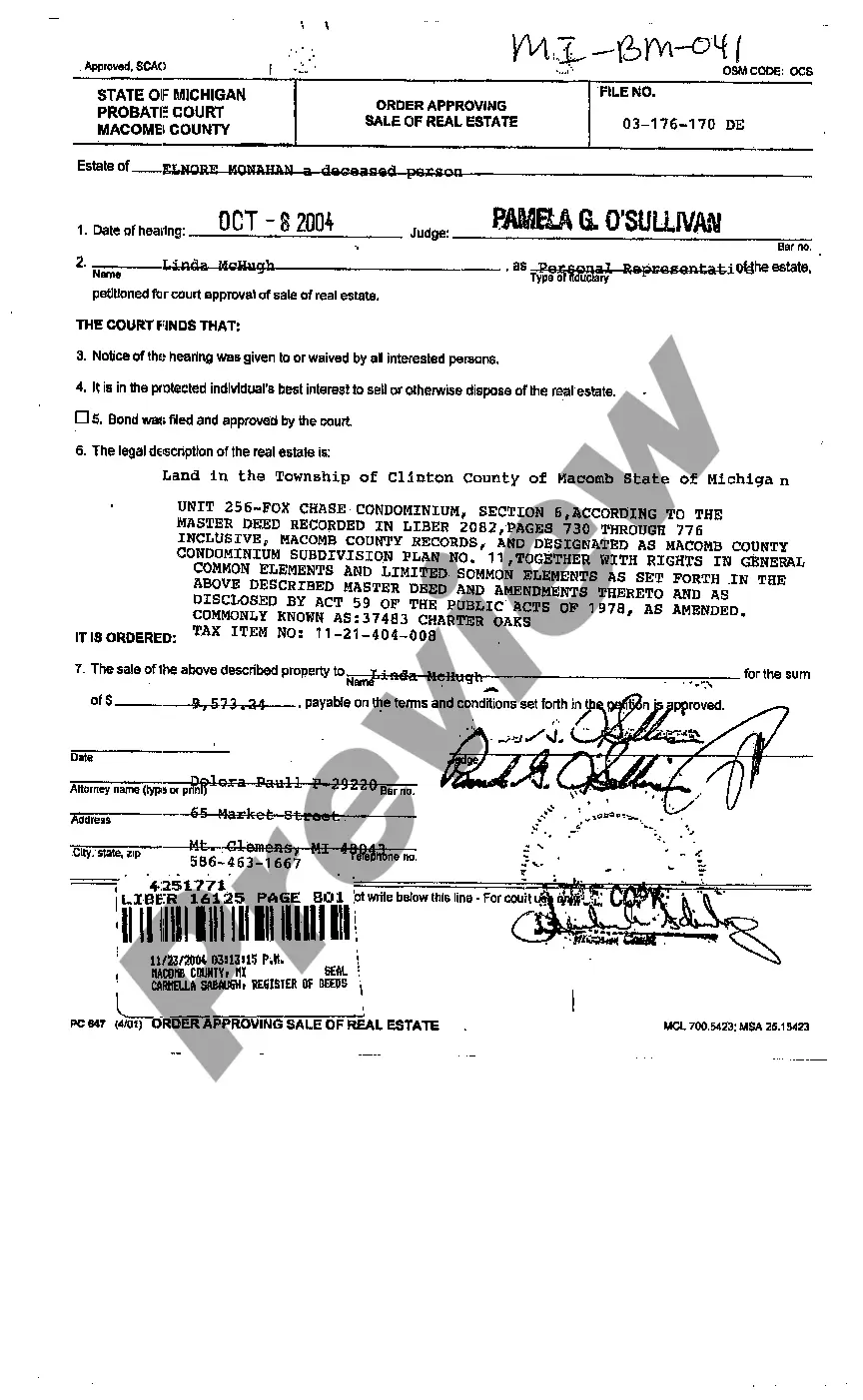

Pennsylvania Sec.3101 Payments to Family and Funeral Directors — Section (b) Deposit Accounts are accounts that are established to facilitate the transfer of money to pay funeral expenses. These accounts are used to provide funds to family members or funeral directors to cover funeral and burial costs in Pennsylvania. They are typically established upon the death of an individual, with the funds coming from the estate of the deceased. There are two types of Pennsylvania Sec.3101 Payments to Family and Funeral Directors — Section (b) Deposit Accounts: 1. Revocable Accounts: These accounts are established with funds that can be withdrawn or changed at any time by the account holder. The funds remain in the account until the funeral expenses are paid. 2. Irrevocable Accounts: These accounts are established with funds that cannot be changed or withdrawn until the funeral expenses are paid. The funds are held in the account until the funeral expenses are paid in full.

Pennsylvania Sec.3101 Payments to Family and Funeral Directors - Section (b) Deposit Accounts

Description

Key Concepts & Definitions

SEC 3101 Payments to Family and Funeral Directors: This terminology reflects the transactional processes associated with payments made to family members and funeral directors, typically from an estate following the demise of an individual. Personal representative or duly appointed personal indicates an individual, often stipulated in a will or appointed by a court, who manages the affairs of the deceased. Letters of administration are legal documents issued to authorize these representatives to manage the decedent's estate.

Step-by-Step Guide: Handling SEC 3101 Payments

- Determine the personal representative: Confirm who has been appointed as the personal representative or whom the court has issued grant letters to oversee the decedent's affairs.

- Secure letters of administration: If not already appointed, apply for these through a court to gain legal authority over the estate.

- Identify payables: Catalog payments that need to be made to family members or funeral directors.

- Execute payments: Ensure payments are made in accordance with legal stipulations and estate plans.

Risk Analysis

Payment distributions involving deceased estates carry risks such as misidentification of duly appointed personal representatives or incorrect payment amounts. Litigation risks arise if the distribution contradicts the terms set by the representative of the decedent. Verifying all details thoroughly and consulting online lawyer services for free legal advice can mitigate these risks.

Common Mistakes & How to Avoid Them

- Insufficient Documentation: Always ensure the personal representative has valid letters of administration.

- Miscommunication: Clarify all payouts with stakeholders to prevent disputes.

- Lack of professional advice: Utilize legal information from credible sources or online lawyer services to navigate complex estate laws.

Pros & Cons of SEC 3101 Payments

- Pros: Ensures legal distribution of estate assets; can provide quick resolution in paying off estate debts.

- Cons: Can lead to disputes if not properly managed; potential for legal complications if the personal representative is not duly appointed.

FAQ

- What is a personal representative? This is legally appointed individual to manage the estate of a deceased person.

- How do I get letters of administration? Apply at a local probate court or consult an online lawyer to guide the application process.

- What should I do if there's a dispute over payments? Consult legal advice immediately to resolve conflicts in line with estate laws and the decedent's wishes.

How to fill out Pennsylvania Sec.3101 Payments To Family And Funeral Directors - Section (b) Deposit Accounts?

Handling official documentation requires attention, accuracy, and using properly-drafted blanks. US Legal Forms has been helping people countrywide do just that for 25 years, so when you pick your Pennsylvania Sec.3101 Payments to Family and Funeral Directors - Section (b) Deposit Accounts template from our library, you can be certain it meets federal and state laws.

Working with our service is straightforward and quick. To obtain the required paperwork, all you’ll need is an account with a valid subscription. Here’s a brief guideline for you to get your Pennsylvania Sec.3101 Payments to Family and Funeral Directors - Section (b) Deposit Accounts within minutes:

- Remember to carefully examine the form content and its correspondence with general and law requirements by previewing it or reading its description.

- Look for an alternative formal blank if the previously opened one doesn’t suit your situation or state regulations (the tab for that is on the top page corner).

- Log in to your account and download the Pennsylvania Sec.3101 Payments to Family and Funeral Directors - Section (b) Deposit Accounts in the format you prefer. If it’s your first experience with our website, click Buy now to continue.

- Register for an account, decide on your subscription plan, and pay with your credit card or PayPal account.

- Choose in what format you want to obtain your form and click Download. Print the blank or upload it to a professional PDF editor to prepare it paper-free.

All documents are created for multi-usage, like the Pennsylvania Sec.3101 Payments to Family and Funeral Directors - Section (b) Deposit Accounts you see on this page. If you need them in the future, you can fill them out without re-payment - just open the My Forms tab in your profile and complete your document any time you need it. Try US Legal Forms and prepare your business and personal paperwork quickly and in full legal compliance!

Form popularity

FAQ

For example, any assets in a living trust or jointly owned under joint tenancy with survivorship rights are considered non-probate assets. In addition, a payable-on-death account is exempt. Retirement accounts are also considered immune from the probate process.

Section 3392 states that all creditor claims shall be paid in the following order: (1) the costs of administering the decedent's estate, which includes any probate fees, attorneys' fees, or personal representative commissions; (2) the family exemption, which is $3,500.00 for each family member who resided with the

The Uniform Probate Code (commonly abbreviated UPC) is a uniform act drafted by National Conference of Commissioners on Uniform State Laws (NCCUSL) governing inheritance and the decedents' estates in the United States.

In Pennsylvania, it is only necessary to probate if the decedent owned assets, whether financial or real estate holdings, solely in their name which did not already have a beneficiary designated. Such assets are called probate assets, and in order to convey ownership of them it is necessary to probate.

The UPC deals with a variety of topics concerning the estates of Pennsylvania residents. For example, the UPC dictates the necessary actions for appointing a guardian to a disabled or incapacitated person. It also deals with the formation and regulation of trusts.

§ 3102. Settlement of small estates on petition. The authority of the court to award distribution of personal property under this section shall not be restricted because of the decedent's ownership of real estate, regardless of its value.

Letters testamentary or of administration shall not be granted after the expiration of 21 years from the decedent's death, except on the order of the court, upon cause shown. § 3153.

The purpose of drafting the Uniform Probate Code (UPC) was to provide a uniform set of laws that could be used by all jurisdictions in the United States to govern the administration of estates and the settlement of disputes between heirs.