Charitable Lead Inter Vivos Unitrust

About this form

The Charitable Lead Inter Vivos Unitrust is a legal document that establishes a trust allowing a donor to make charitable contributions while also providing for beneficiaries. In this type of trust, the donor transfers assets, which are then managed by a trustee. The trust pays a fixed percentage of the trust's net asset value to a specified charity for a specified term. After this term, the remaining assets are distributed to the donor's heirs. This form differs from standard charitable trusts by focusing on unitrust payments that are calculated annually based on the trust's value.

Key components of this form

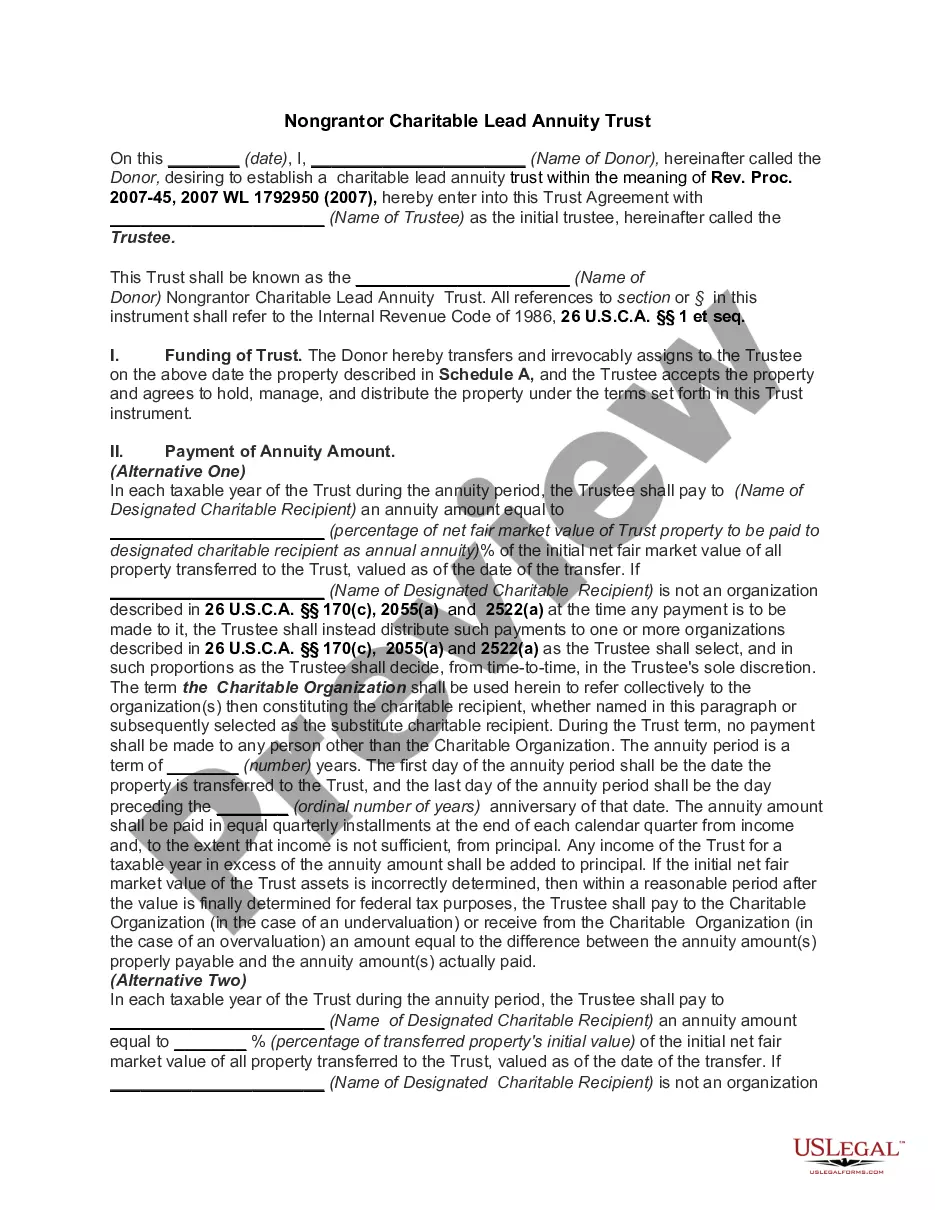

- Identification of parties: Grants the Grantor and Trustee's names and addresses.

- Transfer details: Specifies the property transferred to the trust.

- Charitable lead unitrust provisions: Details the percentage of assets paid to the charity each year.

- Distribution terms: Outlines how remaining assets are shared among the Grantor's heirs after the trust term.

- Trustee powers: Lists the powers and responsibilities of the Trustee in managing the trust.

When to use this document

This form is suitable when a donor wants to create a charitable lead trust that benefits a charity while also providing for their heirs after the trust term ends. It can be particularly useful for individuals wishing to reduce their taxable estate while actively supporting charitable organizations during their lifetime.

Who should use this form

- Individuals looking to benefit a charitable organization through a structured trust.

- Donors who wish to receive an income tax deduction for their charitable contributions.

- People with considerable assets who want to create a financial legacy for their heirs.

How to complete this form

- Identify the parties involved by entering the Grantor and Trustee's names and addresses.

- Transfer property by listing the assets in Schedule A.

- Specify the charity by naming the organization that will receive the annual payments.

- Determine the percentage of the unitrust amount to be paid to the charity each year.

- Enter the duration of the trust in years and details regarding the distribution of remaining assets.

Does this document require notarization?

This form does not typically require notarization unless specified by local law. However, it is advisable to consult with a legal professional to ensure compliance with your jurisdiction's requirements.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Common mistakes to avoid

- Incorrectly specifying the charity, limiting the intended charitable benefits.

- Failing to provide accurate asset valuations at the beginning of each tax year.

- Neglecting to have all required signatures from involved parties.

Advantages of online completion

- Convenient access to legally vetted templates.

- Editable fields that allow for customization based on individual requirements.

- Quick download and use, saving time compared to traditional legal processes.

By utilizing a Charitable Lead Inter Vivos Unitrust, donors can fulfill charitable intentions while also benefiting their heirs tax-efficiently. It is essential to adhere to federal and state regulations to maintain the trust's validity, particularly regarding tax deductions and compliance with IRS rules concerning charitable distributions.

Summary of main points

- A Charitable Lead Inter Vivos Unitrust provides a structured way to donate to charity while retaining some control over the assets.

- The remaining trust assets pass to the donor's heirs after a specific term, potentially offering tax benefits.

- It is crucial to define the trust's key components clearly to avoid future legal complications.

Looking for another form?

Form popularity

FAQ

A charitable lead trust is an irrevocable trust designed to provide financial support to one or more charities for a period of time, with the remaining assets eventually going to family members or other beneficiaries. Charitable lead trusts are often considered to be the inverse of a charitable remainder trust.

The equivalent income interest rate is compared with the Sec.Accordingly, because D retains an interest at least equal to the right to all income from the property in the CRUT, the entire value of the corpus of the CRUT is includible in D's gross estate.

A charitable lead trust works by donating payments out of the trust to charity, for a set amount of time. After that period expires, the balance of the trust is then paid out to the beneficiary.

If an individual establishes a charitable remainder trust for his or her life only, the trust assets will be included in his or her gross estate under IRC section 2036. The amount included, however, will wash out as an estate tax charitable deduction under IRC section 2055.

A charitable remainder trust (CRT) is an irrevocable trust that generates a potential income stream for you, as the donor to the CRT, or other beneficiaries, with the remainder of the donated assets going to your favorite charity or charities.

Currently, a trust is required to file income tax returns if, during a taxable year it has gross income of $600 or more, or any amount of taxable income.Because a charitable remainder trust is ordinarily tax-exempt, the trust will calculate net income at the trust level, but will pay no tax.

A split-interest trust other than an IRC Section 664 charitable remainder trust must file Form 1041 with Form 5227 if it has $600 of gross income or any taxable income during the year.For charitable remainder trusts, there is no requirement that the named charity even know of its impending gift.

A grantor charitable lead unitrust is a gift plan defined by federal tax law that allows an individual to retain ultimate possession of an asset while making a generous gift to charity.Each year, the trustee pays a fixed percentage of the unitrust's current value, as revalued annually, to charity.

The executor or personal representative of an estate must file Form 1041 when a domestic estate has gross income during the tax year of $600 or more. A 1041 tax return must also be filed if one or more of the estate's beneficiaries are nonresident aliens even if it earned less than $600.