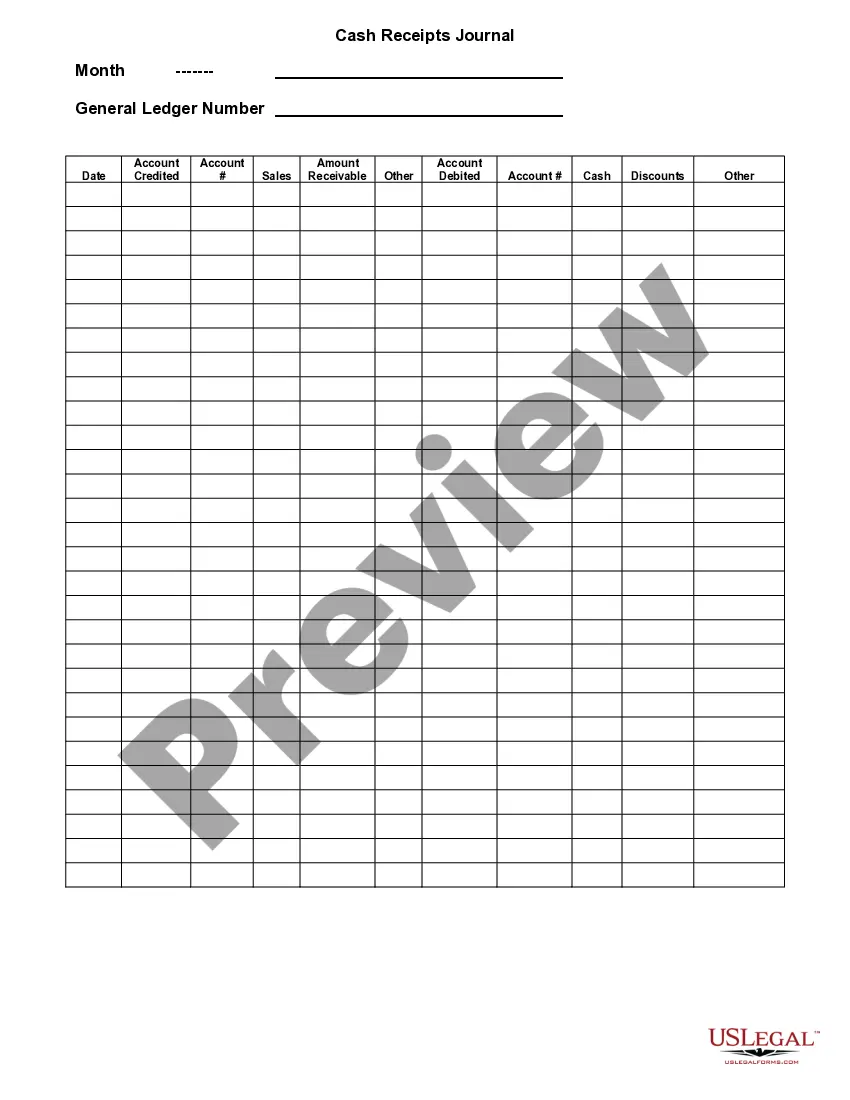

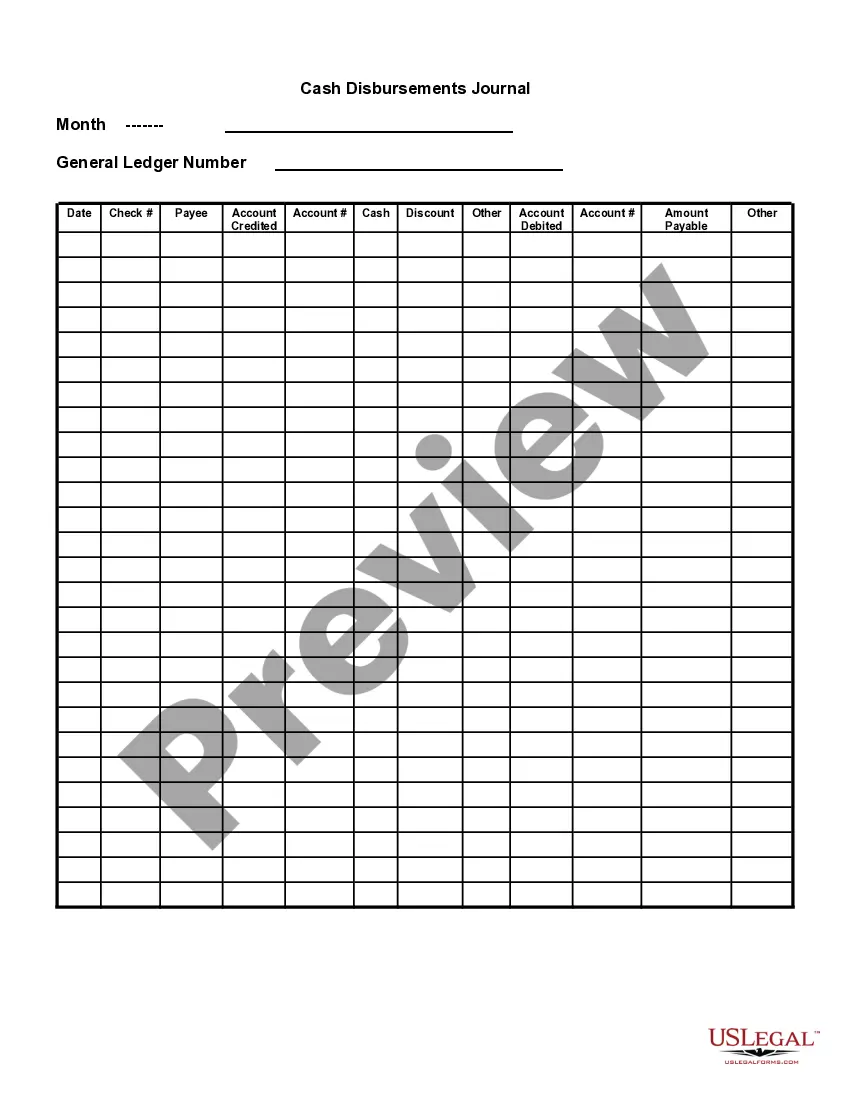

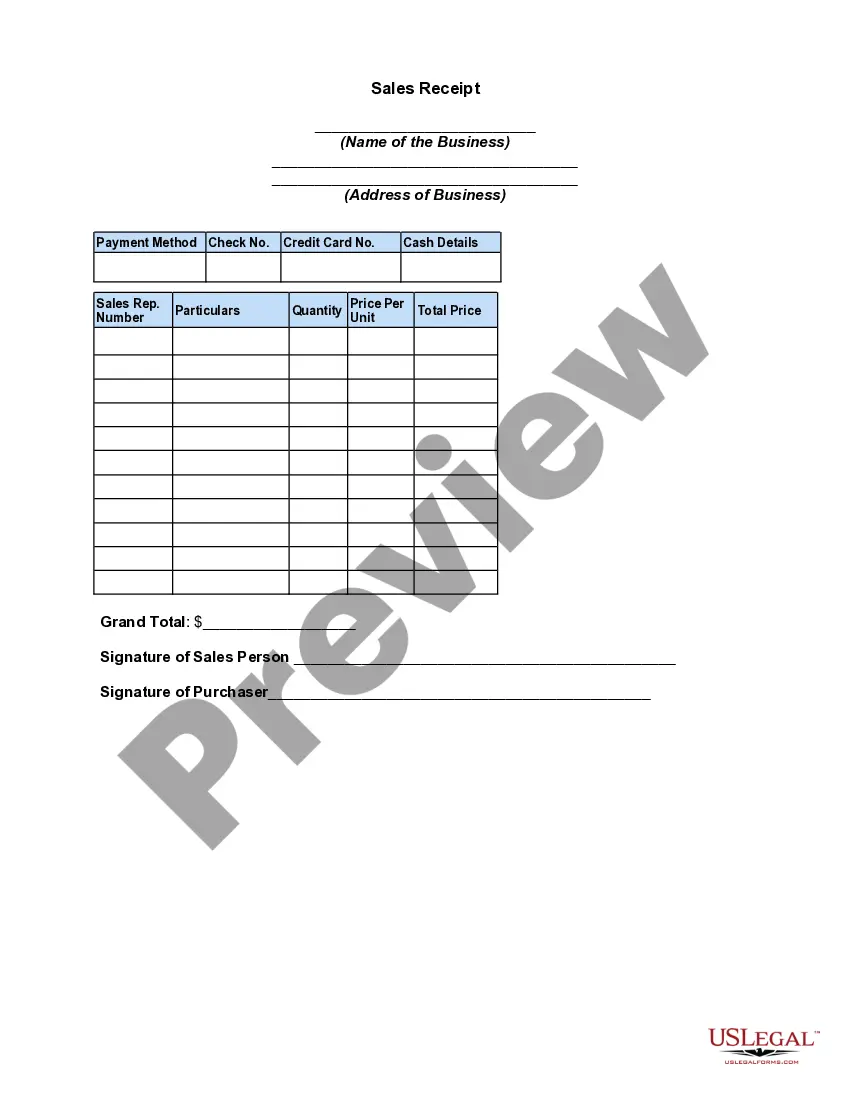

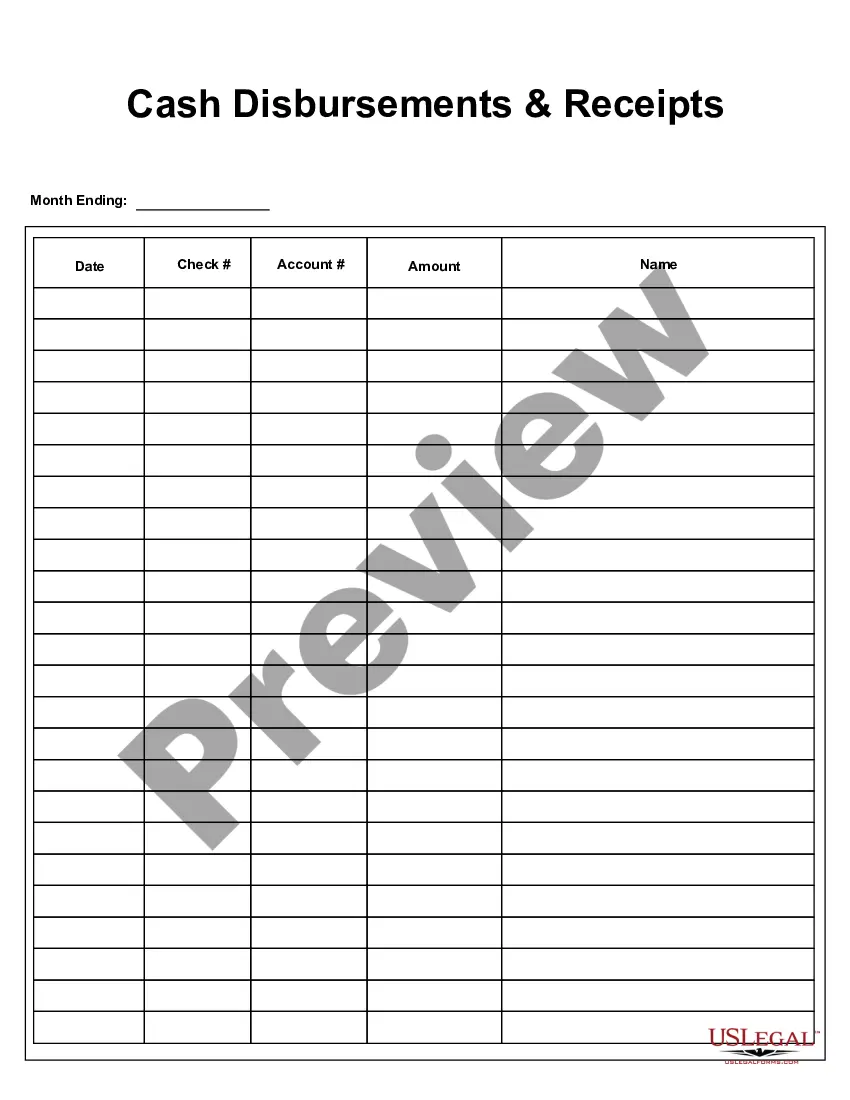

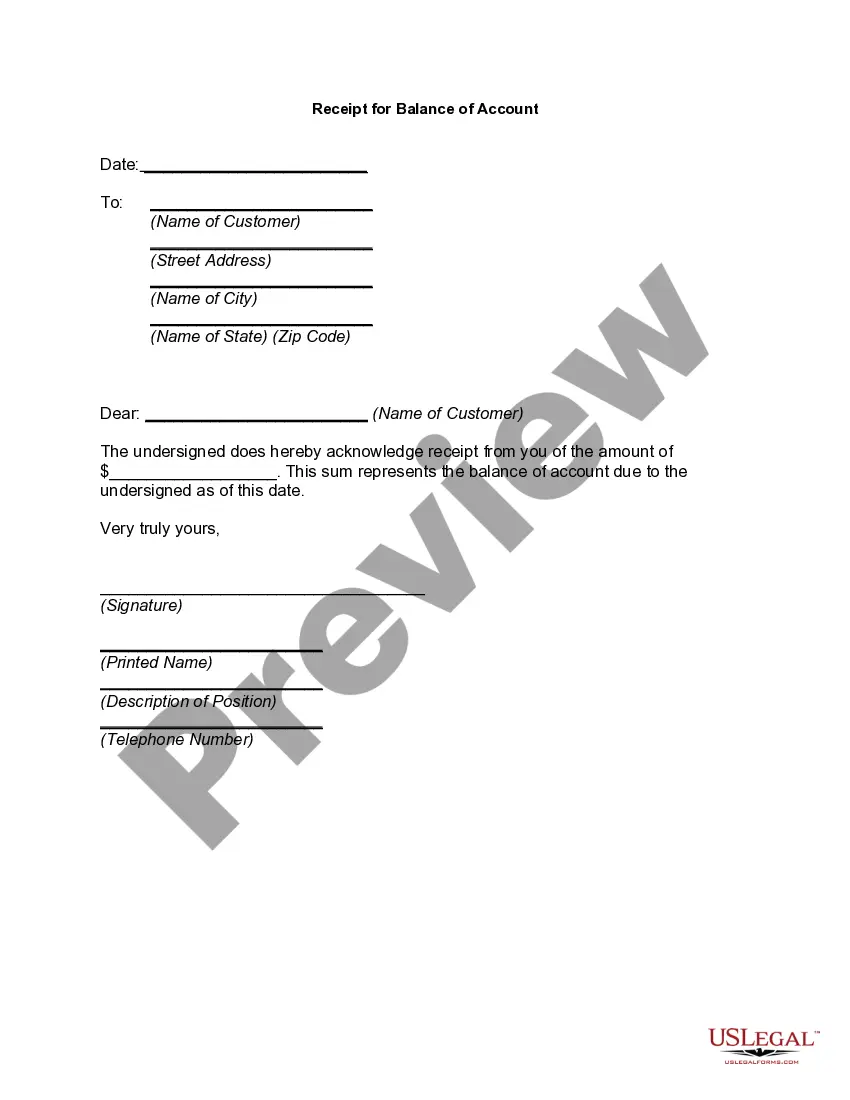

Pennsylvania Cash Receipts Control Log

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Cash Receipts Control Log?

You may spend time online searching for the legal document format that meets the federal and state requirements you need.

US Legal Forms provides thousands of legal forms that are reviewed by experts.

You can easily download or print the Pennsylvania Cash Receipts Control Log from the service.

If available, use the Preview button to review the format as well. If you wish to obtain another version of the form, use the Search field to find the format that suits your requirements.

- If you already have a US Legal Forms account, you can Log In and click the Download button.

- Then you can complete, edit, print, or sign the Pennsylvania Cash Receipts Control Log.

- Every legal document format you purchase belongs to you forever.

- To obtain another copy of the purchased form, go to the My documents tab and click the corresponding button.

- If this is your first time using the US Legal Forms website, follow the simple instructions below.

- First, ensure that you have selected the correct format for your county/area of your choice.

- Refer to the form description to ensure you have chosen the right form.

Form popularity

FAQ

Here are controls: Strong tone at the top; Leadership communicates importance of quality; Accounts reconciled monthly; Leaders review financial results; Log-in credentials; Limits on check signing; Physical access to cash, Inventory; Invoices marked paid to avoid double payment; and, Payroll reviewed by leaders.

Strong internal controls are necessary to prevent mishandling of funds and safeguard assets. They protect both the University and the employees handling the cash.

Generally, the primary incompatible duties that need to be segregated are:Authorization or approval.Custody of assets.Recording transactions.Reconciliation/Control Activity.

Examples of segregation of duties:The person who requisitions the purchase of goods or services should not be the person who approves the purchase. The person who approves the purchase of goods or services should not be the person who reconciles the monthly financial reports.

These controls include written policies and procedures, adequate separation of duties, cash receipt forms, timely deposits, security of funds, establishing accountability, reconciliation procedures, and supervisory reviews.

The internal control that most effectively assures the secure handling of cash is separation of duties. Having different people receive cash, prepare the transmittal, and reconcile the ledger sheets attain this.

Ten Internal Control Practices to Safeguard Smaller BusinessesExpense Management.Supporting Documentary Evidence.Policies and Procedures.Segregation of Duties (SOD)Access Rights and Roles to Critical Financial Applications.Monitoring and Management Oversight.Critical Spreadsheets.More items...?

Best practices:Record cash receipts when received.Keep funds secured.Document transfers.Give receipts to each customer.Don't share passwords.Give each cashier a separate cash drawer.Supervisors verify cash deposits.Supervisors approve all voided refunded transactions.

Segregation of duties serves two key purposes: It ensures that there is oversight and review to catch errors. It helps to prevent fraud or theft because it requires two people to collude in order to hide a transaction.

A. Internal control over cash disbursements is more effective when payments are made by check, rather than by cash, except for incidental amounts that are paid out of petty cash. b. Cash payments are generally made only after specific control procedures have been followed.