Certificate of Trust Indebtedness

Understanding this form

A Certificate of Trust Indebtedness is a legal document that certifies a trust's indebtedness without revealing the specifics about the trust's assets or beneficiaries. This condensed form serves as proof of a valid trust, allowing you to engage with financial institutions while maintaining your privacy. It is sometimes referred to as a certificate or abstract of trust in certain states.

What’s included in this form

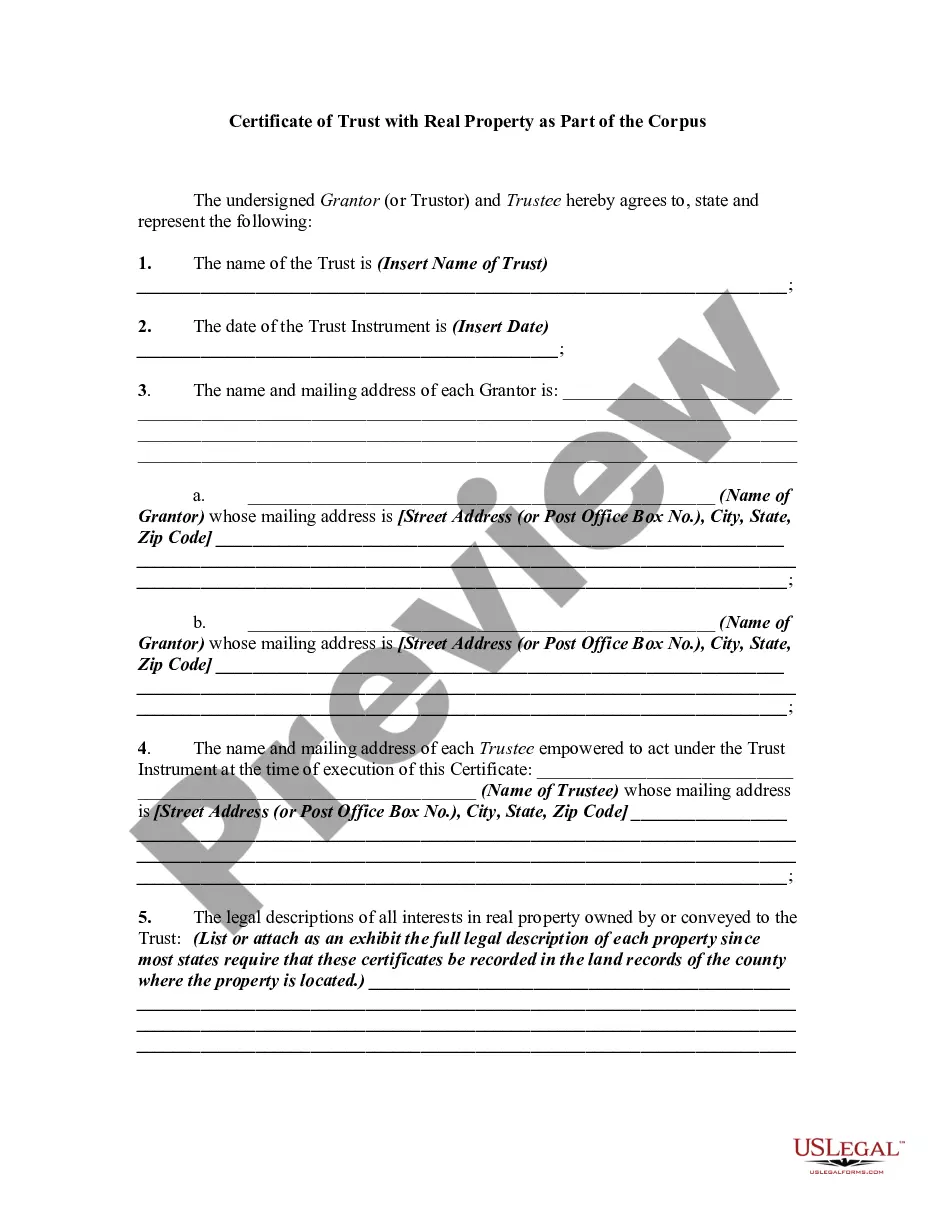

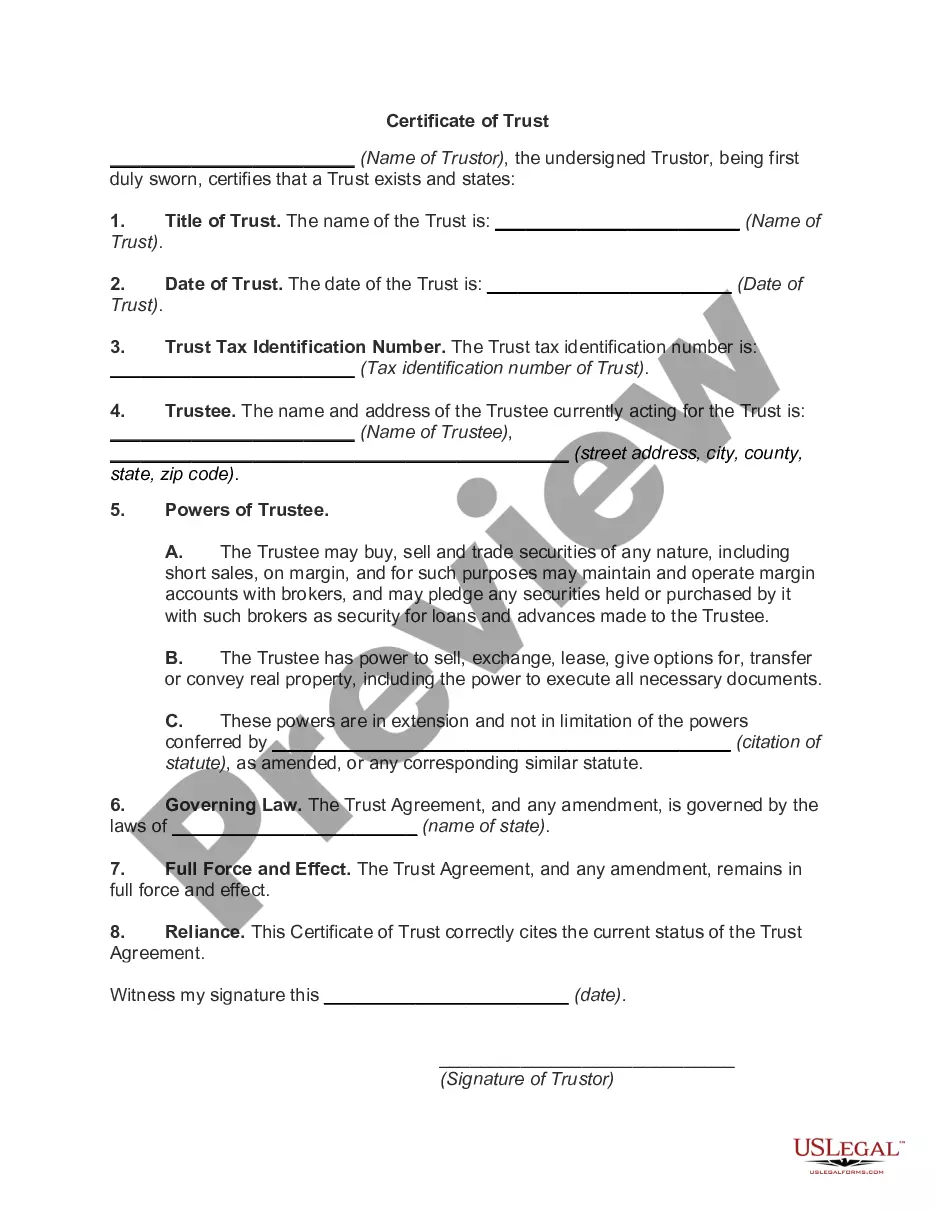

- Names of the Trustor and Trustee, identifying who established the trust and who manages it.

- Date on which the trust agreement was established.

- Name of the Payee, the person or entity to whom the trust is indebted.

- Amount owed, outlining how much is to be paid from the trust's principal upon termination.

- Interest rate applicable to the indebtedness.

- Payment schedule, indicating whether payments will be made monthly or quarterly.

- Signature of the Trustee, providing approval and acknowledgment of the terms outlined.

Situations where this form applies

This form is useful in scenarios where a trust is established with financial obligations without revealing detailed information about the trust's assets or beneficiaries. You might need it when approaching a bank for a loan, seeking investment opportunities, or when settling debts that involve the trust. It provides a concise certification of the trust's validity while keeping private elements secure.

Who should use this form

- Individuals who are trustees of a trust and need to confirm trust obligations.

- Trustors looking to facilitate transactions without disclosing sensitive trust details.

- Financial institutions and creditors requiring assurance of trust validity.

How to complete this form

- Identify the parties involved by entering the names of the Trustor and Trustee.

- Fill in the date when the trust was established.

- Specify the name of the Payee and the amount of the indebtedness.

- Indicate the interest rate and the payment schedule (monthly or quarterly).

- Have the Trustee date and sign the certificate to validate it.

Does this form need to be notarized?

This form usually doesn’t need to be notarized. However, local laws or specific transactions may require it. Our online notarization service, powered by Notarize, lets you complete it remotely through a secure video session, available 24/7.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Avoid these common issues

- Failing to include the name of the Payee, which can render the document invalid.

- Not signing the document where required, leading to issues with enforceability.

- Leaving out the interest rate, which is crucial for clarity on repayment terms.

Advantages of online completion

- Convenience of accessing the form from any location and at any time.

- Editable content allows for quick adjustments to meet personal circumstances.

- Provides reliable templates created by licensed attorneys for legal accuracy.

Looking for another form?

Form popularity

FAQ

Washington Deed of Trust and Promissory Note Information A deed of trust (DOT), is a document that conveys title to real property to a trustee as security for a loan until the grantor (borrower) repays the lender ing to terms defined in an attached promissory note.

A deed of trust is a legal agreement used in real estate transactions that establishes a piece of property as collateral for a loan, much like a traditional mortgage. The deed of trust is signed by the borrowing party and recorded with the register of deeds where the property is located.

A deed of trust ? the form used almost exclusively in Virginia and in many other states in place of a true mortgage ? is similar to a mortgage in that both create a lien on the property to secure repayment of a loan. This lien gives the lender the right to sell the real property in the event the loan is not repaid.

Promissory notes and deeds of trust are subject to Washington's six-year statute of limitations.

If your circumstances change any you are no longer able to make your payments, your Trust Deed may fail and you will still be liable for your debts or even forced into bankruptcy.

A deed of trust has a borrower, lender and a ?trustee.? The trustee is a neutral third party that holds the title to a property until the loan is completely paid off by the borrower. In most cases, the trustee is an escrow If you don't repay your loan, the escrow company's attorney must begin the foreclosure process.

A deed of trust is an agreement between a home buyer and a lender at the closing of a property. The agreement states that the home buyer will repay the home loan and the mortgage lender will hold the property's legal title until the loan is paid in full.

Deeds of trust are the most common instrument used in the financing of real estate purchases in Alaska, Arizona, California, Colorado, the District of Columbia, Idaho, Maryland, Mississippi, Missouri, Montana, Nebraska, Nevada, North Carolina, Oregon, Tennessee, Texas, Utah, Virginia, Washington, and West Virginia,