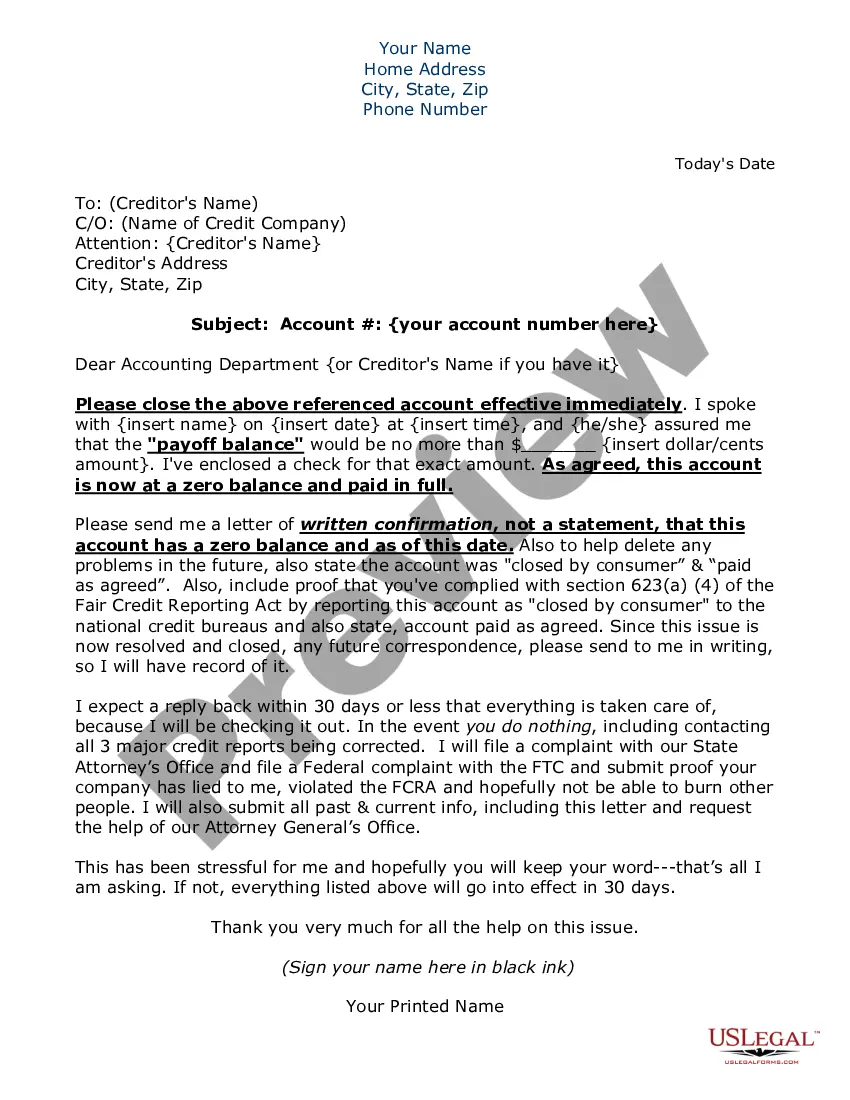

Statement to Add to Credit Report

Overview of this form

The Statement to Add to Credit Report is a legal document that allows consumers to add a brief statement to their credit file. This statement can explain disputes or discrepancies that were not resolved to the individual's satisfaction following a reinvestigation by a credit reporting agency. This form is particularly useful for consumers who want to ensure that potential lenders have a comprehensive understanding of their credit history, especially when negative information is present.

Key parts of this document

- Contact information of the credit reporting agency, including name, address, and phone number.

- A section to specify the creditor and related account information.

- A statement section where the consumer can briefly explain their dispute, limited to 100 words.

- A request for confirmation of the updated credit report after the statement has been added.

- A signature line for the consumer's signature and printed name.

When to use this form

This form should be used when you have filed a dispute with a credit reporting agency and the results of their reinvestigation did not resolve the issue to your satisfaction. It is appropriate to submit this statement to clarify your position on any inaccuracies or discrepancies in your credit report that could affect your creditworthiness.

Intended users of this form

- Consumers who notice inaccuracies in their credit reports.

- Individuals who have disputed an item on their credit report and received an unsatisfactory outcome.

- Anyone seeking to provide additional context regarding their credit history to potential creditors.

How to prepare this document

- Begin by filling in the name of the person you spoke to and the credit reporting agency's details.

- Specify the creditor and account details that relate to your dispute.

- Craft a concise statement (100 words or less) that clearly outlines the nature of your dispute.

- Sign and print your name as well as include your mailing address.

- Request a copy of the updated credit report for your records.

Does this form need to be notarized?

This form does not typically require notarization unless specified by local law. It is advisable to verify local regulations to ensure it meets legal standards in your jurisdiction.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Mistakes to watch out for

- Not keeping the statement within the 100-word limit.

- Failing to provide accurate contact information for the credit reporting agency.

- Neglecting to sign the form, which may lead to rejection.

- Omitting a request for confirmation of the updated credit report.

Benefits of completing this form online

- Instant access to a professionally drafted template that ensures legal compliance.

- Easily editable to reflect your specific circumstances and needs.

- Convenience of downloading and submitting without the need for in-person appointments.

Legal use & context

- The FCRA allows consumers to add a statement of dispute to their credit report as a means to ensure fairness in credit reporting.

- This statement provides context for creditors and may influence lending decisions.

Summary of main points

- The Statement to Add to Credit Report is essential for consumers seeking to clarify disputes.

- This form must be completed carefully, adhering to word limits and accurate information.

- Providing a personal statement can improve understanding between you and potential creditors.

Looking for another form?

Form popularity

FAQ

In fact, an employer is on your report because you provided that information on an application for credit.When the information is shared, the credit reporting agency (Experian, TransUnion or Equifax) will attach the name of the company to the identification section of your credit report.

Generally, utility bills do not appear on a credit report unless they're delinquent and referred to a collection agency. If you have long-overdue bills, a utility company can send your account to a collection agency that can forward it to one or more of the credit bureaus.

Tell the credit reporting company, in writing, what information you think is inaccurate. Tell the information provider (that is, the person, company, or organization that provides information about you to a credit reporting company), in writing, that you dispute an item in your credit report.

Employers may check your credit report with your written permission when you apply for a job. They won't, however, have access to your credit score.You can still get a job with bad credit, but some employers may weigh your credit history more heavily for certain positions.

A personal statement is a section on your credit report that allows you to explain disputed derogatory information.

Yes, you can be denied a job because of bad credit in 39 states and the District of Columbia, while 11 states ban the practice in most cases.In fact, your credit report won't even necessarily be pulled during the application process. And if it is, the employer is required by law to get your written permission.

Key Takeaways. When you encounter a financial event that affects your credit, it normally takes 30 days or less from the close of the current billing cycle to see it on your credit report. Such an event may include a loan application, missed payment, or bankruptcy, for example.

Step 1 - Establish a Data Furnishers or Service Agreement with each Credit Bureau Repository (Equifax, Experian, TransUnion, Innovis) to which you will be reporting. Step 2 - All businesses reporting to the bureaus, must meet the minimum reporting requirements established by each Credit Bureau.

Your creditorsincluding your credit card issuer, loan issuer, utility provider, and landlordare not required to report to the credit bureaus.But if you pay your rent and utilities on time regularly, those payments could be helping you build your credit profile.