, this is considered ordinary income that is not subject to capital gains consideration, unless this is a transfer of a patent.

Your decimal interest is calculated based on your royalty interest in the tract or unit on which the well is drilled.Or, you might own a non-participating royalty equal to 1/16 of the royalty reserved in any lease of the lands in the unit (a fraction of the royalty).

In most cases you report royalties on Schedule E (Form 1040), Supplemental Income and Loss. However, if you hold an operating oil, gas, or mineral interest or are in business as a self-employed writer, inventor, artist, etc., report your income and expenses on Schedule C or Schedule C-EZ (Form 1040).

The working interest would be reported on a Schedule C for the gross receipts, expenses and depletion. The taxpayer will receive the gross receipts (including lease and bonus payments) on Form 1099-MISC, Box 7, Nonemployee Compensation.

Royalty Interest an ownership in production that bears no cost in production. Royalty interest owners receive their share of production revenue before the working interest owners. Working Interest an ownership in a well that bears 100% of the cost of production.

Use this formula to calculate your decimal share of royalties from the producing well: (Mineral Interest Share) times (Royalty Rate) = (Royalty Share Decimal). Example 1: (1/3 x 100% mineral interest) times (1/8 Royalty Rate) = 1/3 x 1/8 = 1/24 = 0.04166667 RI.