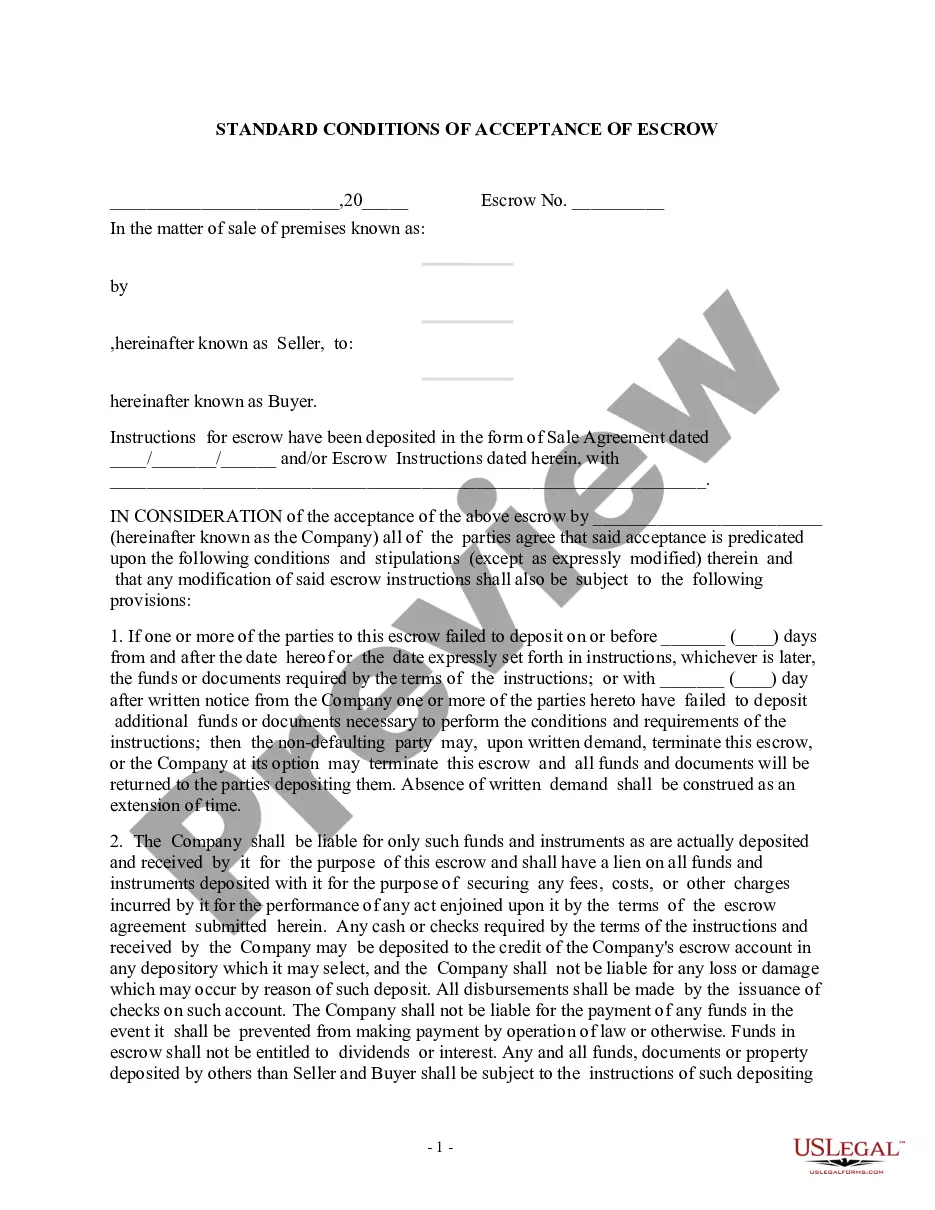

North Carolina Closing Statement

What is this form?

The Closing Statement is a crucial document used in real estate transactions, specifically for cash sales or transactions involving owner financing. This form outlines the financial aspects of the sale, detailing the costs and balances due from both the buyer and seller. Unlike other settlement statements, the Closing Statement is verified and signed by both parties to ensure accuracy and transparency in the transaction.

Key components of this form

- Balance: Summarizes overall financial results after adjusting expenses.

- Expenses: Lists all costs associated with the transaction, including title search and recording fees.

- Title Insurance: Details necessary insurance for protecting against potential title issues.

- Attorney Fees: Specifies legal costs incurred in the transaction process.

- Commissions: States any real estate commissions to be paid during the transaction.

- Notary Fee: Indicates the fee required for notarization of the document, if relevant.

- Total Adjustments: Summarizes all adjustments made throughout the document.

- Certification: Provides a section for both parties to certify the accuracy of the information contained in the form.

Common use cases

This Closing Statement should be used during the final steps of a real estate transaction, particularly when the sale is a cash transaction or when owner financing is involved. It is essential to complete this form before closing, as it helps both the buyer and seller understand all financial obligations and ensure that all terms of the sale have been met.

Who this form is for

- Buyers involved in cash purchases of real estate.

- Sellers conducting transactions that include owner financing.

- Real estate agents facilitating the closing of a property sale.

- Attorneys representing clients in real estate transactions.

Completing this form step by step

- Identify the parties involved: Clearly state the names of the buyer(s) and seller(s).

- Specify the property: Include the address and legal description of the real property being sold.

- List all expenses: Enter detailed expenses such as title insurance, attorney fees, and any other relevant costs.

- Calculate total adjustments: Summarize all credits and debits to arrive at the final amounts due.

- Obtain signatures: Ensure both the buyer and seller sign and date the form to certify its accuracy.

Does this document require notarization?

This form does not typically require notarization unless specified by local law. Notarization may enhance the form's credibility in certain jurisdictions, so check local requirements or consult with a real estate attorney if unsure.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Typical mistakes to avoid

- Failing to list all expenses leading to inaccuracies in the balance.

- Omitting signatures, which can render the form invalid.

- Not updating figures after negotiations, resulting in disputes at closing.

- Incorrectly calculating total adjustments, which may affect the final amounts due.

Advantages of online completion

- Convenient access for quick and easy download.

- Editability allows users to customize the form for their specific transaction.

- Reliability derived from forms prepared by licensed attorneys to ensure compliance with laws.

Main things to remember

- The Closing Statement is essential for documenting financial transactions in real estate sales.

- It must be completed accurately to avoid misunderstandings between parties.

- Proper signatures and dates are crucial for the legal validity of the form.

Looking for another form?

Form popularity

FAQ

The North Carolina Closing Statement is a verified document used in cash real estate sales or owner-financed deals in NC. It itemizes the sale's financials, including the balance due from each party and costs such as expenses, title insurance, attorney fees, commissions, and notary fees. It also records total adjustments and includes a Certification section for accuracy, all finalized before closing.

At closing, the Closing Statement shows who is responsible for each cost in NC real estate transactions. It lists items like title search and recording fees, title insurance, attorney fees, commissions, and notary fees, and assigns these expenses to the buyer, seller, or both as specified by the sale terms. The document helps ensure a clear allocation of costs.

Yes—the settlement date is typically the closing date for NC real estate closings. The North Carolina Closing Statement is prepared for that closing to reflect final numbers, including balances and costs, and both parties sign to confirm accuracy before funds are exchanged, ensuring transparency and agreement on the transaction details.

The key components of the North Carolina Closing Statement are Balance, Expenses, Title Insurance, Attorney Fees, Commissions, Notary Fee, Total Adjustments, and Certification. These sections show the net result after adjustments, list all costs involved in the sale, and provide a place for both parties to confirm the information.

Both the buyer and seller sign the North Carolina Closing Statement at closing and use the Certification section to confirm its accuracy. This certification ensures that the listed balances, expenses, and cost allocations are correct and agreed upon for recording the real estate transfer.

It is tailored for cash sales and owner-financed real estate deals in North Carolina and requires both parties to verify and sign the figures. This dual verification plus the specific components and allocations make it distinct from generic closing statements used primarily with financed purchases.