New York Fair Credit Act Disclosure Notice

Description

How to fill out Fair Credit Act Disclosure Notice?

US Legal Forms - one of the largest collections of legal documents in the United States - offers a broad selection of legal document formats that you can download or print.

By using the site, you can discover thousands of forms for business and personal purposes, categorized by groups, states, or keywords. You can locate the most recent versions of documents like the New York Fair Credit Act Disclosure Notice in just a few minutes.

If you already have a membership, Log In and download the New York Fair Credit Act Disclosure Notice from your US Legal Forms library. The Download button will be visible on every form you view. You can find all previously downloaded forms in the My documents section of your account.

Process the payment. Use your Visa or Mastercard or PayPal account to complete the transaction.

Select the format and download the document to your device. Edit. Fill out, modify, print, and sign the downloaded New York Fair Credit Act Disclosure Notice. Each template you add to your account does not have an expiration date and belongs to you indefinitely. Therefore, to download or print another copy, simply visit the My documents section and click on the form you desire. Access the New York Fair Credit Act Disclosure Notice with US Legal Forms, one of the most extensive collections of legal document formats. Utilize thousands of professional and state-specific templates that fulfill your business or personal needs and requirements.

- If you are using US Legal Forms for the first time, here are simple instructions to get you started.

- Ensure you have selected the correct form for your city/county.

- Click the Review button to examine the form's details.

- Check the form information to confirm that you've chosen the right document.

- If the form does not meet your needs, use the Lookup field at the top of the screen to find one that does.

- Once you are satisfied with the form, finalize your choice by clicking the Acquire now button.

- Then, select your preferred payment plan and provide your details to register for an account.

Form popularity

FAQ

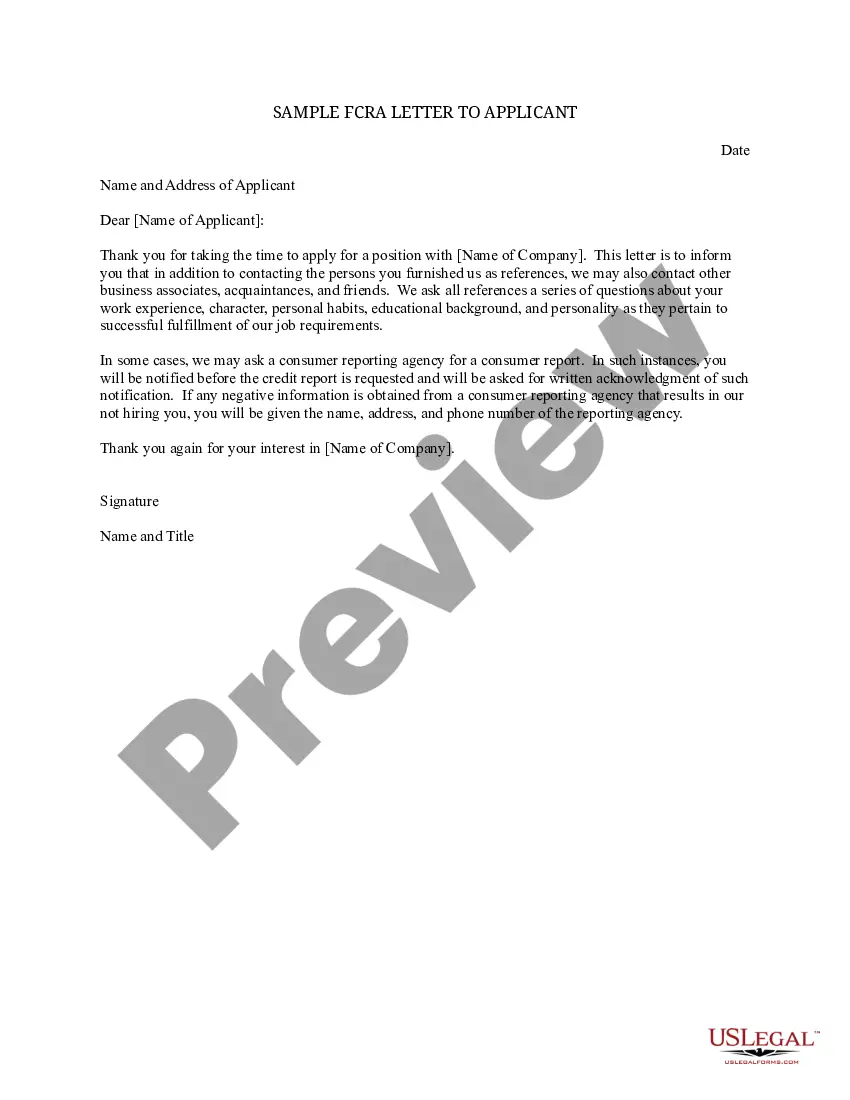

The FCRA gives you the right to be told if information in your credit file is used against you to deny your application for credit, employment or insurance. The FCRA also gives you the right to request and access all the information a consumer reporting agency has about you (this is called "file disclosure").

A creditor must disclose a consumer's credit score and information relating to a credit score on a risk-based pricing notice when the score of the consumer to whom the creditor extends credit or whose extension of credit is under review is used in setting the material terms of credit.

A Credit Score Disclosure alerts a consumer of their FICO scores, defines what a FICO is, informs how FICO scores affect their access to consumer credit and provides contact information for the bureaus.

The Act (Title VI of the Consumer Credit Protection Act) protects information collected by consumer reporting agencies such as credit bureaus, medical information companies and tenant screening services. Information in a consumer report cannot be provided to anyone who does not have a purpose specified in the Act.

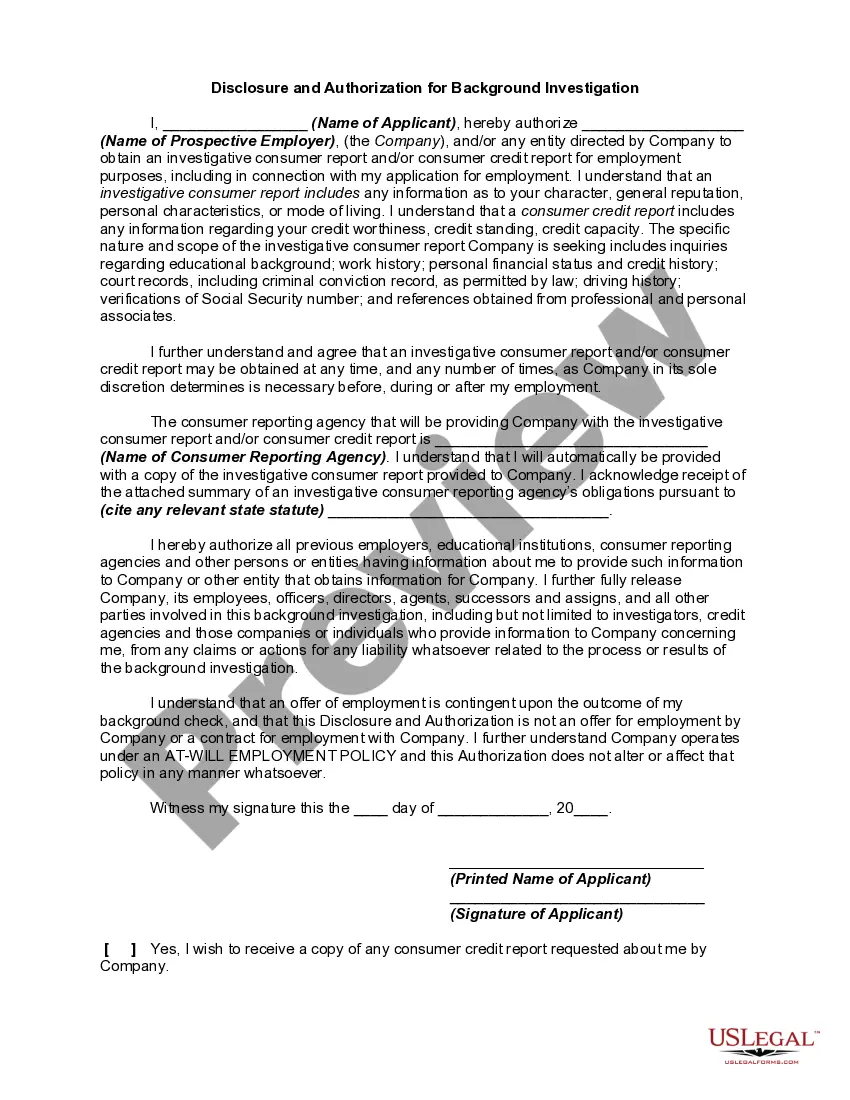

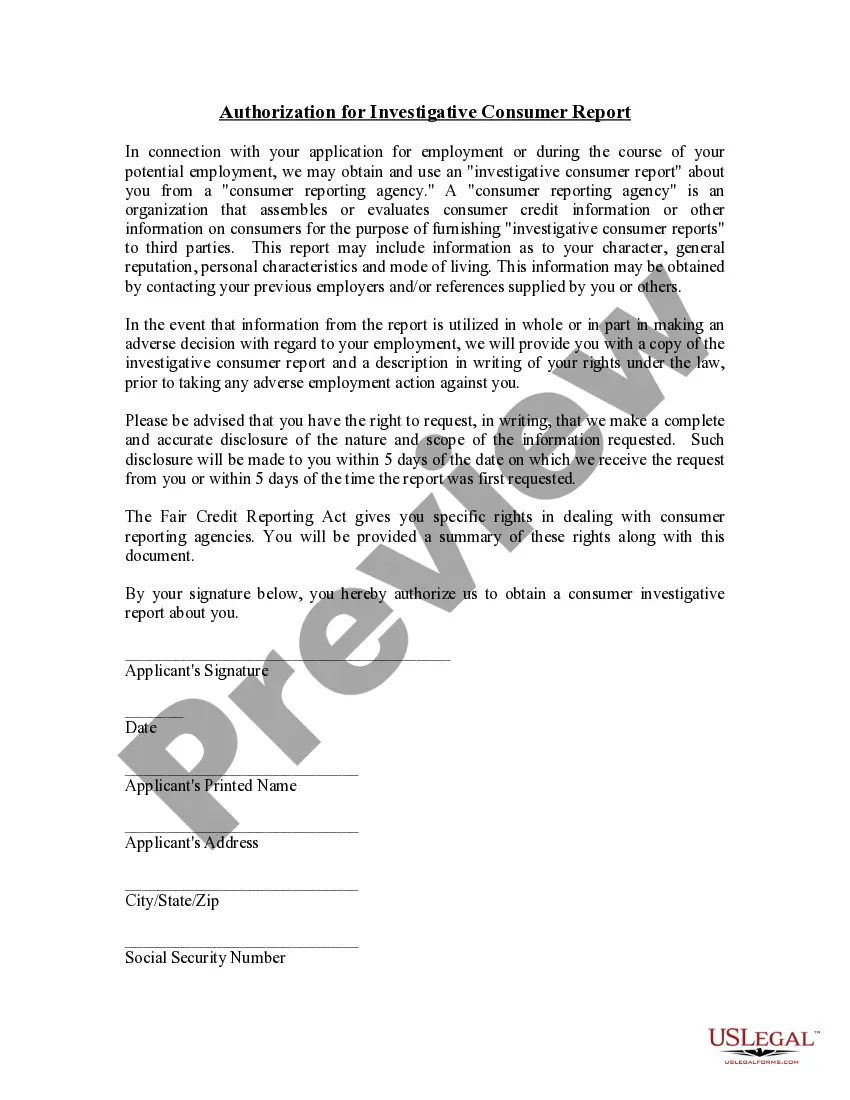

Under the FCRA, an employer may not run a background check on a prospective employee without first providing "a clear and conspicuous disclosure . . . in a document that consists solely of that disclosure, that a consumer report may be obtained for employment purposes." For efficiency, many employers include all

Access to Your Credit Report The act requires credit reporting agencies to provide you with any information in your credit file upon request once a year. You must have proper identification. You have a right to a free copy of your credit report within 15 days of your request.

Under the FCRA, an employer may not run a background check on a prospective employee without first providing "a clear and conspicuous disclosure . . . in a document that consists solely of that disclosure, that a consumer report may be obtained for employment purposes." For efficiency, many employers include all

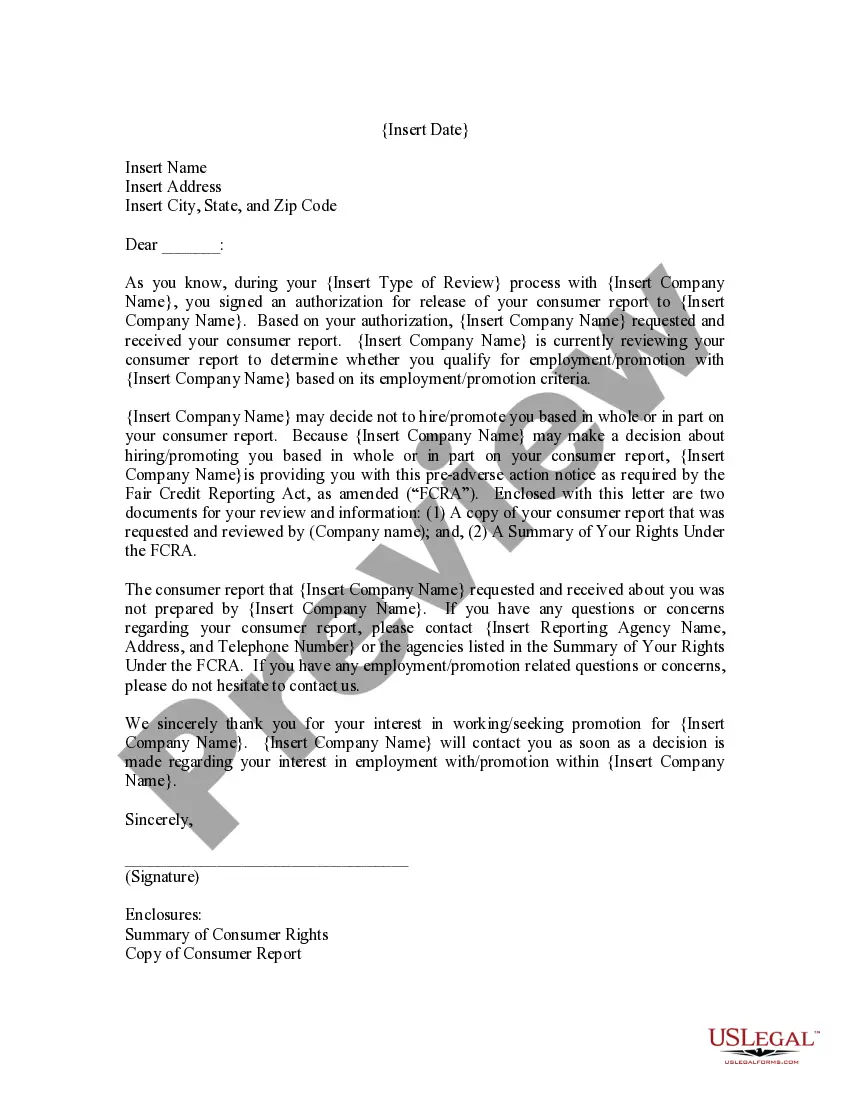

If you deny a consumer credit based on information in a consumer report, you must provide an adverse action notice to the consumer. if you grant credit, but on less favorable terms based on information in a consumer report, you must provide a risk-based pricing notice.

The Dodd-Frank Act also amended two provisions of the FCRA to require the disclosure of a credit score and related information when a credit score is used in taking an adverse action or in risk-based pricing. On December 21, 2011, the CFPB restated FCRA regulations under its authority at 12 CFR Part 1022 (76 Fed. Reg.

The Fair Credit Reporting Act describes the kind of data that the bureaus are allowed to collect. That includes the person's bill payment history, past loans, and current debts.