Owner Financing Contract for Moblie Home

Understanding this form

The Owner Financing Contract for Mobile Home is a legal document that facilitates the sale of a mobile home directly from the seller to the buyer, where the buyer makes payments over time rather than paying the full amount upfront. This form includes various provisions, such as a security agreement that protects the seller's interests by allowing them a claim on the mobile home until all payments are completed. Unlike traditional financing through a bank, this agreement empowers individuals to negotiate terms directly, which can be beneficial in many purchasing situations.

Form components explained

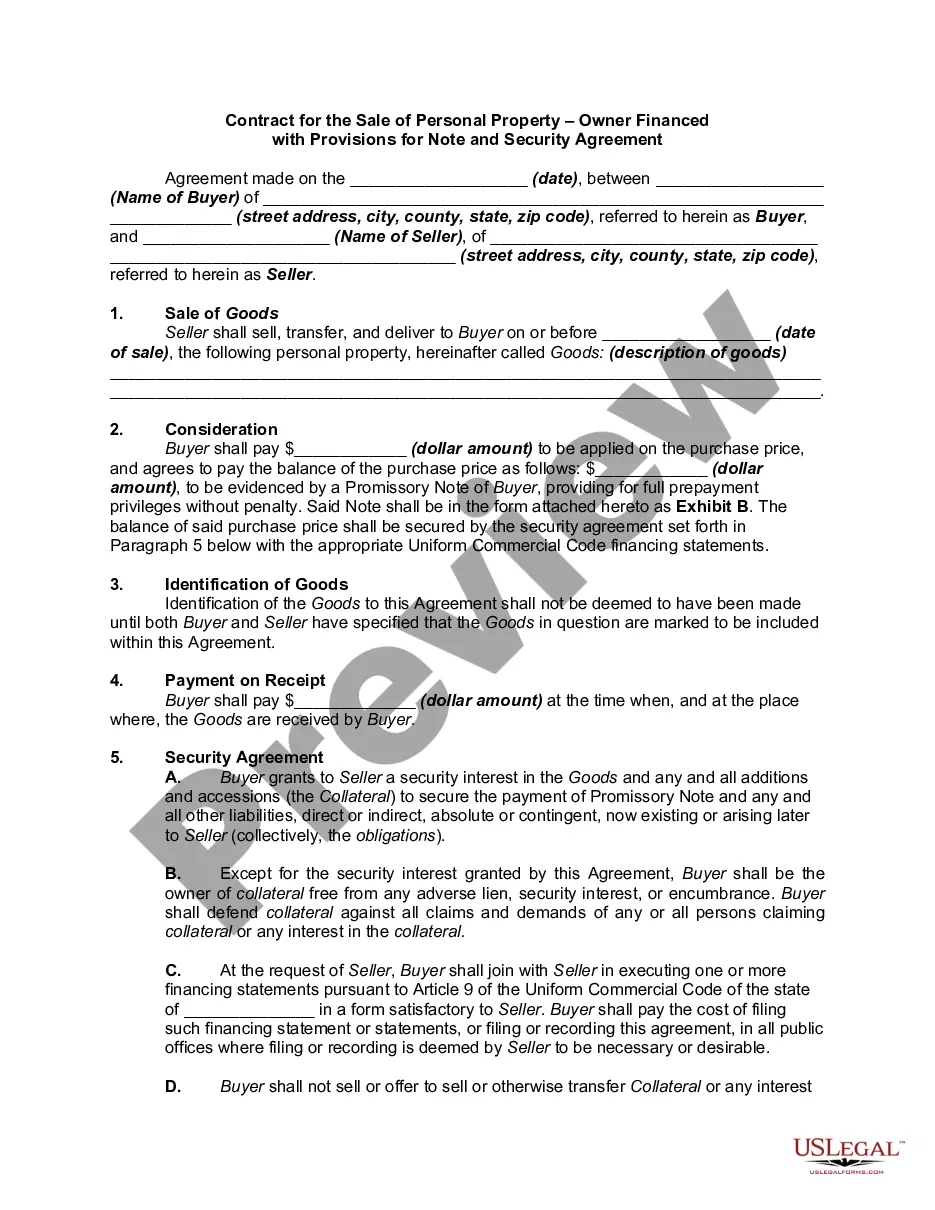

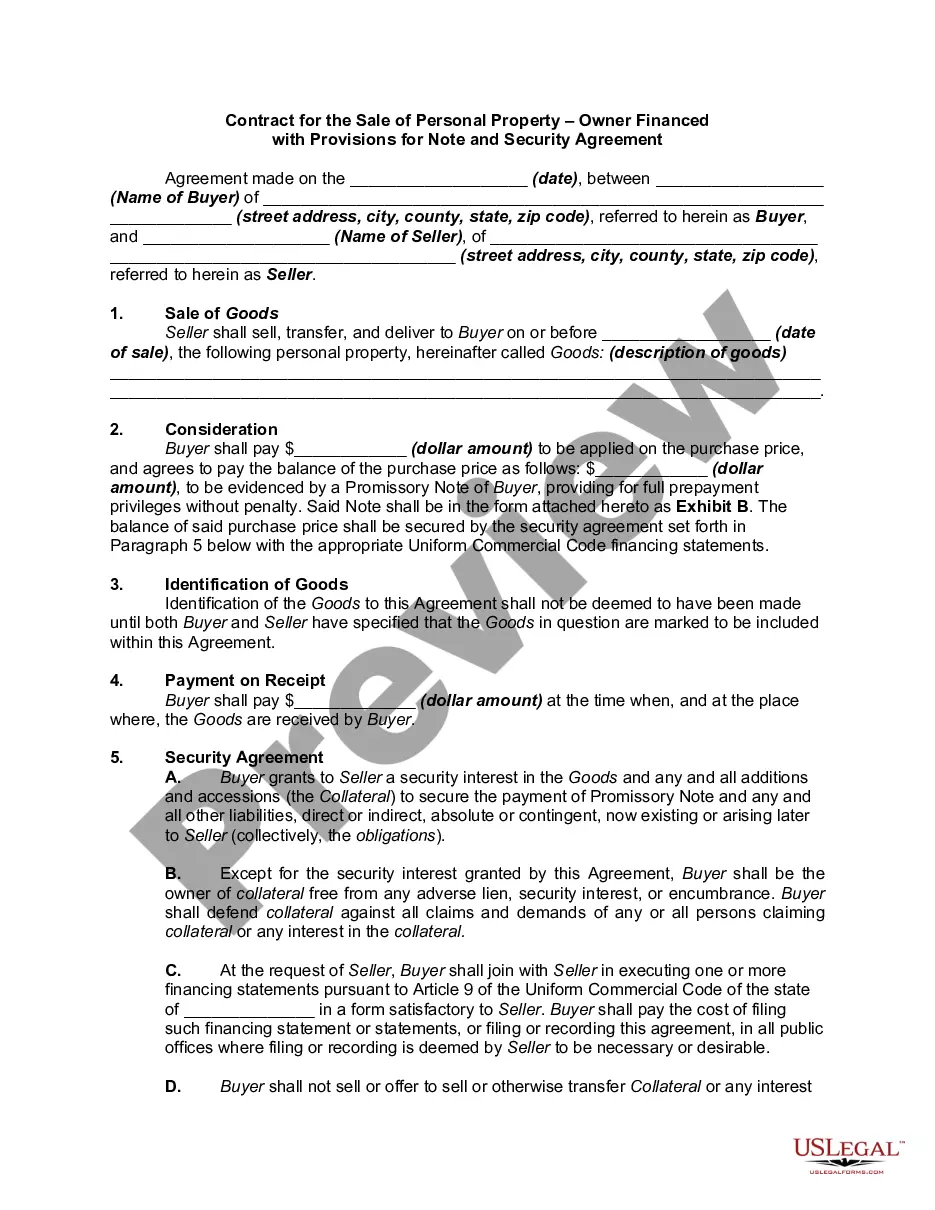

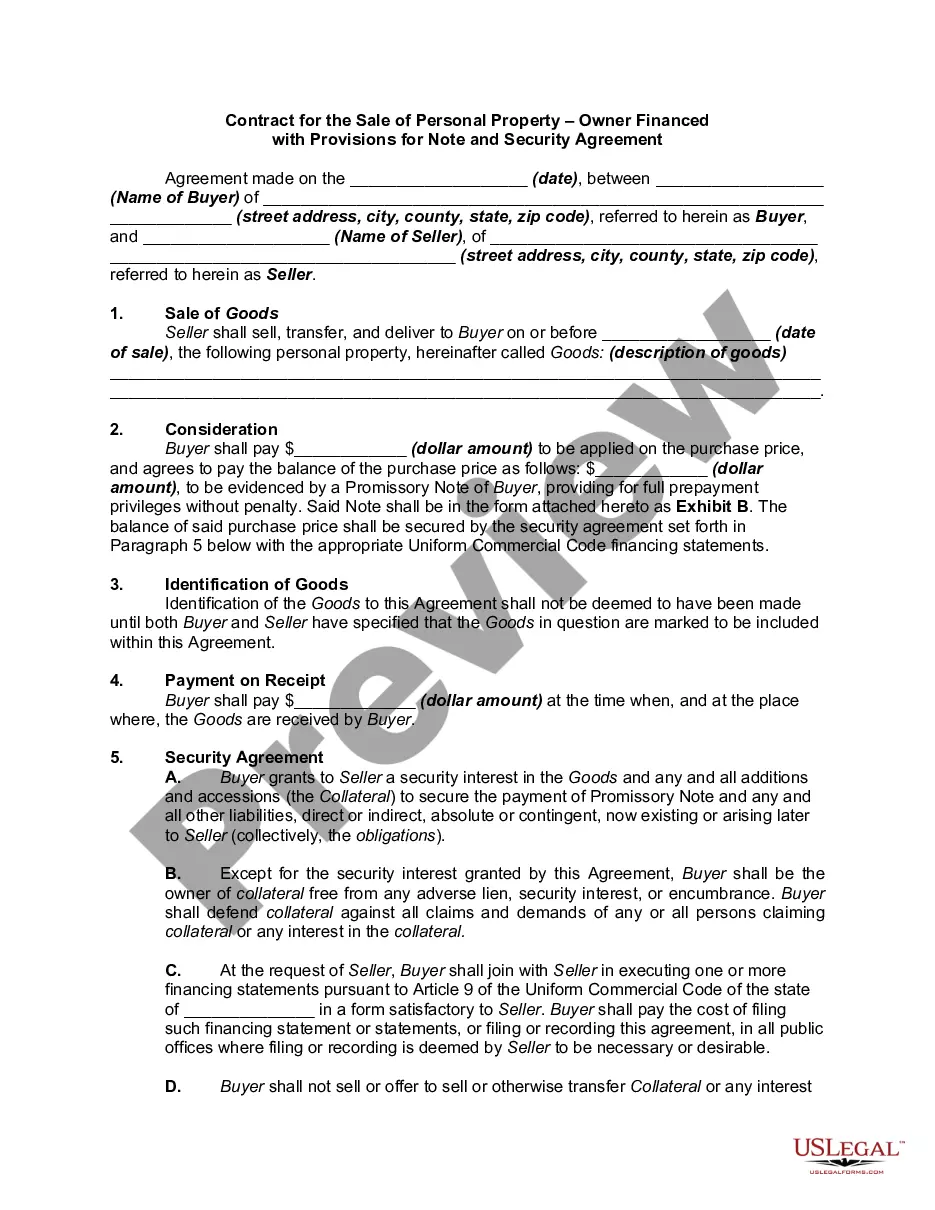

- Date of the agreement and identification of parties involved: buyer and seller.

- Description of the mobile home being sold, referred to as "Goods."

- Payment terms, including down payment and payment plan through a promissory note.

- Security agreement clauses outlining the seller's rights and buyer's obligations.

- Warranties regarding the title and condition of the mobile home.

- Conditions regarding default and remedies available to the seller.

Common use cases

This form is used when a seller wishes to sell a mobile home and provide financing directly to the buyer. It is ideal in situations where the buyer may not qualify for traditional financing or when the seller wants to facilitate a smooth transaction with flexible payment options. This agreement is also beneficial in private sales, where formal loan processes can be cumbersome or time-consuming.

Who should use this form

- Individuals selling a mobile home who prefer to offer financing to the buyer.

- Buyers looking to purchase a mobile home through owner financing.

- Parties in a private sale where traditional financing options are unavailable or undesirable.

How to complete this form

- Identify the parties: Enter the names and addresses of the buyer and seller.

- Specify the mobile home: Provide a detailed description of the property being sold.

- Enter payment details: Include the down payment amount and the payment plan for the remaining balance.

- Review security agreement clauses: Ensure both parties understand their rights and obligations.

- Sign and date the agreement: Both parties must sign and date to finalize the contract.

Notarization requirements for this form

This form does not typically require notarization unless specified by local law. However, verifying your stateâs requirements and seeking legal advice may be beneficial to ensure compliance.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Common mistakes to avoid

- Failing to accurately describe the mobile home, leading to disputes about the property.

- Not specifying payment terms clearly, which can result in confusion later on.

- Neglecting to include or understand the provisions of the security agreement, which can affect the seller's rights.

- Omitting signatures or dates, rendering the contract unenforceable.

Why complete this form online

- Convenience of downloading and printing the form at any time.

- Editability allows customization to fit specific buyer and seller needs.

- Drafted by licensed attorneys, ensuring reliability and adherence to legal standards.

Looking for another form?

Form popularity

FAQ

Owner financing can be a good option for buyers who don't qualify for a traditional mortgage. For sellers, owner financing provides a faster way to close because buyers can skip the lengthy mortgage process.

To qualify for low mobile home interest rates, make sure your credit score is at least 700. You'll need a score of 750 or higher to qualify for the best rates available.

Best Overall: Manufactured Nationwide. Best for Good Credit: ManufacturedHome.Loan. Best for Bad Credit: 21st Mortgage Corporation. Best for Low Down Payment: eLend. Best for Manufacturer's Financing: Vanderbilt Mortgage and Finance.

Mobile homes are far cheaper than traditional homes, so you may be able to finance your purchase through a personal loan. Personal loans are flexible loans you can use for almost any purpose. However, personal loan interest rates tend to be higher than those of other types of loans, such as mortgages or auto loans.

Financing is challenging for any homeowner, and that's especially true when it comes to mobile homes and some manufactured homes. These loans aren't as plentiful as standard home loans, but they are available from several sources and government-backed loan programs can make it easier to qualify and keep costs low.

Advantages of buying an owner-financed home In a seller-financed transaction there are no closing costs such as loan origination fees, discount points and mortgage insurance premiums. Because you won't have to wait for bank approvals, closing can happen much quicker than with traditional financing.

With owner financing (aka seller financing), the seller doesn't hand over any money to the buyer as a mortgage lender would. Instead, the seller extends enough credit to the buyer to cover the purchase price of the home, less any down payment. Then, the buyer makes regular payments until the amount is paid in full.

Why are Loans for Manufactured Homes so Difficult to Find?This is due to the fact that some manufactured homes may age more quickly than their site-built counterparts. It can also be because manufactured homes may not be as profitable as other types of home construction for certain lenders.

If your manufactured house is classified as real property, you may be able to finance it with a mortgage. Typically, it has to be built after 1976 (see explanation below). The loans work almost exactly the same as financing for traditional stick-built houses.