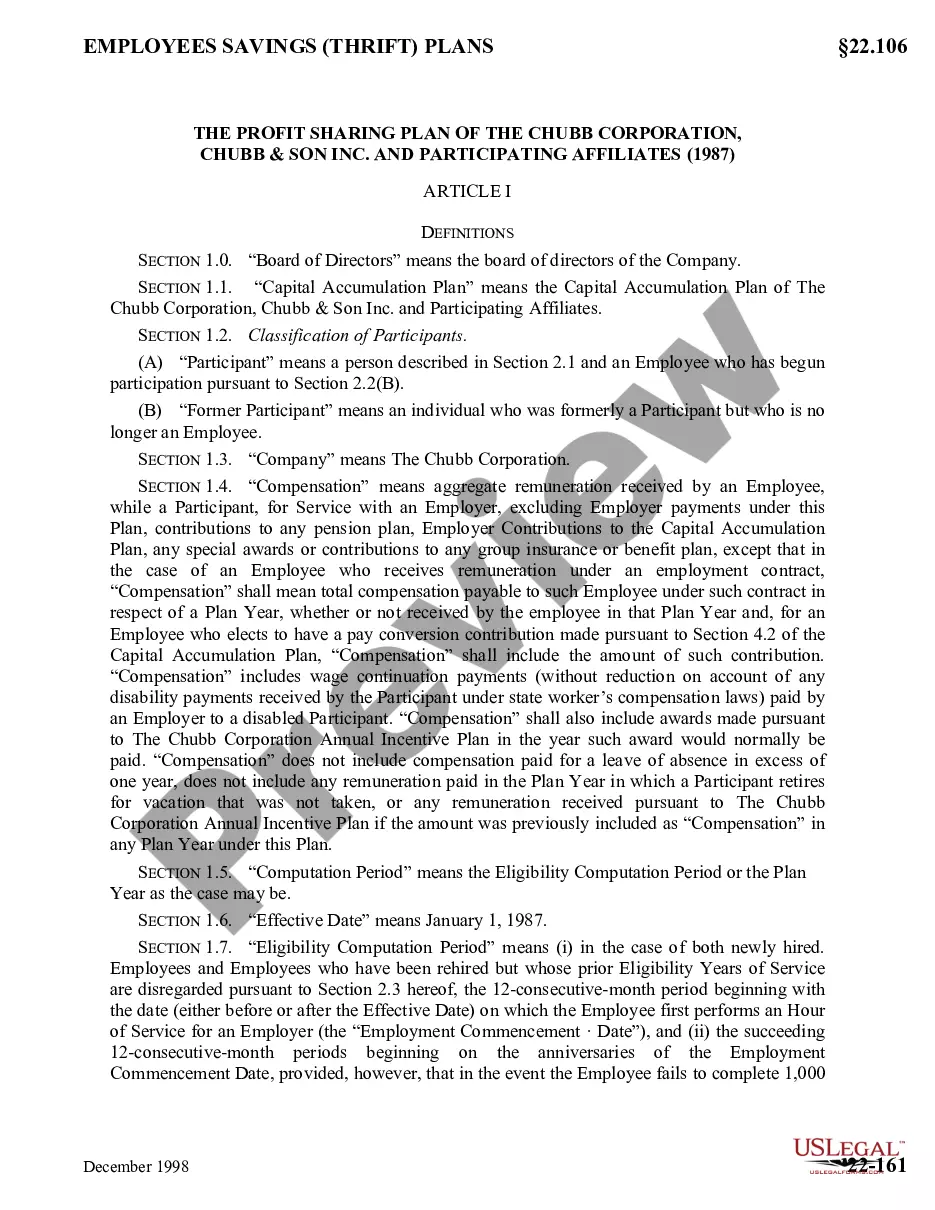

22-118E 22-118E . . . Employee Savings Thrift Plan under which three types of contributions can be made: (a) those permitted under a qualified Cash Or Deferred Arrangement ("CODA") under Section 401(k) of Internal Revenue Code, (b) those made by participating companies matching 40% of CODA contributions, and (c) additional voluntary employee contributions made by participants who elect maximum CODA contribution and wish to save additional amounts out of after-tax dollars

Ohio Employees Savings Thrift Plan

Category:

State:

Multi-State

Control #:

US-CC-22-118E

Format:

Word;

Rich Text

Instant download

Description

Free preview

How to fill out Employees Savings Thrift Plan?

You may commit hours on-line attempting to find the authorized file format that fits the federal and state requirements you will need. US Legal Forms supplies a large number of authorized varieties that happen to be evaluated by pros. You can actually acquire or print the Ohio Employees Savings Thrift Plan from my support.

If you already possess a US Legal Forms account, you may log in and click on the Down load key. Afterward, you may comprehensive, change, print, or signal the Ohio Employees Savings Thrift Plan. Every single authorized file format you acquire is yours forever. To acquire another backup for any bought kind, check out the My Forms tab and click on the corresponding key.

If you work with the US Legal Forms site the first time, follow the simple directions listed below:

- Initially, be sure that you have selected the best file format for the county/metropolis of your choosing. Browse the kind description to make sure you have chosen the appropriate kind. If readily available, utilize the Preview key to search with the file format at the same time.

- If you wish to locate another edition of your kind, utilize the Research area to get the format that suits you and requirements.

- When you have identified the format you desire, just click Buy now to continue.

- Pick the costs prepare you desire, type in your qualifications, and register for your account on US Legal Forms.

- Full the financial transaction. You should use your bank card or PayPal account to cover the authorized kind.

- Pick the formatting of your file and acquire it to the device.

- Make alterations to the file if necessary. You may comprehensive, change and signal and print Ohio Employees Savings Thrift Plan.

Down load and print a large number of file templates while using US Legal Forms web site, which offers the biggest variety of authorized varieties. Use expert and status-specific templates to handle your company or individual demands.

Form popularity

FAQ

The TSP is a defined contribution plan, meaning that the retirement income you receive from your TSP account will depend on how much money you put into your account during your working years and the earnings accumulated over time (and, if you're eligible, agency or service contributions and their earnings).

There are multiple advantages to rollover contributions to the TSP, and you can use this option even after you retire. Rollovers allow you to consolidate your retirement savings in one place so it's easier to evaluate whether you're on target to meet your goals with the right asset allocation.

A FERS employee (generally if you were hired on or after January 1, 1984) A CSRS employee (generally if you were hired before January 1, 1984 and did not convert to FERS) A member of the uniformed services (active duty or Ready Reserve)

However, the IRS rule of 55 may allow you to receive a distribution in the year you reach age 55 or later (and before age 59½) without triggering the early penalty if your plan provides for such distributions. Any distribution would still be subject to an income tax withholding rate of 20 percent, however.

The TSP is a retirement savings and investment plan for federal employees. The purpose of the TSP is to provide retirement income through savings and tax deferred benefits that many private corporations offer their employees. The TSP is similar to private sector 401(k) plans.

Agency/Service matching contributions The first 3% is matched dollar-for-dollar by your agency or service; the next 2% is matched at 50 cents on the dollar. This means that when you contribute 5% of your basic pay, your agency or service contributes an amount equal to 4% of your basic pay to your TSP account.

Fees. While they may not have as many funds to choose from, TSP participants do have one big advantage over most 401(k) investors: lower fees. The total expense ratio, which covers both investment and administrative fees, is 0.066% for individual TSP funds.

If you earn 8% on your money per year (which is historically pretty hard for a combined stock and bond portfolio to do), you can turn that into a million dollars within 25 years. It's no wonder, then, that the average contribution years of a TSP millionaire is over 29 years.

The TSP is a retirement savings and investment plan for federal employees. The purpose of the TSP is to provide retirement income through savings and tax deferred benefits that many private corporations offer their employees. The TSP is similar to private sector 401(k) plans.

By participating in the TSP, Federal employees and uniformed service members can save part of their income for retirement, receive matching agency contributions, and reduce their current taxes.