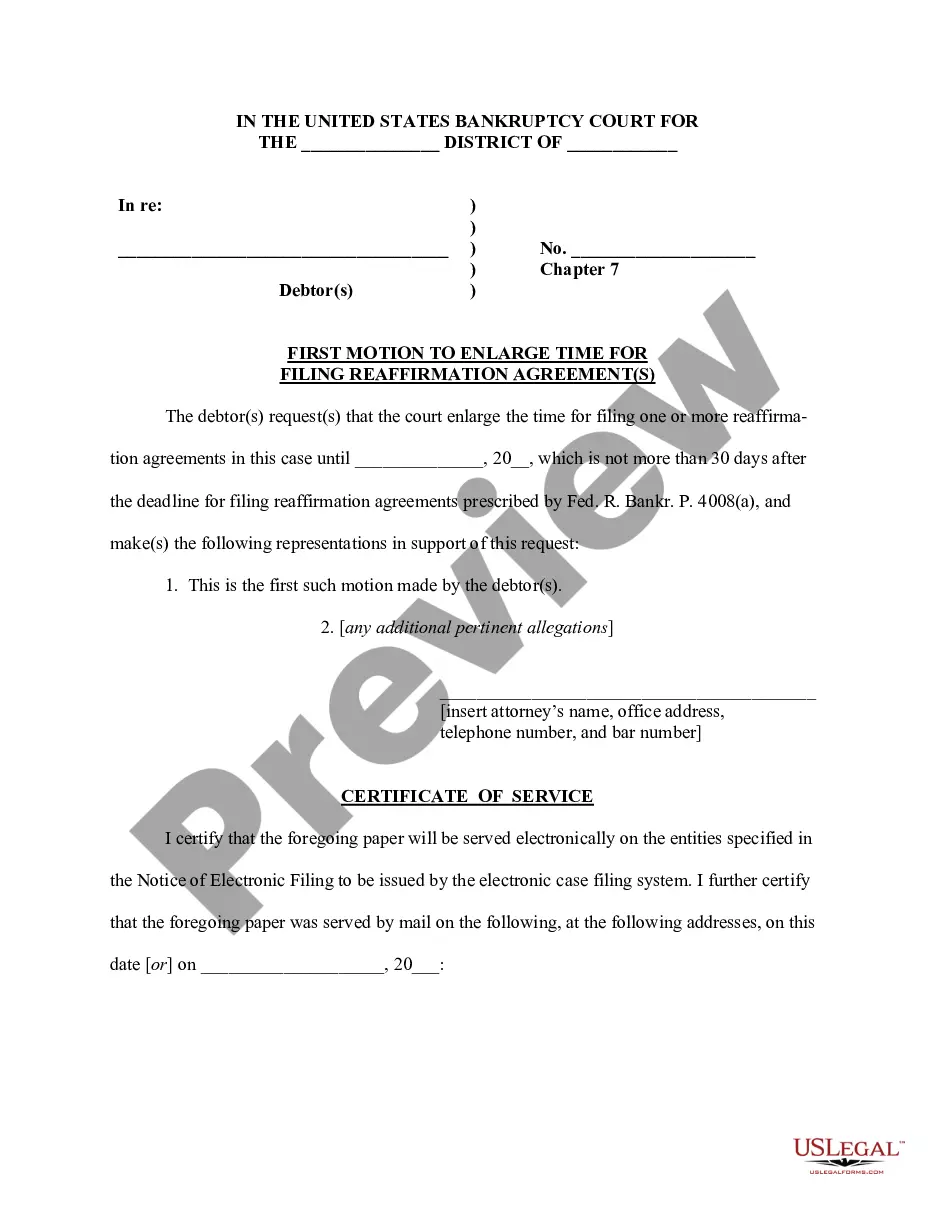

Order granting motion to enlarge time for filing reaffirmation agreements

What this document covers

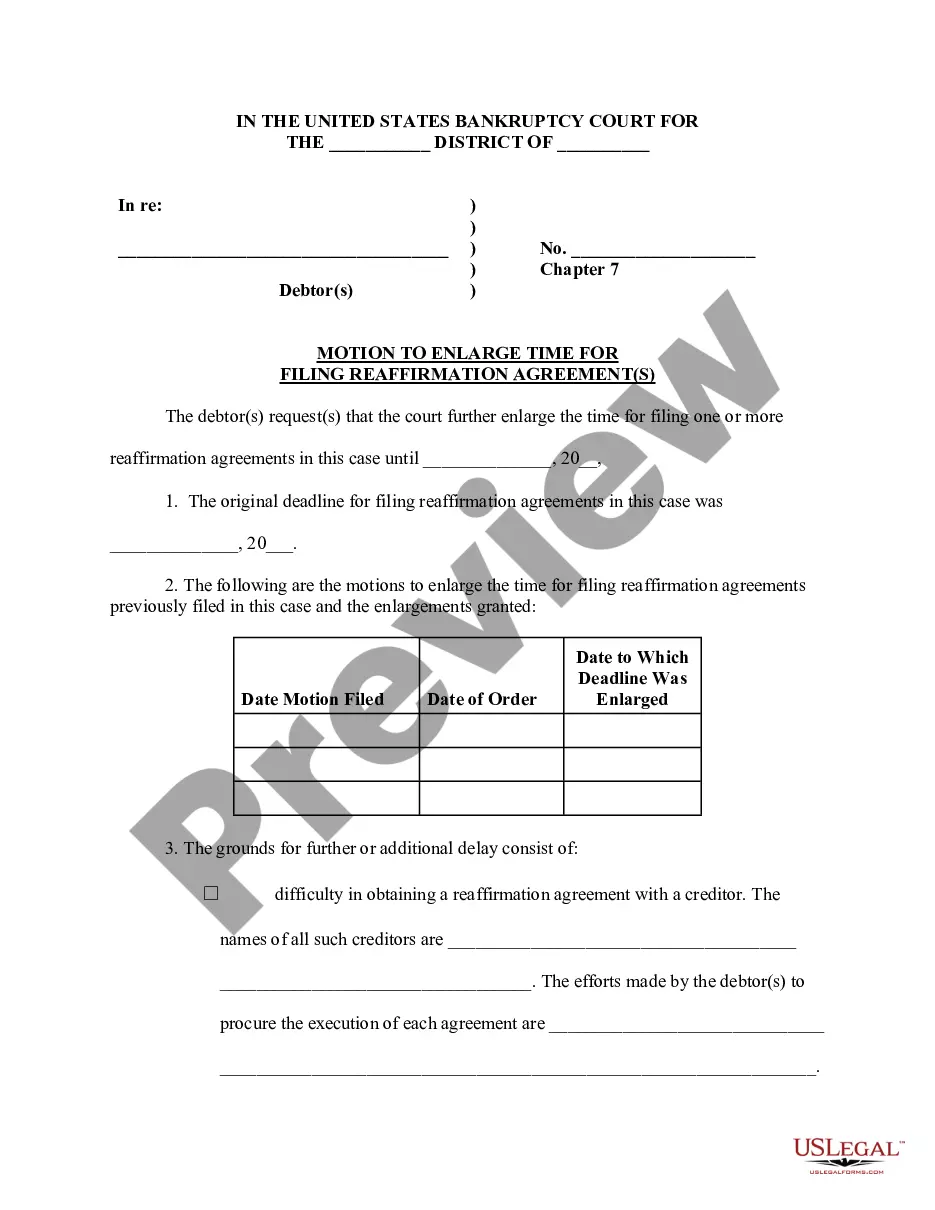

The Order granting motion to enlarge time for filing reaffirmation agreements is a legal document used in bankruptcy proceedings. This form allows debtors to request additional time to file reaffirmation agreements, which can help them retain certain secured debts, such as car loans or mortgage debts, despite being in bankruptcy. This form differs from other bankruptcy motions as it specifically addresses the timeline for reaffirmation agreements rather than their content or approval status.

What’s included in this form

- Case details: Includes the district and case number.

- Order granting motion: Confirms the court's decision to allow extra time for filing.

- New deadline: Specifies the new date by which reaffirmation agreements must be submitted.

- Discharge order delay: Indicates that the discharge order entry is postponed in relation to the new deadline.

- Judgeâs signature: Confirms judicial approval of the motion.

- Attorney approval: Includes details around the attorney who endorsed the motion.

Common use cases

This form is needed when a debtor in a Chapter 7 bankruptcy case realizes they cannot submit their reaffirmation agreements by the original deadline. It may be used when circumstances arise that require additional time to negotiate terms with creditors or when unforeseen delays occur in gathering necessary documentation.

Who can use this document

- Debtors in Chapter 7 bankruptcy seeking to retain secured debts.

- Individuals or businesses that have been granted a bankruptcy discharge but need to file reaffirmation agreements.

- Attorneys representing debtors in need of filing this motion.

Instructions for completing this form

- Identify the debtor(s) involved in the case and fill in the case details at the top of the form.

- Clearly state the reason or cause for requesting an extension on the filing deadline for reaffirmation agreements.

- Specify the new deadline for filing these agreements in the designated section.

- Ensure that it reflects the correct date by which the reaffirmation agreements must be submitted.

- Have the presiding bankruptcy judge sign the order to finalize the motion.

- Obtain the necessary approval and input from the representing attorney before submission.

Is notarization required?

This form does not typically require notarization unless specified by local law. It is essential to confirm with local bankruptcy court rules to determine if notarization is necessary for your particular submission.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Mistakes to watch out for

- Failing to provide a valid reason for the extension.

- Not including all necessary case details such as the case number and district.

- Leaving the new deadline field blank or incorrectly dating it.

- Neglecting to secure the judge's signature before filing.

Benefits of using this form online

- Convenience: Download the form instantly from anywhere without needing a physical trip to the courthouse.

- Editability: Fill out the form digitally, making it easier to correct mistakes than handwritten forms.

- Reliability: Access securely drafted forms that comply with current legal standards and are suitable for submission.

Key takeaways

- The Order granting motion to enlarge time for filing reaffirmation agreements is crucial for debtors needing more time to keep secured debts.

- Proper completion of the form ensures compliance with bankruptcy procedures and avoids delays in the bankruptcy process.

- Taking advantage of online resources for legal forms can streamline the completion process.

Looking for another form?

Form popularity

FAQ

To reaffirm a car loan, you must be able to show the court that the vehicle is necessary and that the payment is reasonable. You must also demonstrate that the car payment isn't an undue hardship on your household and that you'd be able to afford the necessities of life.

A reaffirmation agreement is a new contract with the lender that says you'll be responsible for the debt on your car and the lien will stay in place, even though your other debts are being discharged in bankruptcy. Most lenders will require a reaffirmation agreement if you want to keep your car.

If you reaffirm a debt and then fail to pay it, you owe the debt the same as though there was no bankruptcy. The debt will not be discharged, and the creditor can take action to recover any property on which it has a lien or mortgage. The creditor can also take legal action to recover a judgment against you.

You will likely have to default on the loan before the lender takes such an action, but if you don't reaffirm, you'll live in a legal gray area. Your lender can take your home even if you make all your payments, as you are no longer obligated under the terms of the promissory note.

An executed reaffirmation agree- ment may be filed by any party, including the debtor or a creditor. It must be filed within 60 days after the first date set for the first meeting of creditors in the bankruptcy case unless the deadline is extended by the bankruptcy court.

If you don't sign a reaffirmation agreement, the lender can repossess your car after your case closes and the automatic stay lifts. Some car lenders are known to repossess the car immediately, even if you are current on payments.

Reaffirming a debt informs the lender that you intend to continue to pay the loan. Generally, the lender will continue to report the loan and all payments made on that loan to the credit reporting agencies, which may help improve your credit score after bankruptcy, provided timely payments are made on the loan.

A reaffirmed debt remains your personal legal obligation to pay. Your reaffirmed debt is not discharged in your bankruptcy case. That means that if you default on your reaffirmed debt after your bankruptcy case is over, your creditor may be able to take your property or your wages.