Purchase and Assumption Agreement

Understanding this form

The Purchase and Assumption Agreement is a legal document used in transactions where a healthy bank buys the assets and assumes the liabilities of a struggling bank. This form facilitates the transfer of deposits and other obligations, making it a common practice endorsed by the Federal Deposit Insurance Corporation (FDIC) to stabilize failing banks. It can be customized to meet specific needs and differs from other legal forms by focusing on asset purchase and liability assumption as a single cohesive transaction.

Form components explained

- Identification of the seller and purchaser, including their banking associations.

- Details about the seller's intention to liquidate and dissolve.

- Terms of the purchase price and the offset against assumed liabilities.

- Obligations of the seller to provide necessary documentation for asset transfer.

- Warranties from the seller regarding its condition at the closing date.

- Provisions for the closing date and any applicable approvals needed.

When to use this form

This agreement is essential during transactions where a compliant bank or thrift seeks to take over another's assets and liabilities. It is frequently employed when a bank is about to cease operations due to financial difficulties, allowing the purchaser to gain control of insured deposits and other liabilities swiftly, supporting financial stability in the banking sector.

Who should use this form

- Banking institutions engaged in the acquisition of assets and liabilities from another bank.

- Shareholders of a failing bank looking to liquidate assets properly.

- Legal representatives of both buyer and seller involved in the transaction.

- Financial regulators overseeing the transition to ensure compliance with banking laws.

Instructions for completing this form

- Identify the parties involved, including names and addresses of the seller and purchaser.

- Specify the closing date and ensure it aligns with the sellerâs liquidation timeline.

- Detail the purchase price and the liabilities being assumed.

- Include any additional exhibits or terms required for the asset transfer.

- Ensure signatures are obtained from all authorized representatives of both parties.

Notarization guidance

This form does not typically require notarization unless specified by local law. Users should verify any state-specific regulations that may impose additional notarization requirements.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Typical mistakes to avoid

- Failing to accurately specify all assets and liabilities involved in the transaction.

- Not obtaining necessary approvals from shareholders or regulatory bodies.

- Leaving out essential details regarding the closing date or terms of payment.

- Inadequate documentation or signatures from both parties involved.

Benefits of completing this form online

- Convenient access to templates that can be downloaded and edited according to specific needs.

- Ensures compliance with legal standards and reduces the chance of errors in drafting.

- Provides a straightforward process that eliminates the need for in-person appointments.

- Access to reliable support and guidance if questions arise during completion.

Legal use & context

- This agreement is legally binding upon completion and execution by both involved parties.

- All terms stated in the document should comply with federal and state banking laws.

- Failure to follow the proper execution process may lead to legal disputes or unenforceability.

Quick recap

- The Purchase and Assumption Agreement is crucial for banks acquiring assets and liabilities.

- The form must be tailored to cover essential transaction details accurately.

- Understand the requirements for completion and ensure all regulatory approvals are in place.

- Utilizing the form online provides convenience and assurance of legal compliance.

Looking for another form?

Form popularity

FAQ

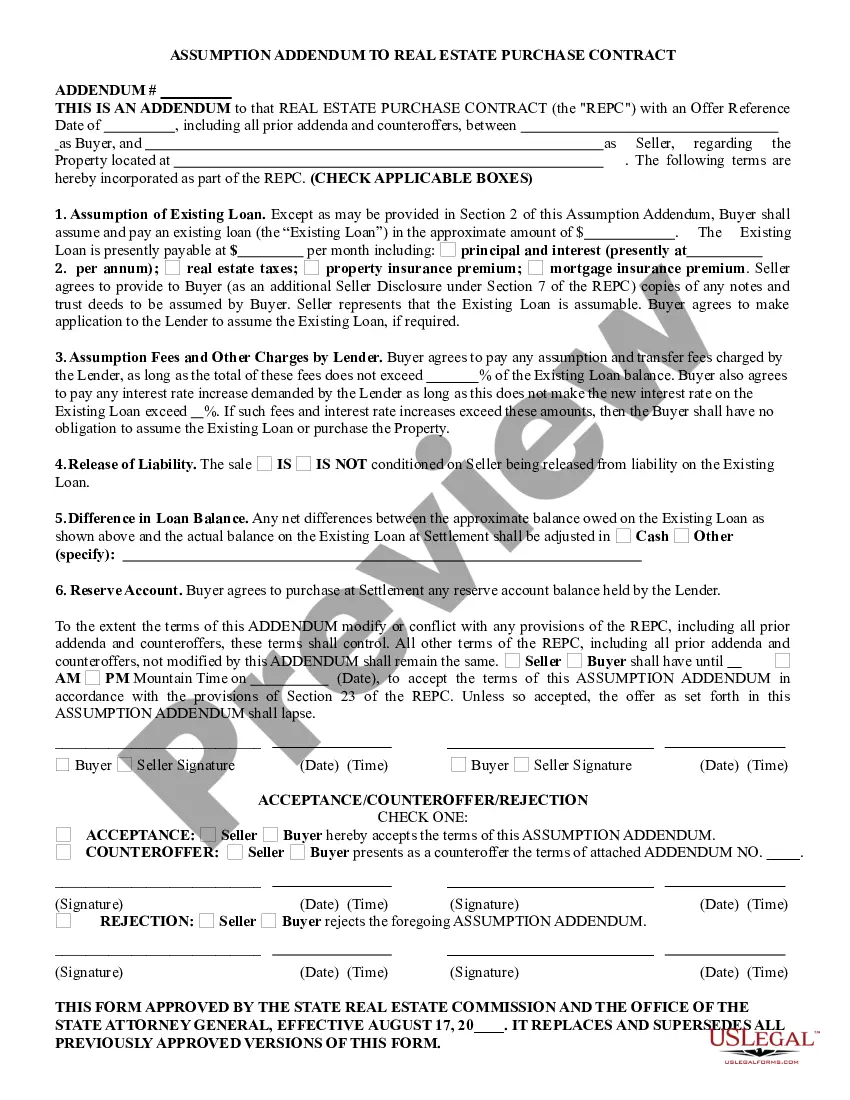

Under the payoff method, the FDIC must payout $250,000 but may pay out more, up to the original $350,00 value of the deposit, depending on the amount of proceeds received when the bank is liquidated. Under the purchase and assumption method, the bank is completely absorbed, and all accounts are paid their full value.

An assignment and assumption agreement is used after a contract is signed, in order to transfer one of the contracting party's rights and obligations to a third party who was not originally a party to the contract.

A loan assumption agreement is an agreement between a lender, original borrower, and a new borrower, where the new borrower agrees to assume responsibility for the debt owed by original borrower. These agreements are commonly seen in mortgages and real estate.

Purchase and assumption is a transaction in which a healthy bank or thrift purchases assets and assumes liabilities (including all insured deposits) from an unhealthy bank or thrift. It is the most common and preferred method used by the Federal Deposit Insurance Corporation (FDIC) to deal with failing banks.

Purchase and Assumption Transaction. This is the preferred and most common method, under which a healthy bank assumes the insured deposits of the failed bank. Insured depositors of the failed bank immediately become depositors of the assuming bank and have access to their insured funds.

Keep in mind that the average loan assumption takes anywhere from 45-90 days to complete. The more issues there are with underwriting, the longer you'll have to wait to finalize your agreement.

An assumption clause is a provision in a mortgage contract that allows the seller of a home to pass responsibility for the existing mortgage to the buyer of the property. In other words, the new homeowner assumes the existing mortgage and?along with it?ownership of the property that secures the loan.