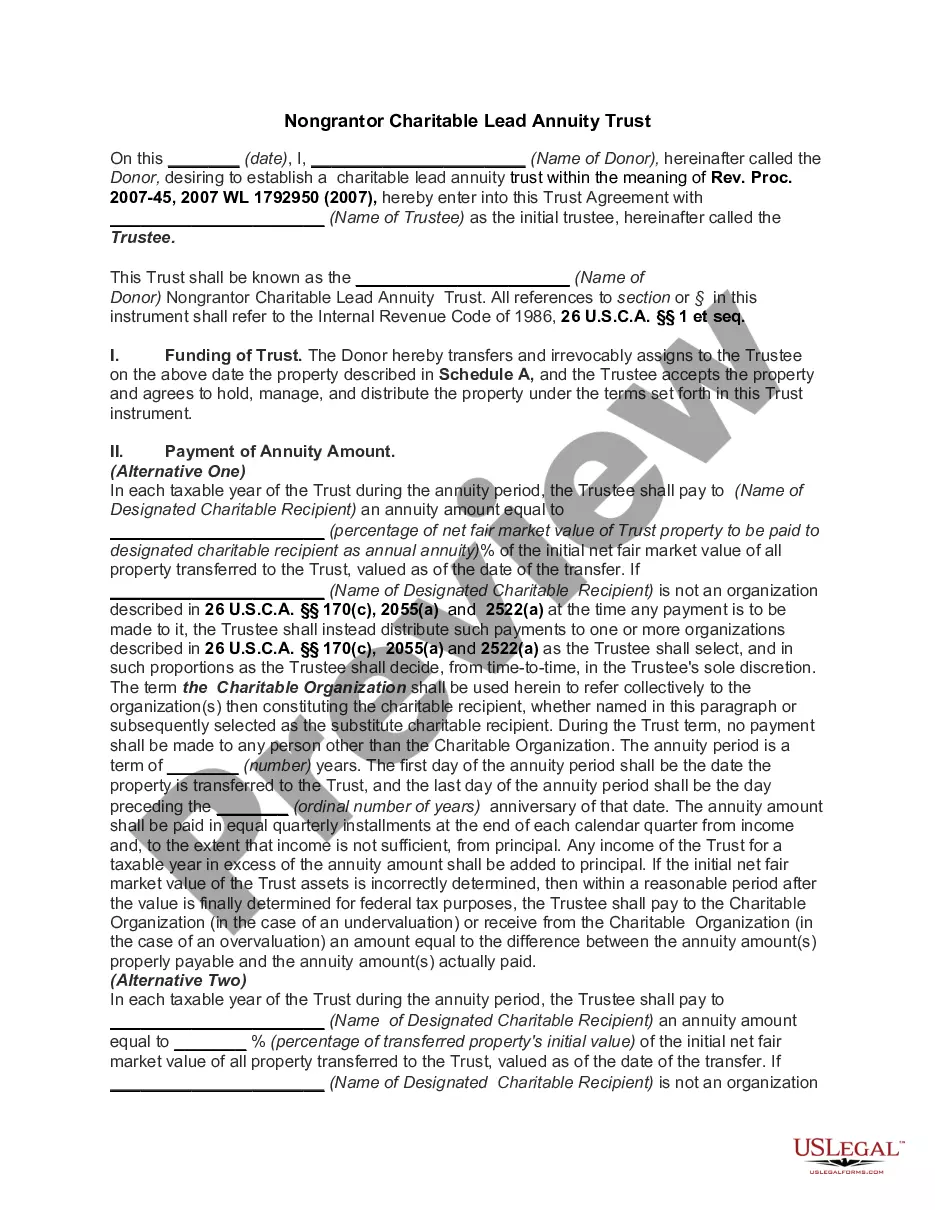

Charitable Inter Vivos Lead Annuity Trust

Understanding this form

The Charitable Inter Vivos Lead Annuity Trust is a legal document allowing a donor to establish a trust that provides income to a charitable organization for a specified number of years. After the specified term, the remaining assets return to the donor or their designated beneficiaries. This trust differs from a charitable remainder trust as the donor does not receive an immediate income tax deduction, and the income generated within the trust is taxed at trust rates rather than the donor's individual rates.

Key parts of this document

- Identification of the Grantor and Trustee along with their addresses.

- Transfer of property into the trust as specified in Schedule A.

- Definition of the annuity amount to be paid to the charity.

- Details on the distribution of trust assets after the annuity period ends.

- Trustee powers, responsibilities, and processes for managing the trust.

- Compliance with specific tax regulations to maintain its charitable status.

When to use this document

This form is appropriate when an individual wishes to make charitable contributions while maintaining control of their assets during their lifetime. It is useful for individuals looking to support a charity over a set number of years, while also planning for the future distribution of their wealth to family members or other beneficiaries after the charitable term.

Who this form is for

- Individuals who want to support charitable organizations while retaining their assets.

- Donors looking for a structured way to contribute over time.

- Those planning for the transition of assets to heirs after charitable payments are fulfilled.

- Individuals seeking tax-related benefits through established charitable giving methods.

How to complete this form

- Identify and enter the names and addresses of both the Grantor and the Trustee.

- Specify the property being transferred to the trust in Schedule A.

- Determine and enter the terms of the annuity amount to be paid to the charitable organization.

- Outline the distribution plan for the remaining trust funds upon completion of the charitable term.

- Sign and date the trust document in the presence of a notary (if required in your state).

Notarization requirements for this form

This form does not typically require notarization unless specified by local law. It's advisable to verify whether additional steps are needed in your specific jurisdiction.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Common mistakes

- Failing to clearly specify the annuity amount can lead to tax issues.

- Not transferring the property into the trust correctly, which may invalidate the trust.

- Overlooking the need for regular updates to the trust based on changing tax laws.

Why complete this form online

- Instant download provides immediate access to the legal document.

- Editability allows customization to meet individual preferences and needs.

- Guided instructions simplify the process of completing the trust.

Main things to remember

- A charitable lead trust provides payments to a charity while preserving assets for future generations.

- This trust structure can help manage tax liabilities effectively.

- Completing the form correctly is crucial for compliance with legal standards.

Looking for another form?

Form popularity

FAQ

Currently, a trust is required to file income tax returns if, during a taxable year it has gross income of $600 or more, or any amount of taxable income.Because a charitable remainder trust is ordinarily tax-exempt, the trust will calculate net income at the trust level, but will pay no tax.

Charitable Contributions DeductionIf you take the standard deduction on your 2020 tax return, you can deduct up to $300 for cash donations to charity you made during the year.For instance, joint filers can claim up to $600 for cash donations on their 2021 return. The 2021 deduction won't reduce your AGI, either.

Reduce Your Taxes with a Charitable Income Tax Deduction. If the CRT is funded with cash, the donor can use a charitable deduction of up to 60% of Adjusted Gross Income (AGI); if appreciated assets are used to fund the trust, up to 30% of their AGI may be deducted in the current tax year.

Transfers to charitable lead trusts during lifetime can provide tax benefits to the donor, and can avoid inclusion of the transferred property in the gross estate of the donor for federal estate tax purposes at death.

A charitable lead trust works by donating payments out of the trust to charity, for a set amount of time. After that period expires, the balance of the trust is then paid out to the beneficiary.

All qualified and nonqualified nongrantor charitable lead trusts are required to file Form 1041 U.S. Income Tax Return for Estates and Trusts. Inter vivos nongrantor trusts are required to make estimated tax payments.

A charitable lead trust is an irrevocable trust designed to provide financial support to one or more charities for a period of time, with the remaining assets eventually going to family members or other beneficiaries. Charitable lead trusts are often considered to be the inverse of a charitable remainder trust.

Because the charitable bequest is not paid from income, no charitable income tax deduction can be taken on the Form 1041, which is the fiduciary income tax return.

This holiday season, donate to charity and give yourself the gift of an attractive tax break.If you itemize on your taxes meaning your deductions exceed the 2019 standard deduction of $12,200 for singles and $24,400 for married couples you can write off the value of your charitable donations.