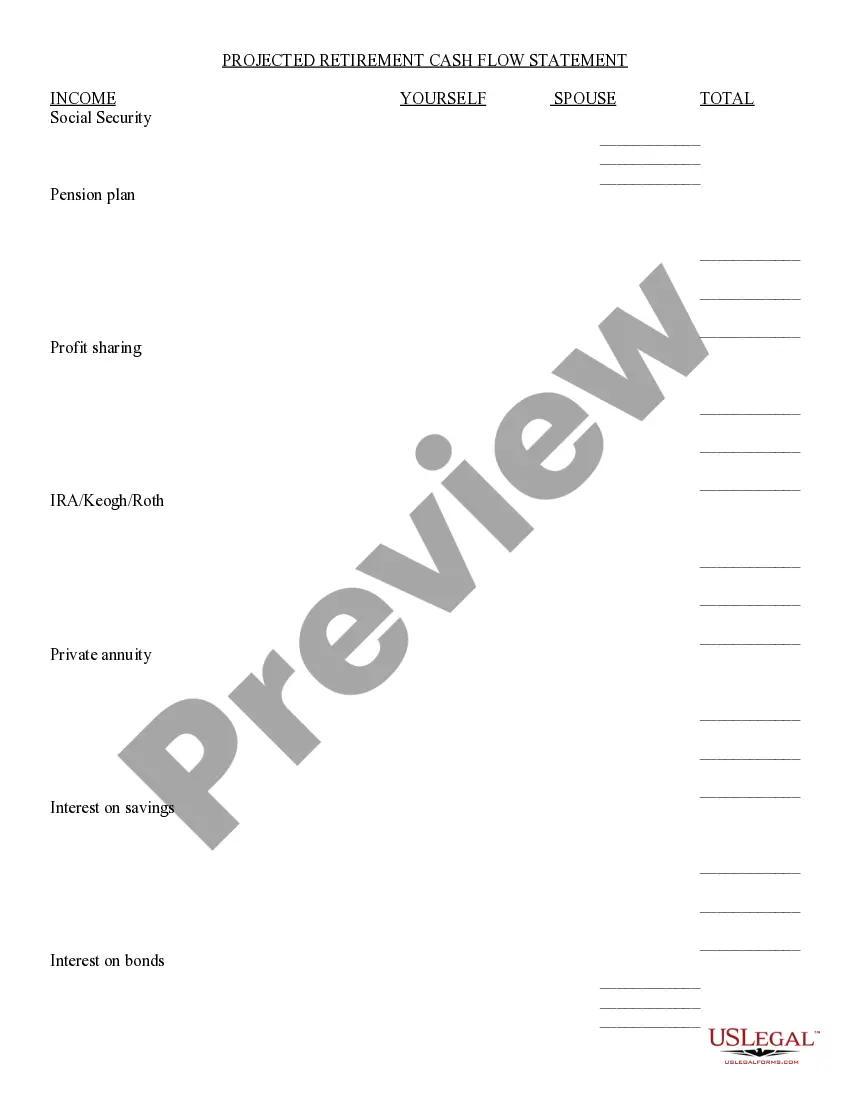

Monthly Retirement Planning

About this form

The Monthly Retirement Planning form is a practical tool designed to help individuals calculate how much they need to save each month to retire comfortably. This form caters specifically to those looking to ensure they meet their retirement savings goals with an understanding of interest rates and inflation. By using this planning sheet, individuals can determine the amount required to build a nest egg for a secure retirement, distinguishing it from general budgeting or savings forms.

Form components explained

- Annual income desired at retirement: Allows users to specify how much they wish to live on during retirement.

- Nest egg calculation: Provides a formula for determining the total amount needed based on the desired annual income.

- Monthly savings factor: Includes age-specific factors to outline how much users should save each month based on their current age and retirement timeline.

- Interest and inflation considerations: Clarifies how interest rates and inflation affect retirement savings and income.

Common use cases

This form is beneficial for anyone planning for retirement, especially if you are in your 20s to 60s. Use it when you want to assess your monthly savings needs based on your desired retirement income. Itâs particularly useful if you are starting your savings journey or if you want to adjust your current savings strategy to better meet your retirement goals.

Who this form is for

- Individuals aged 25 to 60 looking to plan for retirement.

- Those estimating their retirement needs based on current income and lifestyle expectations.

- People wanting to ensure their savings account for future inflation and investment growth.

Steps to complete this form

- Determine your desired annual income at retirement and enter it in the designated field.

- Calculate your required nest egg by dividing your desired income by 0.08.

- Select your age to find the appropriate savings factor for your timeline.

- Multiply the nest egg needed by your age-specific savings factor to find your monthly savings requirement.

- Consider running the calculation with adjusted ages to gauge the impact of starting your savings earlier or later.

Notarization requirements for this form

This form does not typically require notarization unless specified by local law.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Avoid these common issues

- Failing to account for inflation when determining nest egg requirements.

- Not updating the form as personal financial situations or goals change.

- Overestimating anticipated investment returns without proper research.

Benefits of completing this form online

- Convenient access to a structured savings calculator at any time.

- Editability allows for adjustments as financial goals evolve.

- Reliability in calculations, stemming from attorney-drafted templates.

Legal use & context

- This form serves as a guideline rather than a legally binding document.

- Users should consult financial advisors for personalized retirement planning advice.

- Calculations provided in this form are estimates and should be reviewed periodically.

Quick recap

- The Monthly Retirement Planning form helps you quantify your monthly savings needs for retirement.

- Understanding the impact of inflation and compound interest is crucial for effective retirement planning.

- Regularly reassessing your retirement plans can help you stay on track towards your goals.

Looking for another form?

Form popularity

FAQ

A 401(k), pensions are often seen as the clear winner. However, the smart use of a 401(k) plan can provide benefits that make for a comfortable retirement. To make the most of your company-sponsored retirement plan, start saving early, maximize your employer's match and watch your balance grow.

401(k) plans. A 401(k) plan is a tax-advantaged plan that offers a way to save for retirement. 403(b) plans. 457(b) plans. Traditional IRA. Roth IRA. Spousal IRA. Rollover IRA. SEP IRA.

Until recently, the commonly accepted rule of thumb said to withdraw 4% each year. However, now experts are stating that 3% might be better.

Determine your expenses. Your expenses, and not your income, will determine how much you need to save for your retirement. Eliminate all kinds of debt. Save money through an RRSP. Retirement housing planning.

401(k) plans. A 401(k) plan is a tax-advantaged plan that offers a way to save for retirement. 403(b) plans. 457(b) plans. Traditional IRA. Roth IRA. Spousal IRA. Rollover IRA. SEP IRA.

Research shows that high stock valuations should lead to lower initial withdrawal rates.Even at extremely high stock valuations, research by financial planner Michael Kitces shows that the 4% rule still holds.

People who are considering early retirement may have to reduce their annual withdrawal to 3% to make the money last. In a situation where there are low returns and high inflation, following the 4% rule means higher withdrawals. This could deplete the retirement savings faster.

The Four Percent Rule states that you can withdraw 4% of your portfolio each year in retirement for a comfortable life. It was created using historical data on stock and bond returns over a 50-year period.

To figure out how much income you'll need in retirement, take your estimated monthly expenses (be sure it's realistic) and divide by 4%. So, for example, if you estimate you'll need $50,000 a year to live comfortably, you'll need $1.25 million ($50,000 ÷ 0.04) going into retirement.