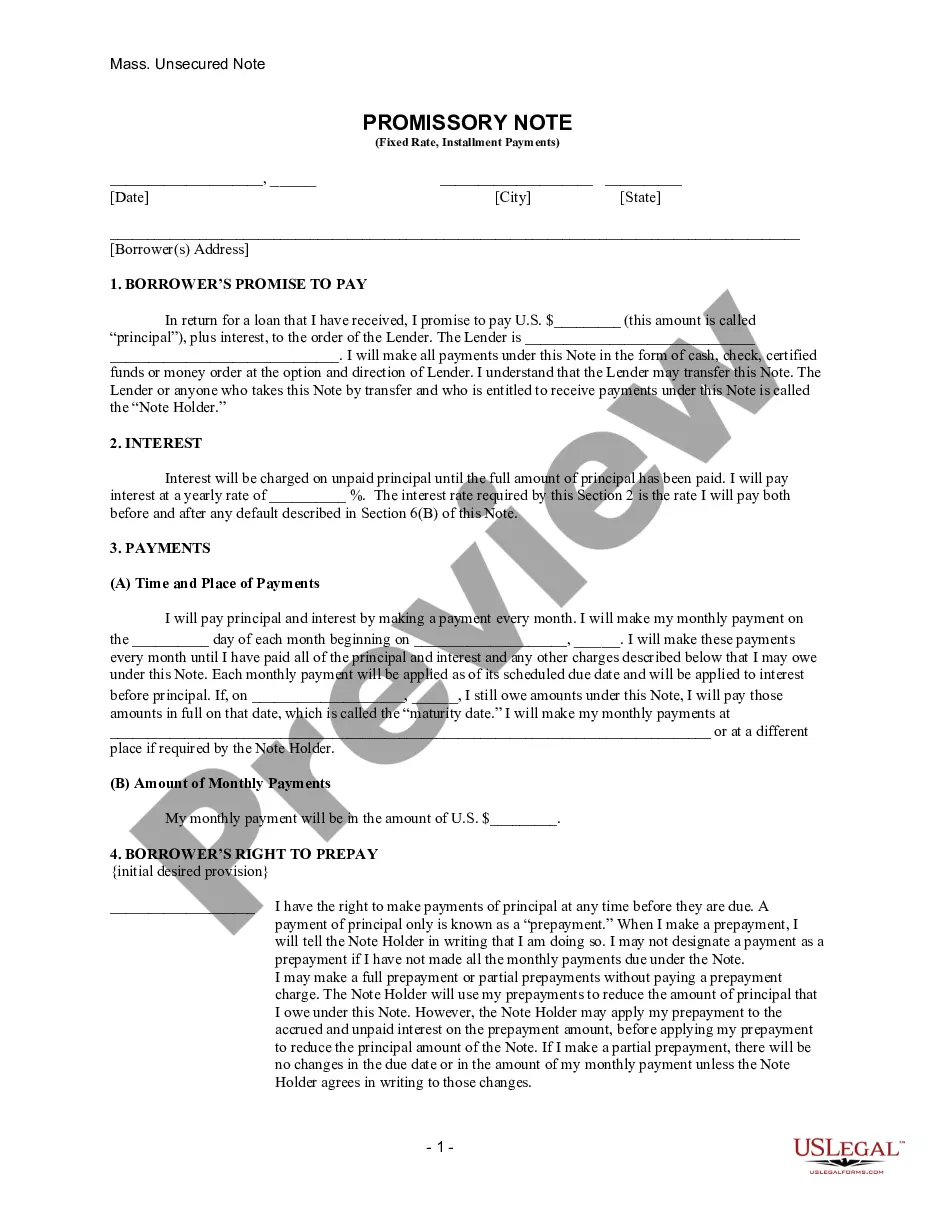

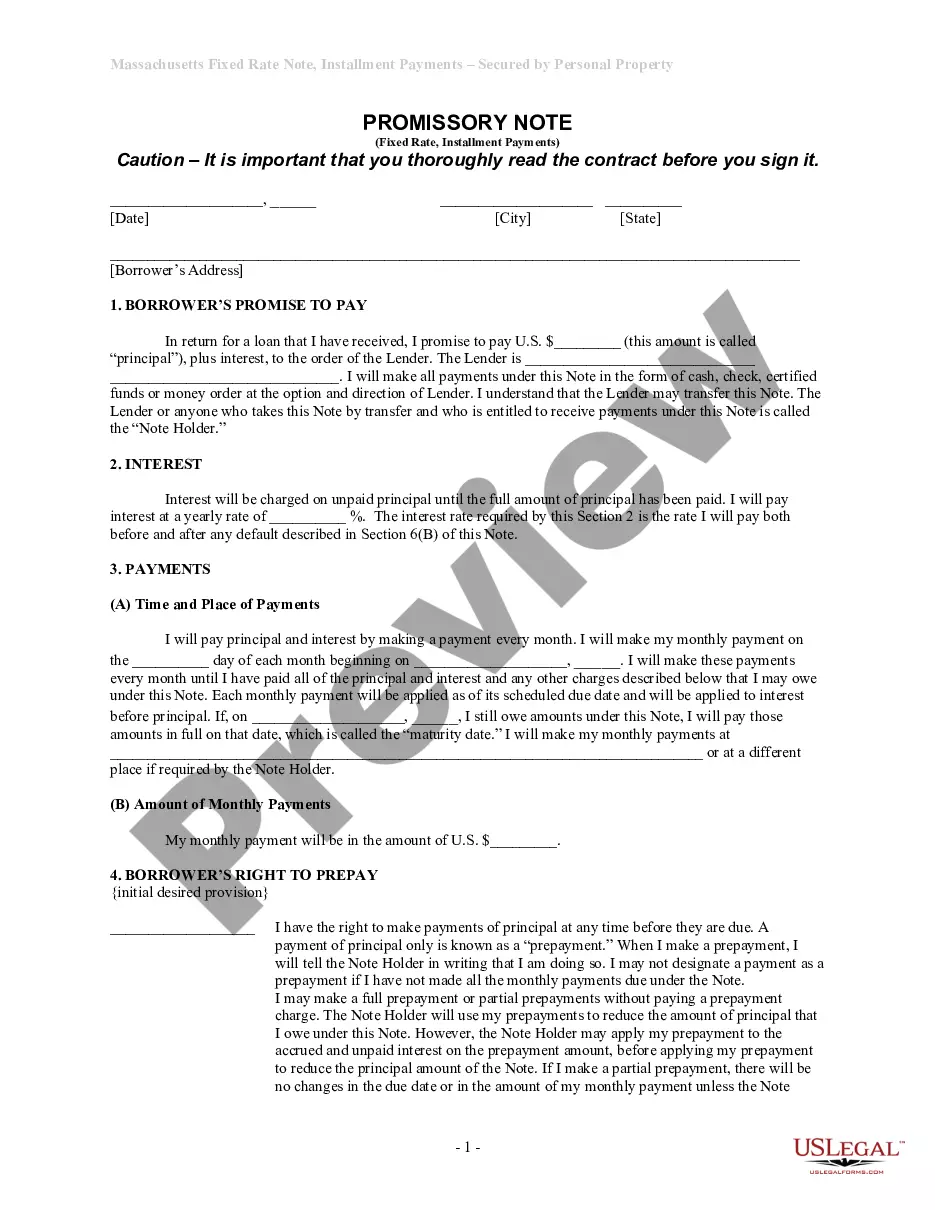

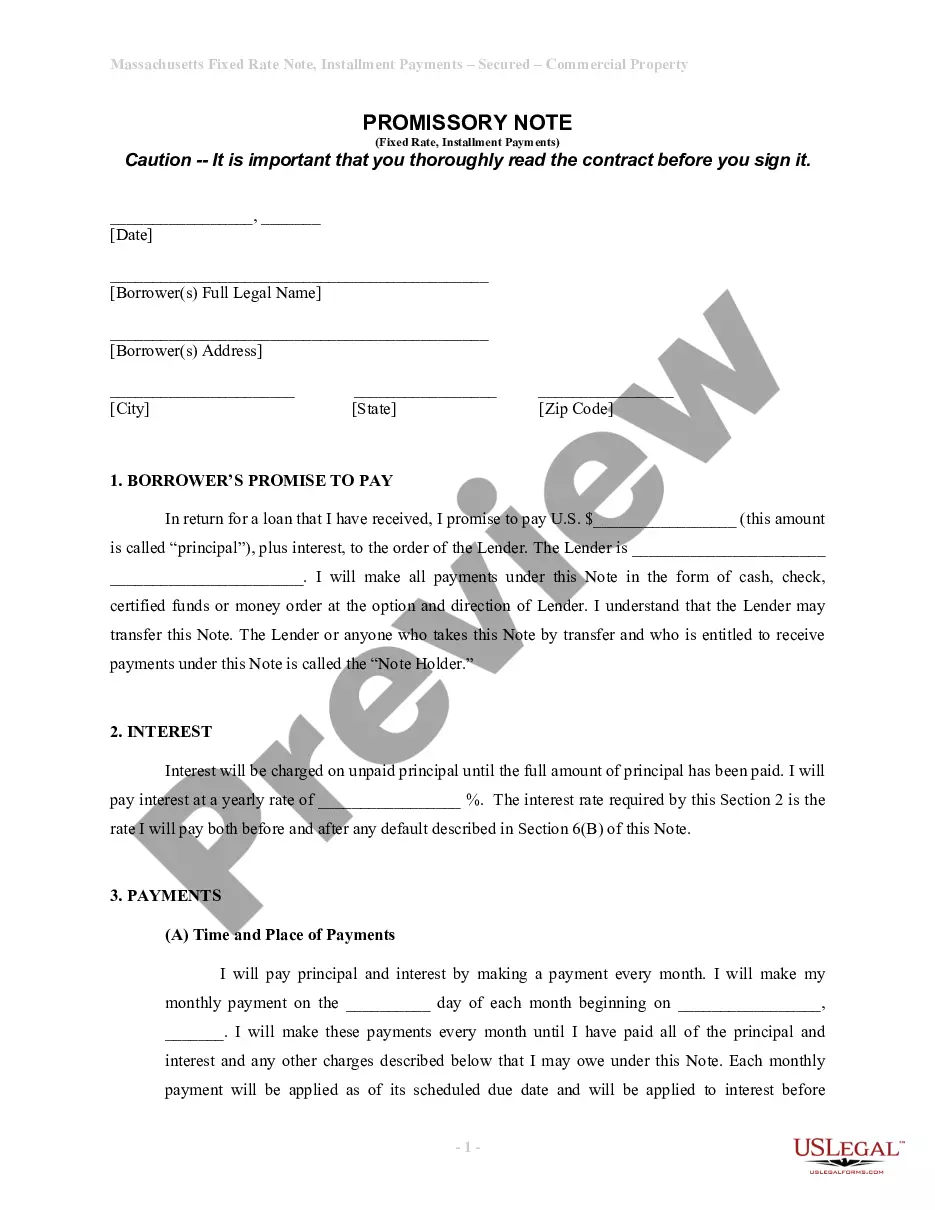

Massachusetts Installments Fixed Rate Promissory Note Secured by Residential Real Estate

Overview of this form

The Massachusetts Installments Fixed Rate Promissory Note Secured by Residential Real Estate is a legal document that outlines a borrower's promise to repay a loan secured by residential property. This form differs from other types of promissory notes because it includes specific terms for fixed-rate repayment and establishes the property as collateral for the loan, enhancing security for the lender. The use of this form is essential in situations where the borrower wishes to formalize a loan agreement with set repayment terms.

Main sections of this form

- Borrower's promise to pay, detailing the principal amount and interest rate.

- Payment schedule, including specific due dates for monthly installments.

- Provisions regarding the rights to prepay the loan and any associated penalties.

- Late payment fees and conditions regarding defaults.

- Notices and obligations outlined for communication between the borrower and lender.

- Secured provisions related to the mortgage or deed of trust that protect the lender's interests.

When to use this document

This form should be used when an individual or business is borrowing money and using residential real estate as collateral. Scenarios may include purchasing a home, refinancing a mortgage, or consolidating debts by taking out a loan with property security. The form is crucial when both the lender and borrower wish to have clearly defined payment terms and conditions to avoid disputes in the future.

Who should use this form

This form is suitable for the following users:

- Individuals or entities seeking a loan secured by residential property.

- Lenders looking to formalize loan agreements with borrowers.

- Homeowners refinancing their existing loans.

- Borrowers with multiple loans who want to consolidate through secured financing.

Steps to complete this form

- Identify the parties involved, including the borrower and lender.

- Specify the principal loan amount and the agreed-upon interest rate.

- Enter the payment schedule, including the start date and the due date for each monthly installment.

- Include any prepayment rights and fees, if applicable.

- Sign and date the form, ensuring all parties involved do so in the designated areas.

Does this document require notarization?

Notarization is required for this form to take effect. Our online notarization service, powered by Notarize, lets you verify and sign documents remotely through an encrypted video session, available 24/7.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Common mistakes

- Failing to properly specify the interest rate or payment terms.

- Not providing accurate identification for all parties involved.

- Overlooking the need for a separate mortgage or deed of trust document.

- Neglecting to date the document upon execution.

- Not reviewing state-specific requirements fully before completing the form.

Benefits of completing this form online

- The ability to access and download the form instantly, saving time.

- Easy customization to fit particular loan terms.

- Reliability and compliance with up-to-date legal standards.

- Clear, user-friendly interface that guides users through the process.

- Access to support and resources if questions arise during completion.

Looking for another form?

Form popularity

FAQ

"A promissory note is enforceable through an ordinary breach of contract claim." In other words, it's not required that the loan be secured; an unsecured loan is still enforceable as long as the promissory note is fully completed. Lender and borrower information.

Small businesses frequently borrow money, or extend credit, in the course of their operations. A promissory note is the document that sets forth the terms of a loan's repayment. A promissory note can be secured with a pledge of collateral, which is something of value that can be seized if a borrower defaults.

A promissory note is a contract, a binding agreement that someone will pay your business a sum of money. However under some circumstances if the note has been altered, it wasn't correctly written, or if you don't have the right to claim the debt then, the contract becomes null and void.

What Happens When a Promissory Note Is Not Paid? Promissory notes are legally binding documents. Someone who fails to repay a loan detailed in a promissory note can lose an asset that secures the loan, such as a home, or face other actions.

In order for a promissory note to be valid, both the lender and the borrower must sign the documentation. If you are a co-signer for the loan, you are required to sign the promissory note. Being a co-signer requires you to repay the loan amount in the instance that the borrower defaults on payment.

Promissory notes are legally binding whether the note is secured by collateral or based only on the promise of repayment. If you lend money to someone who defaults on a promissory note and does not repay, you can legally possess any property that individual promised as collateral.

Promissory notes are a valuable legal tool that any individual can use to legally bind another individual to an agreement for purchasing goods or borrowing money. A well-executed promissory note has the full effect of law behind it and is legally binding on both parties.

Writing the Promissory Note Terms You can use a template or create a promissory note online. But before you begin, you'll need to gather some information and make decisions about the way the loan will be structured. First, you'll need the names and addresses of both the lender (or "payee") and the borrower.