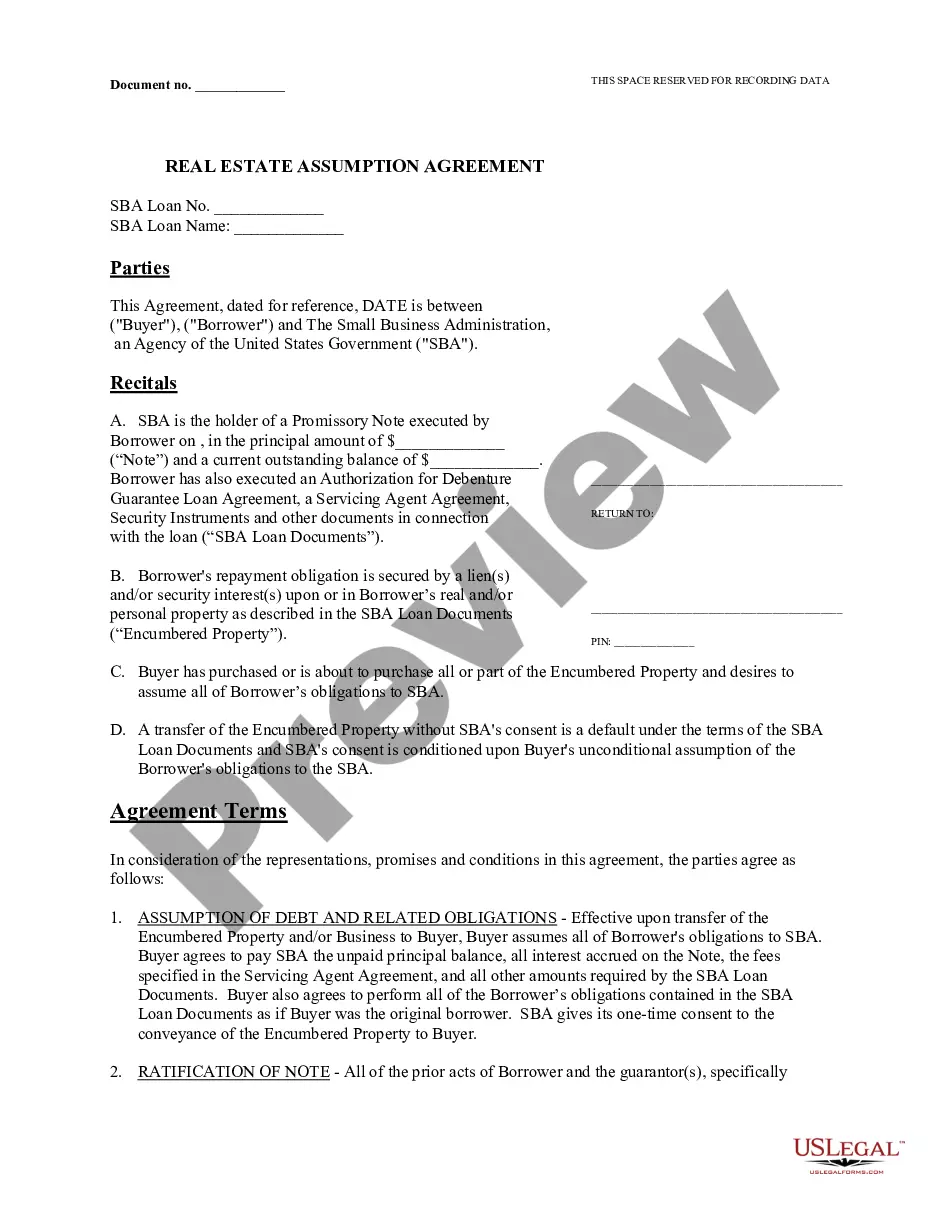

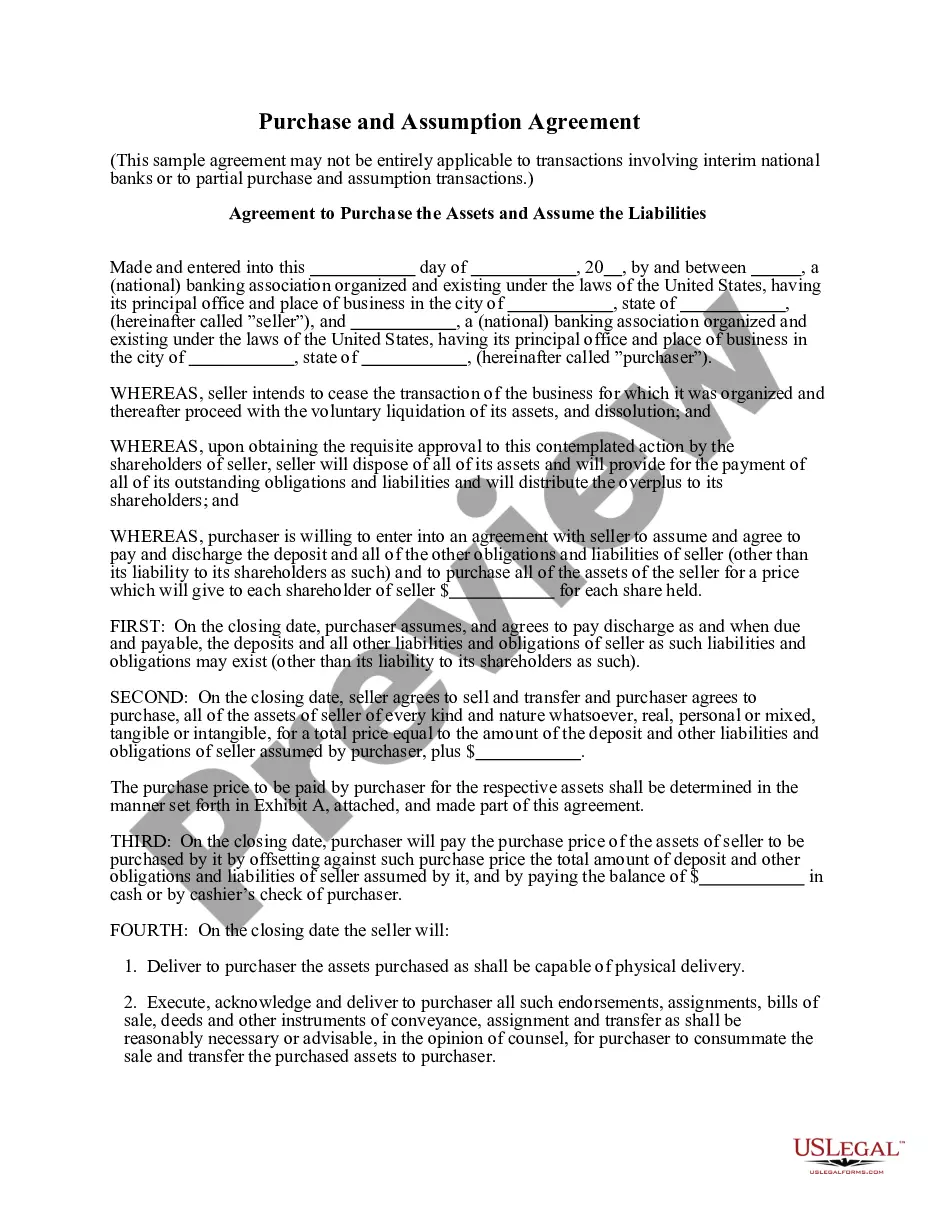

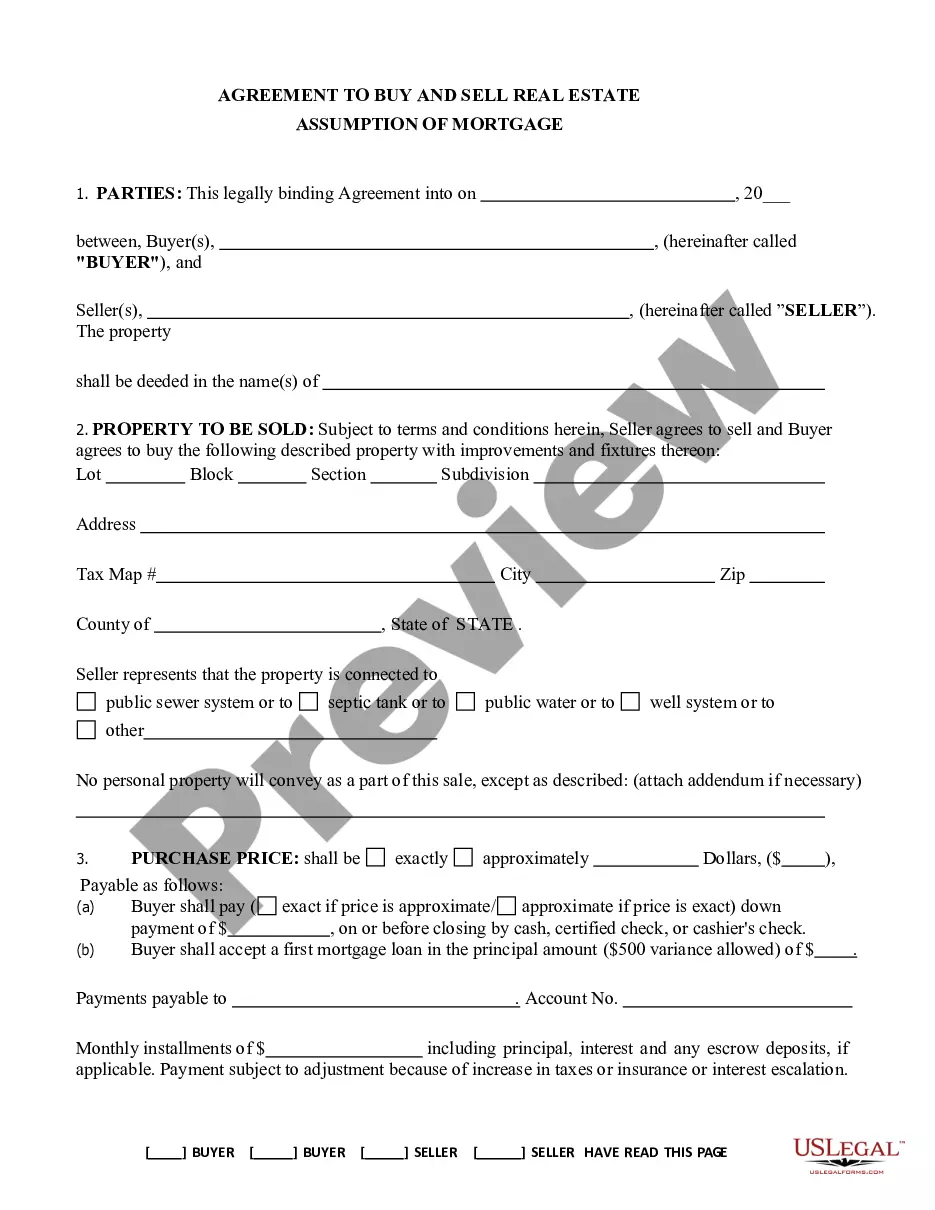

Oklahoma Veterans Affairs Assumption AgreementAgreement

About this form

The Veterans Affairs Assumption Agreement is a legal document that enables a new buyer (the Grantee) to take over the mortgage obligations from the original borrower (the Mortgagor) with the lender (the Mortgagee). This agreement ensures that the buyer assumes the responsibility for repaying the VA Debt and releases the original borrower from any future liabilities associated with the loan. This form is specifically tailored for transactions involving properties financed through the Department of Veterans Affairs loan programs, distinguishing it from standard assumption agreements used in non-VA mortgage transactions.

Main sections of this form

- Identification of the Mortgagor, Mortgagee, and Grantee.

- Details of the existing VA Debt and associated promissory note.

- Provisions stating the Granteeâs agreement to assume the debt and obligations.

- Clauses outlining the lien requirements on the property.

- Signatures of all parties involved, including acknowledgment requirements from a notary public.

Common use cases

This form should be used when a buyer intends to purchase a property currently under a VA loan, and they wish to assume the existing mortgage. It is particularly relevant when the seller (original Mortgagor) wants to transfer their debt obligations to the buyer. This agreement protects the seller from future liability regarding the loan after it has been assumed by the buyer, thereby facilitating a smoother transfer of ownership.

Who should use this form

- Original borrowers (Mortgagors) transferring their property to a new buyer.

- New buyers (Grantees) who are assuming the mortgage and wish to formalize their agreement with the lender.

- Lenders (Mortgagees) involved in VA loans who require a formal acknowledgment of the debt assumption.

Steps to complete this form

- Fill in the date of the agreement at the top of the form.

- Identify all the parties involved: Mortgagor (seller), Mortgagee (lender), and Grantee (buyer).

- Provide details of the existing VA Debt, including the debt amount, promissory note number, and property description.

- Ensure all parties agree to the terms by signing the document in the designated areas.

- Arrange for the notarization of the signed document to ensure its legal validity.

Is notarization required?

Yes, this form must be notarized to be legally valid. Each party must sign the document in the presence of a notary public, who will verify their identity and witness their signatures. US Legal Forms offers integrated online notarization, making it easy and secure to complete this step with legal equivalence from anywhere.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Typical mistakes to avoid

- Failing to have the agreement signed by all parties.

- Leaving out critical details about the VA Debt or property description.

- Not notarizing the document, which may be required for legal enforceability.

Why use this form online

- Convenient access to a legally drafted document that saves time and effort.

- Editable templates allow you to customize the agreement to fit your specific situation.

- Reliability from using forms created by experienced attorneys, ensuring legal compliance.

Looking for another form?

Form popularity

FAQ

Anyone can assume a VA mortgage as long as their income and credit qualify but children of veterans can't get VA loans themselves (unless, of course, they join the military as well). You have to be a current service member, veteran or surviving spouse of a veteran to qualify for a VA loan.

A loan can be denied by the automated underwriting system for any number of reasons. It could be that something was input wrong. It could be because something was reported wrong on your credit.

How Often Do Underwriters Deny VA Loans? About 15% of VA loan applications get denied, so if your's isn't approved, you're not alone. If you're denied during the automated underwriting stage, you may be able to seek approval through manual underwriting.

Application errors. Double check your loan paperwork. Change in employment. Keep your employment consistent throughout the loan process. Change in credit. Borrower Delays. Factors beyond your control.

Yet another benefit: VA loans are assumable. A VA loan assumption allows a borrower to take over the terms of an existing mortgage, even if they aren't a military service member, veteran or eligible surviving spouse. This type of transaction can benefit both homebuyers and sellers.

Processing. Once a loan officer has a completed loan file, income documents and a credit report, the application will be submitted to a VA underwriter for processing. Underwriters can take as long as 14 days to render a decision on underwriting a loan for individuals with a solid credit background.

Underwriters may view certain employment changes as unreliable sources of income. If a job change cannot be avoided, speak to your loan officer about new documentation or verification of income. Errors: In simpler cases, VA loans may be rejected because you made a mistake on the documents somewhere.

For a VA mortgage assumption to take place, the following conditions must be met: The existing loan must be current. If not, any past due amounts must be paid at or before closing. The buyer must qualify based on VA credit and income standards.

Veterans with VA mortgages can have their VA home loan assumed by someone else, also called a VA loan assumption. If your plans, goals, or needs changed and you need to get out of a VA loan one option is to sell your home but an alternative option is an assumable mortgage, a buyer takes over the loan.