Owner Financing Contract for Home

Understanding this form

The Owner Financing Contract for Home is a legal agreement between a buyer and a seller that outlines the terms under which the seller acts as the lender for the home purchase. This form establishes a security agreement, ensuring that the buyer's obligation to pay is backed by an interest in the property being sold. It differs from traditional bank financing by facilitating a direct buyer-seller relationship, which can be beneficial when both parties seek flexible terms.

Form components explained

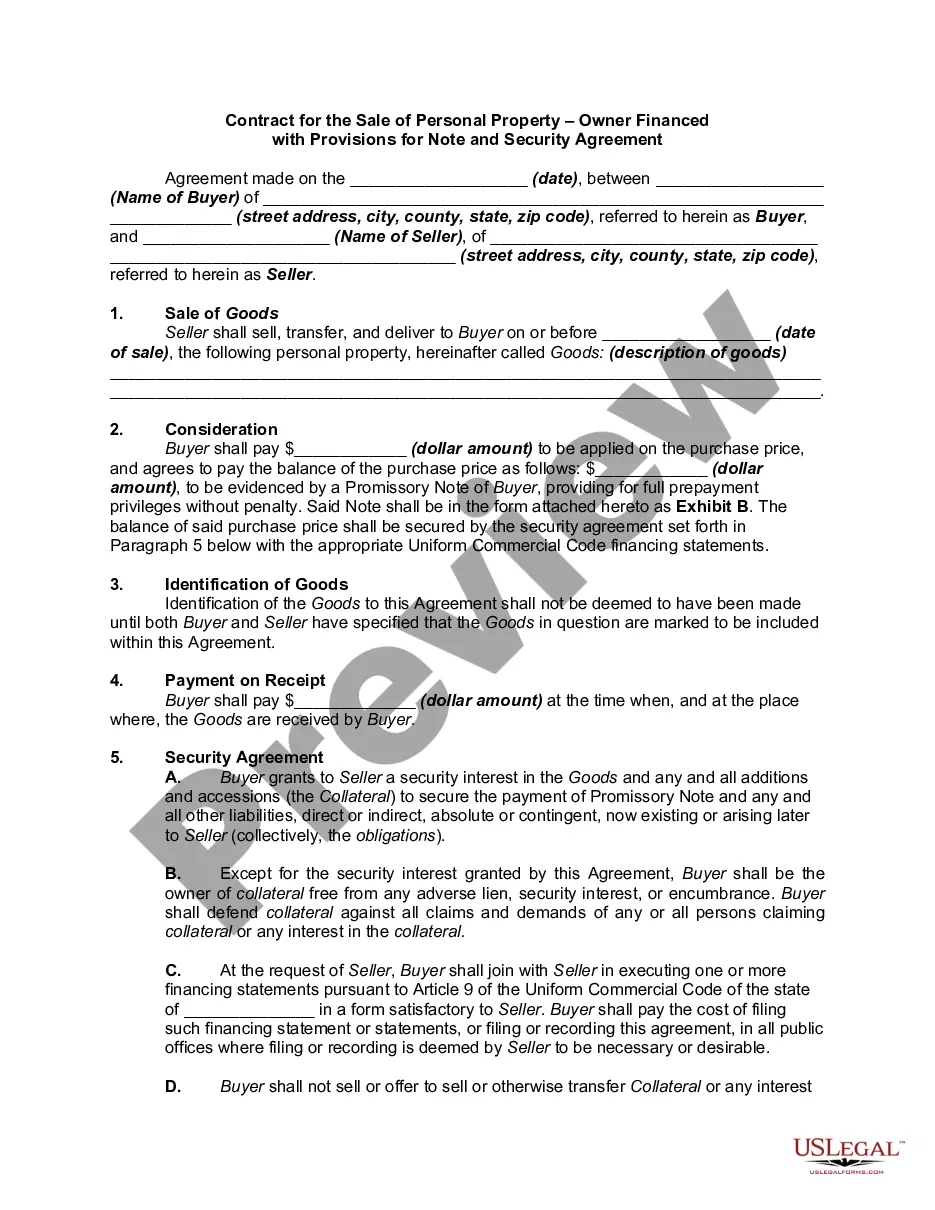

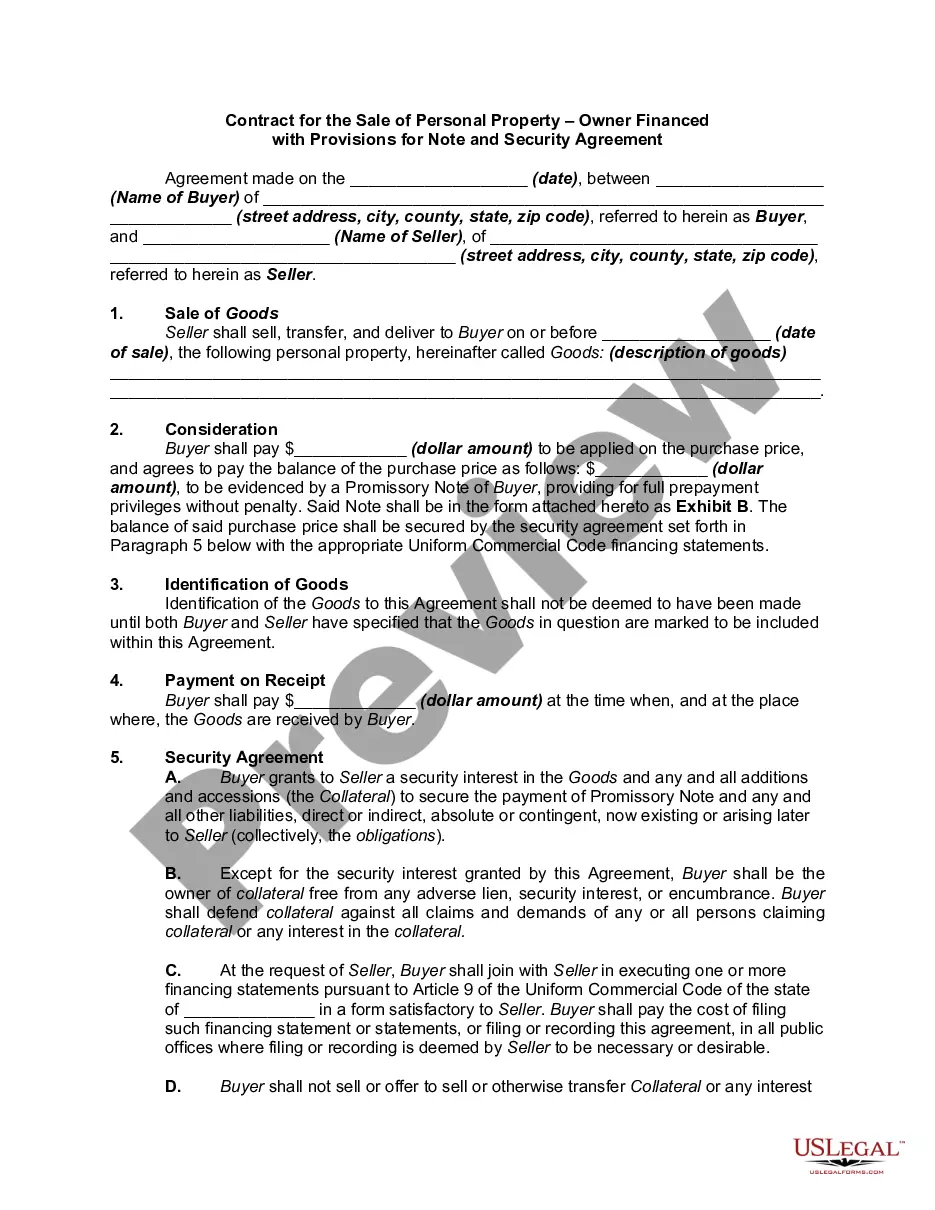

- Identification of parties: Includes names and addresses of the buyer and seller.

- Sale of goods: Details the property being sold and the purchase price.

- Payment terms: Outlines how the buyer will pay the seller, including down payment and monthly payments.

- Security agreement: Specifies the security interest granted to the seller and the buyer's responsibilities.

- Warranties: Includes warranties of no encumbrances on the property and clear title.

- Default clauses: Defines what constitutes a default and the seller's remedies.

When this form is needed

This form is essential in situations where a buyer wishes to purchase a home but prefers to finance through the seller instead of a bank. It is particularly useful when traditional financing options are limited or when the buyer and seller have agreed on customized terms that benefit both parties. This agreement is also advantageous in a competitive real estate market where quick financing arrangements might be necessary.

Who should use this form

- Home buyers seeking flexible financing arrangements directly with a seller.

- Home sellers looking to provide owner financing as an alternative to traditional mortgages.

- Individuals who want to outline clear payment and security terms in a home sale.

- People involved in a real estate transaction who want a legally binding agreement outlining their obligations.

Instructions for completing this form

- Identify the parties: Fill in the names and addresses of both the buyer and seller.

- Specify property details: Provide a detailed description of the property being sold.

- Outline payment terms: Indicate the total purchase price and payment schedule, including any down payment.

- Include security details: Outline the security interest in the property and any conditions tied to it.

- Sign and date: Ensure both parties sign and date the contract, confirming their agreement to the terms.

Does this document require notarization?

This form does not typically require notarization unless specified by local law. However, it is advisable to check with local regulations to ensure compliance.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Common mistakes to avoid

- Failing to clearly define the property being sold may lead to disputes.

- Not specifying payment terms can create confusion regarding obligations.

- Omitting security interests, which is crucial for protecting the seller's investment.

- Not having both parties sign and date the agreement can lead to enforceability issues.

Benefits of completing this form online

- Convenient access to legal documents from anywhere at any time.

- Editable templates allow users to customize terms specific to their situation.

- Secure storage ensures your information is protected and accessible.

- Drafted by licensed attorneys, providing peace of mind regarding legality.

Looking for another form?

Form popularity

FAQ

In seller financing, the seller takes on the role of the lender. Instead of giving cash to the buyer, the seller extends enough credit to the buyer for the purchase price of the home, minus any down payment. The buyer and seller sign a promissory note (which contains the terms of the loan).

Step 1: Obtain the current principal balance and interest rate from the land contract or promissory note. Step 2: Times the balance by the interest rate. Step 3: Divide by 12. Step 1: A seller-financed note has a balance of 100,000 at 8% interest. Step 2: $100,000 x 8% (or .08) = $8,000 (interest for the year)

A homeowner with a mortgage can offer seller-carried financing but it's sometimes difficult to actually do.Home sellers, looking to increase their buyer pools, might choose to offer seller-carried financing, even if they still have mortgages on their homes.

There is no legal requirement that a lender charge interest. However, the failure to charge interest on an owner-financed sale or real property may bring into question for tax purposes whether the transfer was a legitimate sale or a gift.

Interest rateInterest rates for seller-financed loans are typically higher than what traditional lenders would offer. The seller takes on some risk by holding financing, and he or she may charge a higher interest rate to offset this risk. It's not uncommon to see interest rates from 4% to 10%.

Potential buyers can be turned down if they are a credit risk. Most owner-financing deals are short term. A typical arrangement is to amortize the loan over 30 years (which keeps the monthly payments low), with a final balloon payment due after only five or ten years.

Advantages of buying an owner-financed home In a seller-financed transaction there are no closing costs such as loan origination fees, discount points and mortgage insurance premiums. Because you won't have to wait for bank approvals, closing can happen much quicker than with traditional financing.

Q: Are there closing costs when you sell for sale by owner? A: Yes! Home closing costs usually amount to two to four percent of the purchase price.