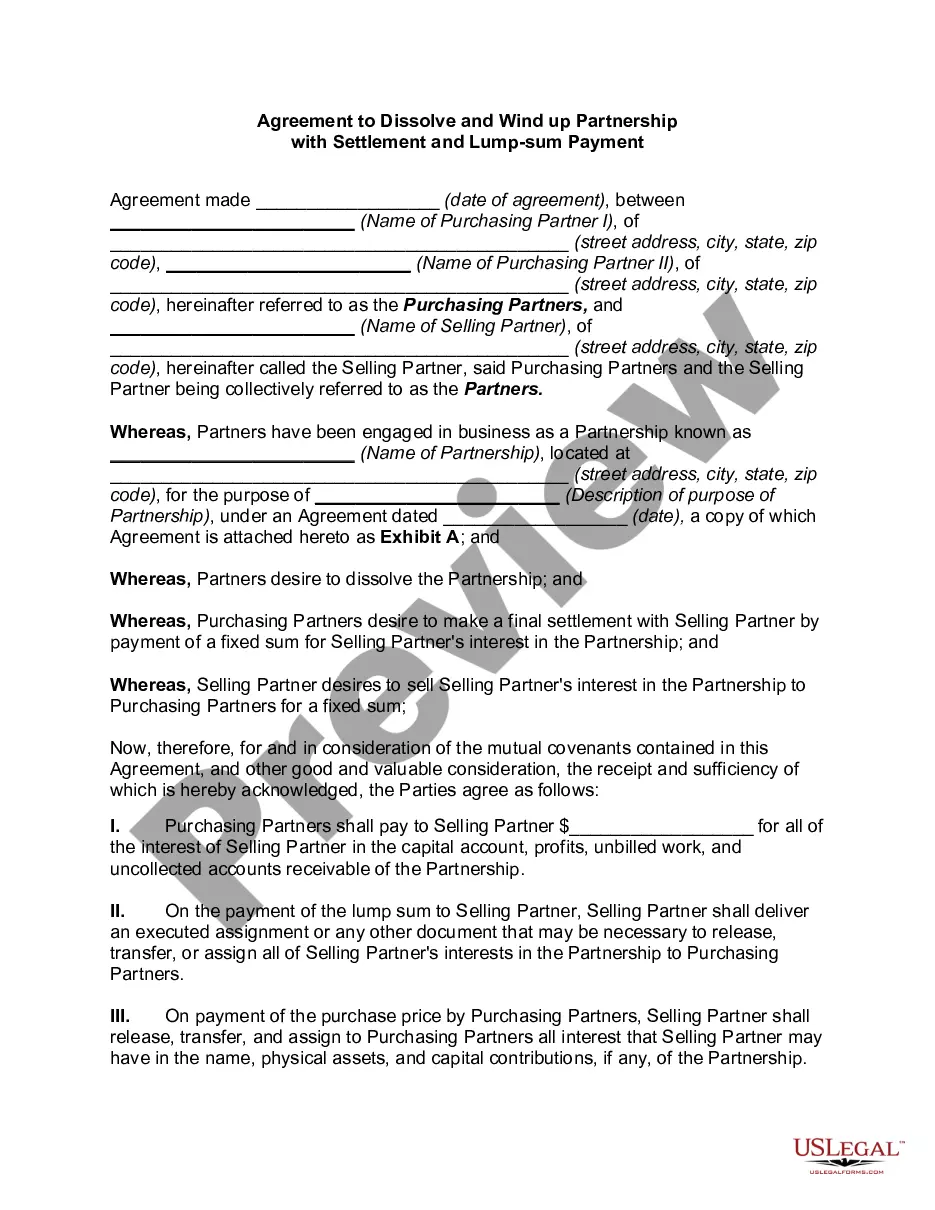

Maine Agreement to Dissolve and Wind up Partnership with Settlement and Lump Sum Payment

Description

How to fill out Agreement To Dissolve And Wind Up Partnership With Settlement And Lump Sum Payment?

You can allocate time online searching for the authentic document template that meets the federal and state requirements you need.

US Legal Forms offers thousands of verified legal forms assessed by professionals.

You can download or print the Maine Agreement to Dissolve and Wind up Partnership with Settlement and Lump Sum Payment from this service.

First, make sure you have selected the correct document template for your desired area/city. Review the form details to ensure you have chosen the right one. If available, use the Preview button to view the document template as well.

- If you possess a US Legal Forms account, you can Log In and click the Obtain button.

- After that, you can complete, modify, print, or sign the Maine Agreement to Dissolve and Wind up Partnership with Settlement and Lump Sum Payment.

- Every legal document template you purchase is yours permanently.

- To get another copy of the purchased form, go to the My documents section and click the corresponding button.

- If you are using the US Legal Forms website for the first time, follow the simple instructions below.

Form popularity

FAQ

The firm will pay the losses including the deficiency of capital firstly out of the profits, secondly out of the partner's capital and lastly by the partners individually in their profit sharing ratio.

The following four accounting steps must be taken, in order, to dissolve a partnership: sell noncash assets; allocate any gain or loss on the sale based on the income-sharing ratio in the partnership agreement; pay off liabilities; distribute any remaining cash to partners based on their capital account balances.

If a partner's capital account results in a debit balance (called capital deficiency), the deficiency can be eliminated by Making additional cash investment, if the deficient partner is solvent. Charging the deficiency as additional loss to the remaining partners, if the deficient partner is insolvent.

Liquidation by installment or piece-meal liquidation. This is a type of liquidation whereby assets are realized on a piecemeal basis and cash is distributed to partners on a periodic basis as it becomes available, that is even before all non-assets are converted into cash.

Ways of Dissolving a Partnership FirmWhen partners mutually agreed. It is the easiest way to dissolve a partnership firm since all partners have mutually agreed upon closing the partnership firm.Compulsory dissolution.Dissolution depending on certain contingent events.Dissolution by notice.Dissolution by Court.

sum liquidation of a partnership is one in which all the assets are converted into cash within a very short time, creditors are paid, and a single, lumpsum payment is made to the partners for their capital interests.

The proceeds from the sale of assets along with the contribution of the partners at the time of dissolution of the firm are first used up to pay off the external liabilities, i.e., the creditors, bank loans, bank overdrafts, bills payable etc.

On dissolution of firm, when assets are distributed, liabilities are disposed in a proper order wherein payment to third party debt is on priority, followed by amount due to partners and in the end the residual amount is divided amongst the partners in profit sharing ratio.

When one partner wants to leave the partnership, the partnership generally dissolves. Dissolution means the partners must fulfill any remaining business obligations, pay off all debts, and divide any assets and profits among themselves. Your partners may not want to dissolve the partnership due to your departure.

INSTALLMENT LIQUIDATION Involves selling of some assets, paying the liabilities of the partnership, and dividing the available cash to the partners, selling additional assets to make further payments to partners until all the assets have been sold and all cash has been distributed to the creditors and partners.