A limited partnership is a modified partnership. It has characteristics of both a corporation and a general partnership. In a limited partnership, certain members contribute capital, but do not have liability for the debts of the partnership beyond the amount of their investment. These members are known as limited partners. The partners who manage the business and who are personally liable for the debts of the business are the general partners. Limited partners have the right to share in the profits of the business and, if the partnership is dissolved, will be entitled to a percentage of the assets of the partnership. A limited partner may lose his limited liability status if he participates in the control of the business.

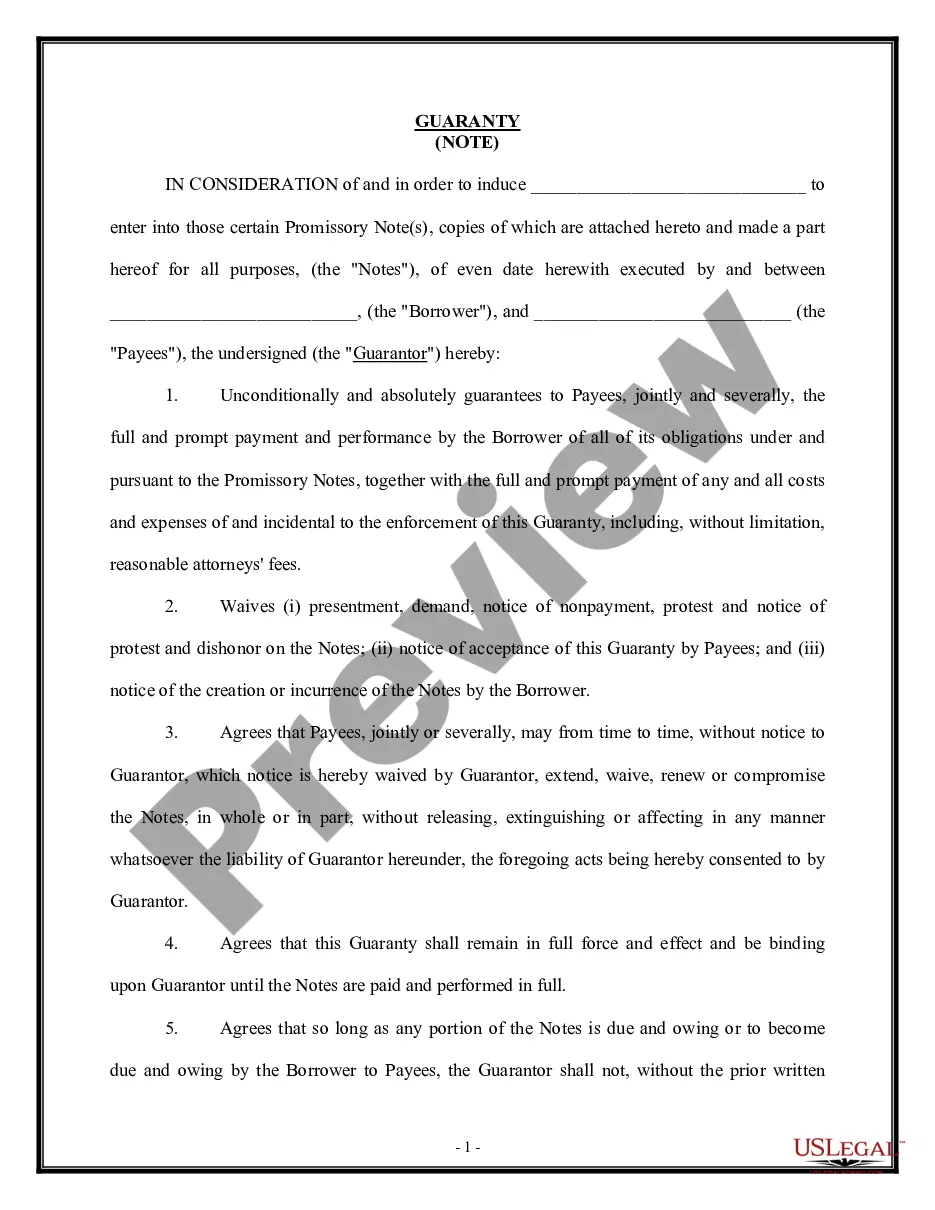

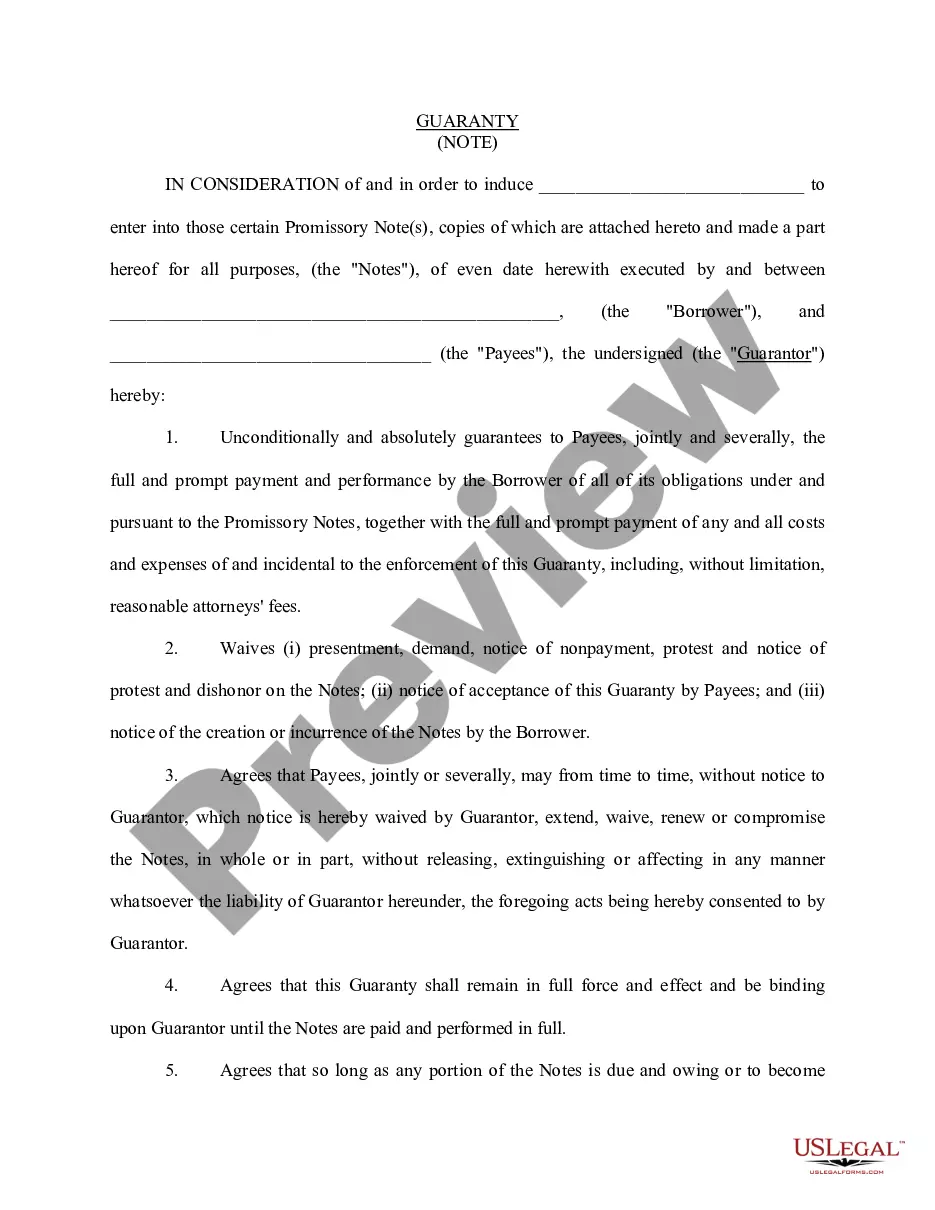

Guaranty of Payment by Limited Partners of Notes Made by General Partner on Behalf of Limited Partnership

Category:

State:

Multi-State

Control #:

US-01115BG

Format:

Word;

Rich Text

Instant download

Description

Free preview

How to fill out Guaranty Of Payment By Limited Partners Of Notes Made By General Partner On Behalf Of Limited Partnership?

Aren't you sick and tired of choosing from hundreds of templates each time you need to create a Guaranty of Payment by Limited Partners of Notes Made by General Partner on Behalf of Limited Partnership? US Legal Forms eliminates the lost time numerous American people spend browsing the internet for perfect tax and legal forms. Our skilled crew of lawyers is constantly updating the state-specific Samples collection, so it always provides the appropriate documents for your situation.

If you’re a US Legal Forms subscriber, simply log in to your account and click the Download button. After that, the form can be found in the My Forms tab.

Visitors who don't have a subscription should complete easy steps before being able to get access to their Guaranty of Payment by Limited Partners of Notes Made by General Partner on Behalf of Limited Partnership:

- Use the Preview function and look at the form description (if available) to make certain that it is the proper document for what you are looking for.

- Pay attention to the validity of the sample, meaning make sure it's the proper example for the state and situation.

- Utilize the Search field on top of the webpage if you want to look for another file.

- Click Buy Now and select a convenient pricing plan.

- Create an account and pay for the services using a credit card or a PayPal.

- Get your sample in a convenient format to complete, print, and sign the document.

After you have followed the step-by-step recommendations above, you'll always have the capacity to sign in and download whatever file you want for whatever state you want it in. With US Legal Forms, finishing Guaranty of Payment by Limited Partners of Notes Made by General Partner on Behalf of Limited Partnership samples or other legal files is not hard. Get started now, and don't forget to look at your examples with certified attorneys!

Form popularity

FAQ

In a general partnership: all partners (called general partners) are personally liable for all business debts, including court judgments. each individual partner can be sued for the full amount of any business debt (though that partner can in turn sue the other partners for their share of the debt), and.

The same person can be both a general partner and a limited partner, as long as there are at least two legal persons who are partners in the partnership. The general partner is responsible for the management of the affairs of the partnership, and he has unlimited personal liability for all debts and obligations.

Partners in an LLP are not personally liable when the business cannot pay its debts; instead, their liability is limited to the capital they have invested into the LLP. However due to their operational structure, limited liability partnerships are dealt with in a similar manner to companies when they become insolvent.

Limited partners cannot incur obligations on behalf of the partnership, participate in daily operations, or manage the operation.A creditor may sue for repayment of the partnership's debt from the general partner's personal assets.

A general partner is the partner who is personally liable within a limited partnership. They bear the direct and joint liability, with both the business and their own private assets, and usually act as managing director and representative of the company.

In a General Partnership, each Partner is liable for all debts and obligations of the Partnership. If one or more of the remaining Partners are unable to meet their obligations to the Partnership then the remaining Partner(s) are liable for the full debts of the Partnership.

If the withdrawal of a general partner violates a partnership agreement, in addition to any remedies otherwise available under applicable law, the limited partnership may recover from the withdrawing general partner damages for breach of the partnership agreement and offset the damages against the amount otherwise

A limited partnership is a relationship where one or more partners are not involved in the day-to-day management of the business.A general partner may invest money into the company. However, a general partner may also be personally liable for the debts of the company, while the limited partner is not.

A limited partnership (LP) exists when two or more partners go into business together, but the limited partners are only liable up to the amount of their investment.