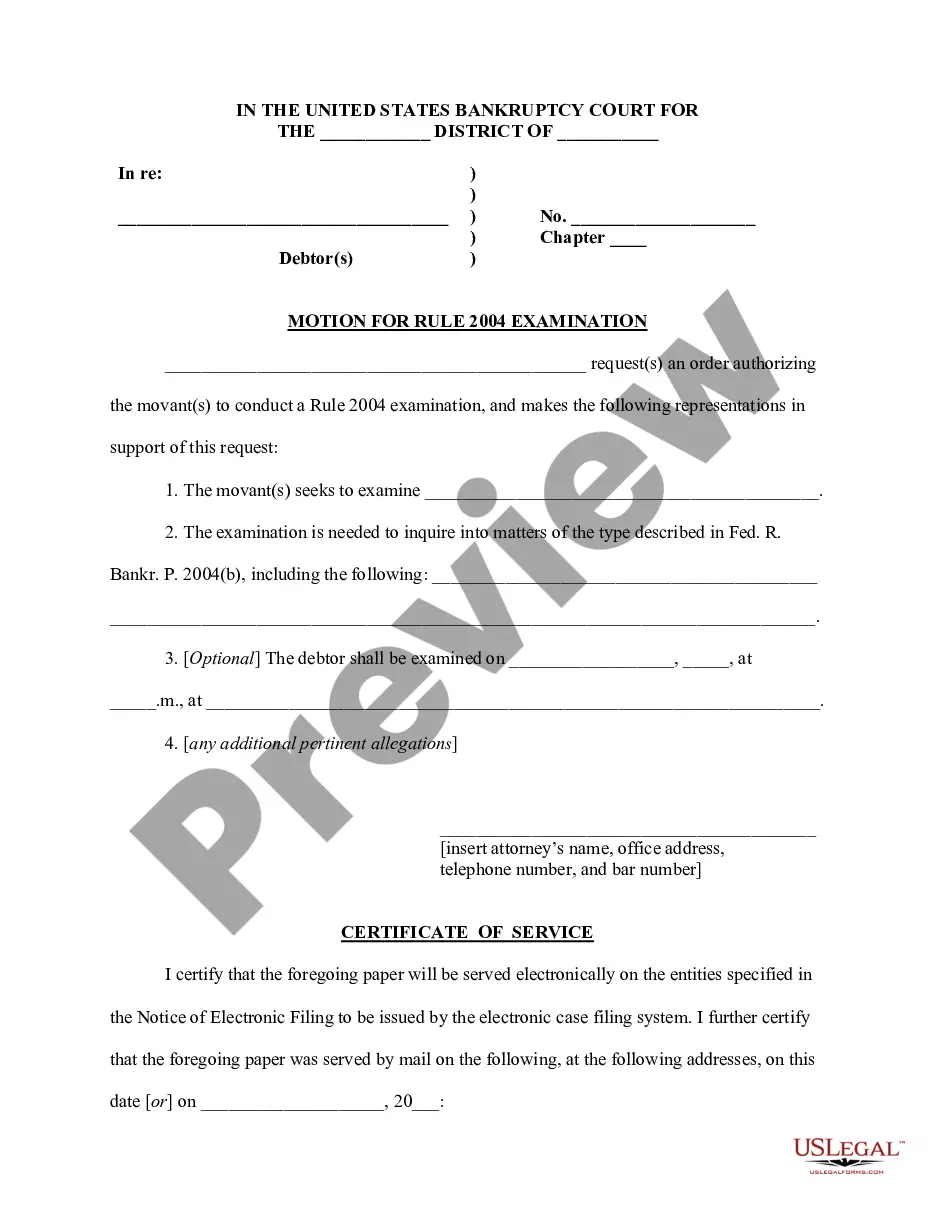

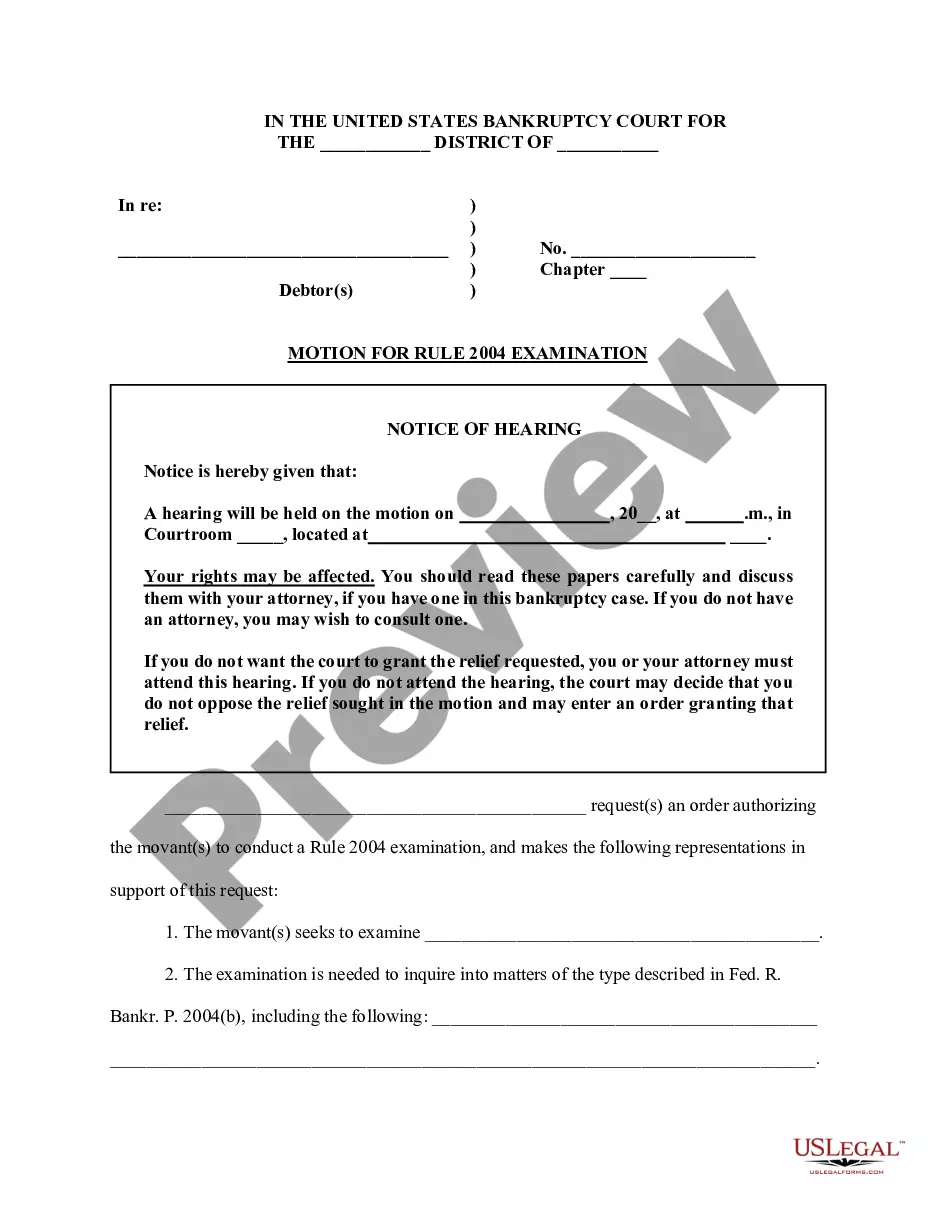

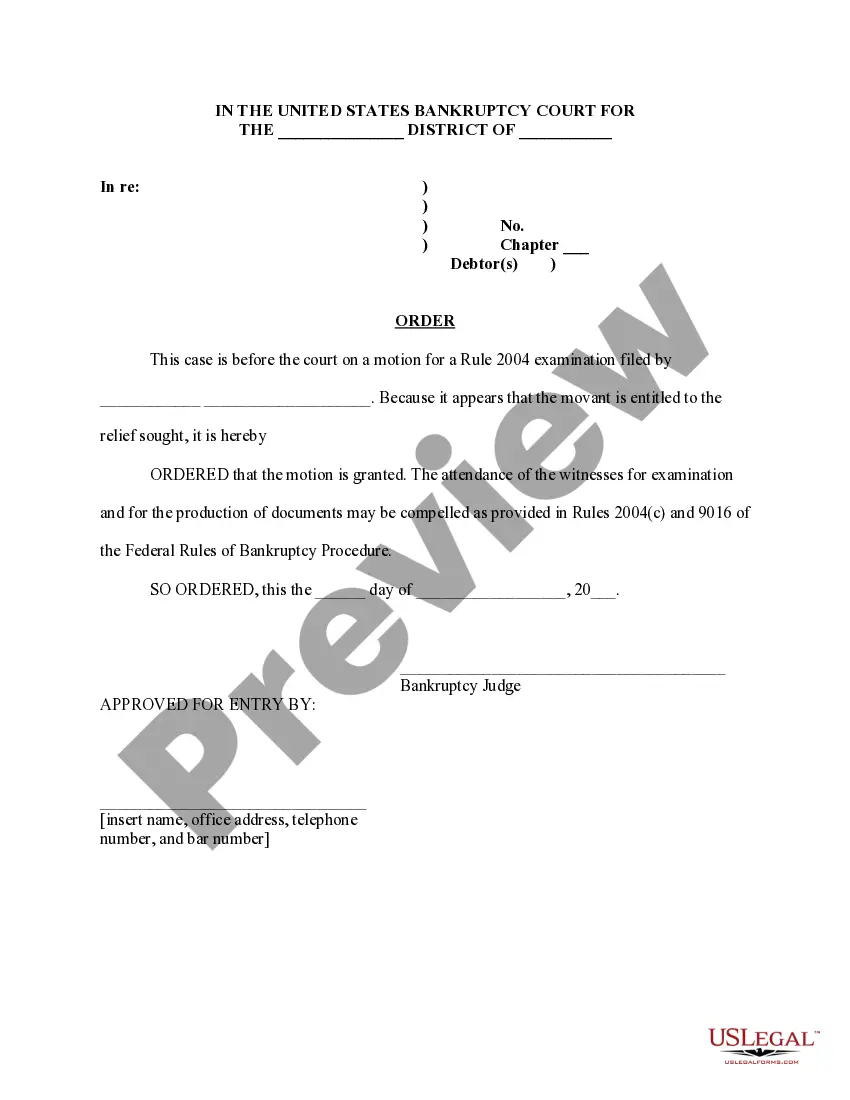

Order authorizing Rule 2004 examination - debtor

What is this form?

The Order Authorizing Rule 2004 Examination - Debtor is a legal document used in bankruptcy cases to permit the examination of a debtor by the requesting party. This form is specifically designed to confirm that the debtor will provide testimony or produce documents essential for understanding their financial situation. It differs from other legal forms as it addresses specific bankruptcy examination procedures under federal rules, enabling an authorized party to gather pertinent information regarding the debtor's assets and liabilities.

Key parts of this document

- The introduction specifying the jurisdiction and case details.

- The motion statement indicating who is requesting the examination.

- The order detailing the date, time, and location for the debtor's examination.

- The signature field for the bankruptcy judge to validate the order.

- Contact information for the attorney representing the movant.

When to use this form

This form is typically used when creditors or other interested parties need to investigate a debtor's financial position further. It may be employed in cases where there are questions about the accuracy of the debtor's listed assets or liabilities, or when additional evidence is required to support claims made in the bankruptcy proceedings.

Who this form is for

- Creditors seeking to verify claims against the debtor.

- Attorneys representing interested parties in bankruptcy cases.

- Trustees looking for more information regarding a debtor's financial circumstances.

Steps to complete this form

- Identify the parties involved and the specific bankruptcy case number.

- Fill in the name of the movant requesting the examination.

- Specify the date, time, and location for the debtorâs examination.

- Leave space for the bankruptcy judgeâs signature to finalize the order.

- Enter the attorneyâs contact information for reference.

Does this document require notarization?

This form does not typically require notarization unless specified by local law. It is recommended to check local regulations to ensure compliance with any specific requirements.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Mistakes to watch out for

- Neglecting to fill in the case number or relevant details accurately.

- Failing to provide all required dates and times for the examination.

- Omitting the attorney's contact information for processing the motion.

Advantages of online completion

- Convenient access to legal templates that can be downloaded and filled out at your pace.

- Editability of the form allows for adjustments tailored to specific cases.

- Reliable templates drafted by licensed attorneys to ensure legal compliance.

Looking for another form?

Form popularity

FAQ

As a result, most Chapter 13 plans do not have to provide for the repayment of unsecured debts. The only instance when Chapter 13 plans must provide for payment of unsecured debts is when an unsecured creditor objects to the plan. If this happens, the debtor must pass a ?disposable income? test.

If the Chapter 13 plan is dismissed, creditors may immediately initiate or continue with state court litigation pursuant to applicable state law to foreclose on the petitioner's property or garnish their income. If a bankruptcy case is dismissed, the legal affect is that the bankruptcy is deemed void.

A 100% plan is a Chapter 13 bankruptcy in which you develop a plan with your attorney and creditors to pay back your debt. It is required to pay back all secured debt and 100% of all unsecured debt.

Authority to Take a Rule 2004 Exam: FRBP 2004 provides parties with the opportunity to conduct an examination of a person and/or documents, even though an adversary proceeding has not been filed. This is called a "Rule 2004 Examination".

The amount of time you need to wait to apply for a conventional loan after a Chapter 13 bankruptcy depends on how a court chooses to handle your bankruptcy. If the court dismisses your bankruptcy, you must wait at least 4 years from your dismissal date before you can apply.

Your debts will not be discharged. Often creditors?especially unsecured creditors?don't bother to file claims with the bankruptcy court and their debts get discharged, but only if you complete the plan. When the case is dismissed, those creditors stay with you.

During a 2004 examination, the trustee or creditor can examine anyone that might have knowledge of the debtor's finances and request the debtor or a third party to produce documents for review.

The discharge releases the debtor from all debts provided for by the plan or disallowed (under section 502), with limited exceptions. Creditors provided for in full or in part under the chapter 13 plan may no longer initiate or continue any legal or other action against the debtor to collect the discharged obligations.