Inter Vivos Grantor Charitable Lead Annuity Trust

About this form

An Inter Vivos Grantor Charitable Lead Annuity Trust (CLAT) is an irrevocable split-interest trust designed to benefit charitable organizations. During the trust's term, a set annuity is paid to chosen charitable beneficiaries, with the remaining principal ultimately distributed to non-charitable beneficiaries. This arrangement can provide significant tax benefits, absorbing gift, estate, and potentially income tax deductions under certain conditions as outlined in the Internal Revenue Code. Unlike other types of trusts, the CLAT facilitates philanthropic intentions while retaining control over the remaining assets for future beneficiaries.

Key parts of this document

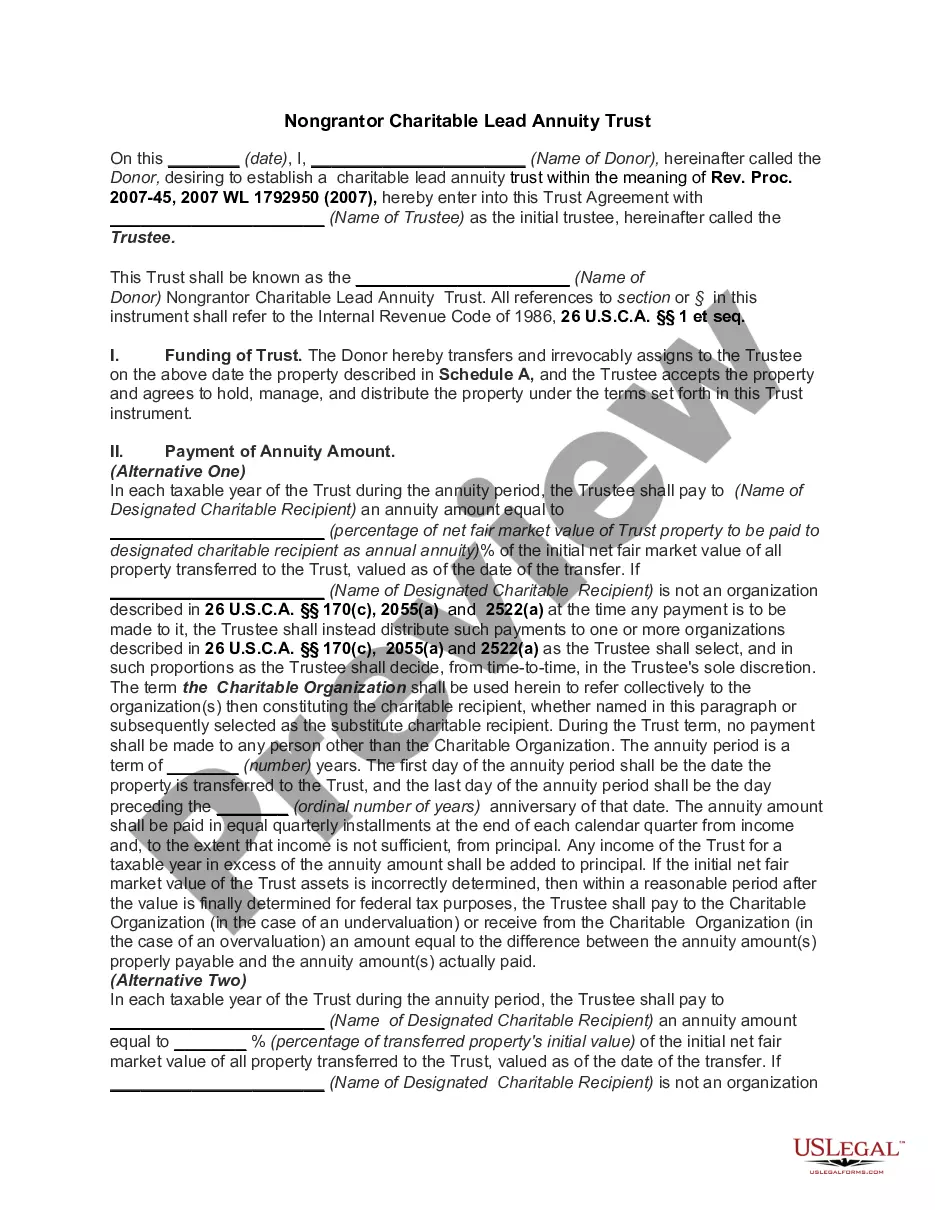

- Donor information: Name and address of the individual establishing the trust.

- Trustee details: Name and designation of the initial trustee who will manage the trust.

- Annuity payment clause: Specifies the amount and terms for payments to charitable recipients.

- Distribution upon termination: Outlines how trust assets are distributed after the annuity term ends.

- Prohibited transactions clause: Establishes guidelines to prevent self-dealing and other incompatible actions.

- Governing law clause: Indicates which stateâs laws govern the trust.

When to use this form

This form is typically used when an individual wishes to create a Charitable Lead Annuity Trust while still alive, to support charitable causes of their choice while ensuring that remaining assets will benefit non-charitable beneficiaries in the future. It is particularly relevant for individuals looking to maximize their tax deductions while making philanthropic contributions, especially if they have substantial assets to contribute.

Who should use this form

- Individuals wishing to donate to charity while retaining control of trust assets.

- Wealthy donors looking for tax benefits related to charitable contributions.

- Persons with specific charitable designations that they wish to support over a defined period.

- Those wanting to ensure a continuation of support for selected charities after their passing.

Instructions for completing this form

- Initiate by entering the date the trust is established.

- Fill in your name and address as the donor establishing the trust.

- Designate the initial trustee responsible for managing the trust.

- Specify the charitable organization(s) that will receive the annuity payments.

- Define the annuity amount and the duration of the annuity payment period.

- Sign and date the trust agreement along with witnesses as required.

Notarization guidance

This form does not typically require notarization unless specified by local law. However, notarization can provide additional legal assurance of the trust's authenticity.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Common mistakes

- Failing to clearly define the charitable organization beneficiaries.

- Incorrectly calculating the annuity amount, which can affect tax deductions.

- Neglecting to consult state-specific requirements, leading to legal issues.

- Not properly executing the trust agreement, including the necessary signatures.

Benefits of using this form online

- Convenience of accessing and downloading the form anytime.

- Easy to edit the template to fit specific needs and preferences.

- Reliability of professionally drafted material created by licensed attorneys.

Legal use & context

- The CLAT is legally binding once completed and accepted by the trustee.

- Provides strategic tax benefits under federal tax codes for eligible contributions.

- Must comply with IRS regulations to maintain its charitable deduction status.

Summary of main points

- A charitable lead annuity trust can provide support to charities while benefiting the donor tax-wise.

- Proper completion of the form is essential for the trust's effectiveness and legal standing.

- Consult local laws to ensure compliance and effectiveness of the trust established.

Looking for another form?

Form popularity

FAQ

Transfers to charitable lead trusts during lifetime can provide tax benefits to the donor, and can avoid inclusion of the transferred property in the gross estate of the donor for federal estate tax purposes at death.

It is widely understood that a CRUT can hold an Unmarketable Asset and that the grantors can act as trustee. However, an Independent Trustee should be considered and may be required in certain circumstances, such as valuing the Unmarketable Asset.

Currently, a trust is required to file income tax returns if, during a taxable year it has gross income of $600 or more, or any amount of taxable income.Because a charitable remainder trust is ordinarily tax-exempt, the trust will calculate net income at the trust level, but will pay no tax.

A charitable lead trust is an irrevocable trust designed to provide financial support to one or more charities for a period of time, with the remaining assets eventually going to family members or other beneficiaries. Charitable lead trusts are often considered to be the inverse of a charitable remainder trust.

A charitable lead trust works by donating payments out of the trust to charity, for a set amount of time. After that period expires, the balance of the trust is then paid out to the beneficiary.

Advantages of a Charitable Trust Charitable trusts provide more tax benefits than just income tax deductions. If set up correctly, they can also reduce estate taxes and preserve the value of highly appreciated assets that you may have in your portfolio.

CRTs are exempt from income tax. The CRT assumes the grantor's adjusted cost basis and holding period in the property. If the CRT sells appreciated property, neither the grantor nor the CRT will pay immediate income tax on the sales.

All qualified and nonqualified nongrantor charitable lead trusts are required to file Form 1041 U.S. Income Tax Return for Estates and Trusts. Inter vivos nongrantor trusts are required to make estimated tax payments.