Guam Assignment of Life Insurance as Collateral

Description

How to fill out Assignment Of Life Insurance As Collateral?

You are able to devote hours on the Internet searching for the legitimate document web template which fits the state and federal specifications you will need. US Legal Forms supplies a huge number of legitimate forms which are evaluated by professionals. It is simple to acquire or print the Guam Assignment of Life Insurance as Collateral from my support.

If you already have a US Legal Forms account, it is possible to log in and click the Obtain key. After that, it is possible to full, modify, print, or sign the Guam Assignment of Life Insurance as Collateral. Each legitimate document web template you get is the one you have for a long time. To get yet another backup of the bought type, proceed to the My Forms tab and click the related key.

If you work with the US Legal Forms internet site for the first time, follow the easy directions below:

- Initial, ensure that you have selected the proper document web template to the region/metropolis of your choice. Browse the type explanation to make sure you have picked the right type. If readily available, take advantage of the Review key to look throughout the document web template at the same time.

- If you wish to find yet another version from the type, take advantage of the Look for field to find the web template that meets your requirements and specifications.

- After you have identified the web template you would like, just click Buy now to carry on.

- Find the prices program you would like, key in your accreditations, and register for a free account on US Legal Forms.

- Full the financial transaction. You should use your charge card or PayPal account to purchase the legitimate type.

- Find the file format from the document and acquire it for your gadget.

- Make alterations for your document if needed. You are able to full, modify and sign and print Guam Assignment of Life Insurance as Collateral.

Obtain and print a huge number of document web templates while using US Legal Forms site, that offers the largest selection of legitimate forms. Use expert and condition-distinct web templates to deal with your organization or personal requirements.

Form popularity

FAQ

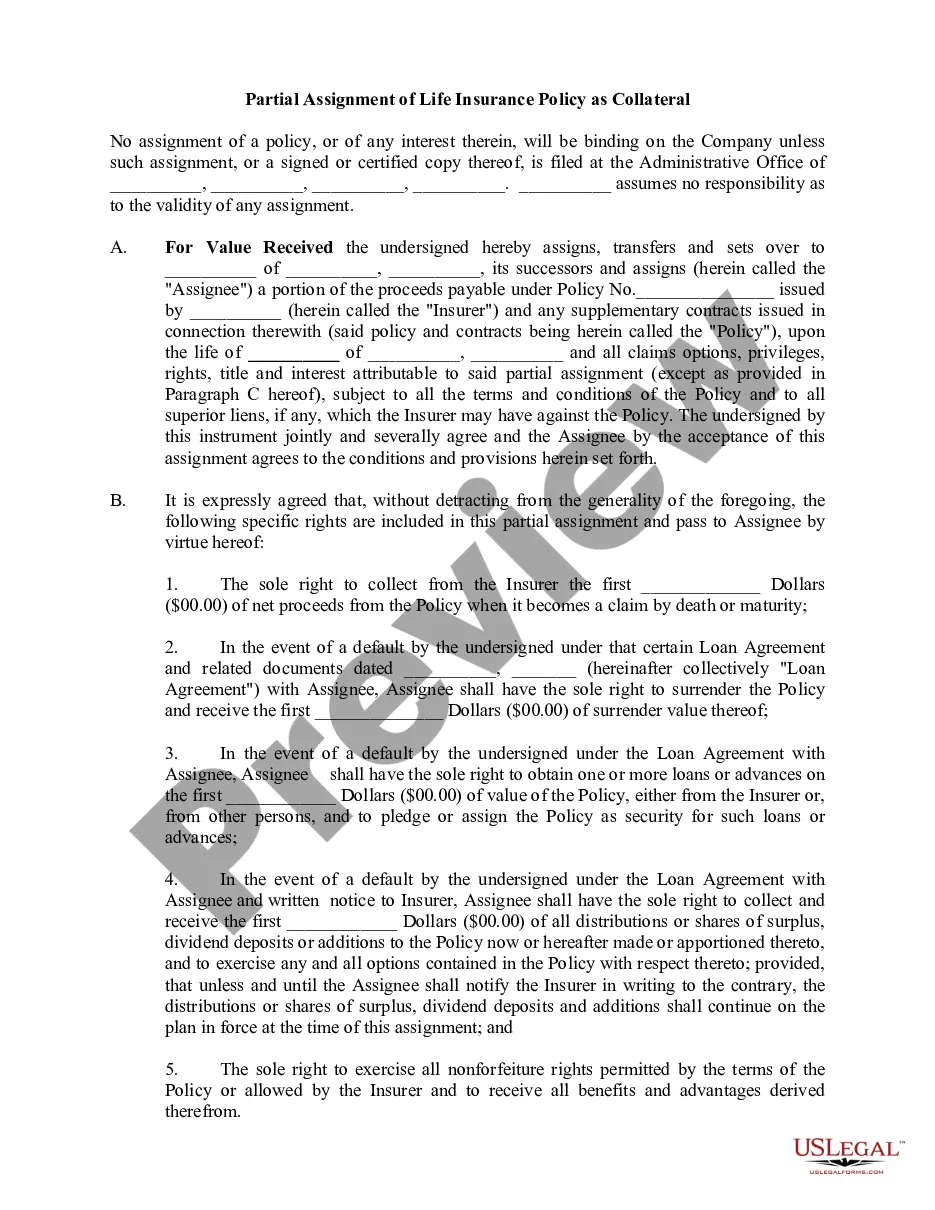

Which of these actions is taken when a policyowner uses a Life Insurance policy as collateral for a bank loan? Collateral assignment" A policyowner using the Life Insurance policy as collateral for a bank loan normally would make a collateral assignment.

The collateral assignment is irrevocable as established by a written agreement preventing the holder of the life insurance policy from affecting or using the cash surrender value after the irrevocable assignment.

Collateral assignment of life insurance is a method of providing a lender with collateral when you apply for a loan. In this case, the collateral is your life insurance policy's face value, which could be used to pay back the amount you owe in case you die while in debt.

The irrevocable assignment includes: Irrevocably assigns and transfers all the benefits and proceeds of the life insurance policy to the funeral home/funeral director. The cash value is not counted as an available asset. The life insurance cannot be canceled.

You can use either term or whole life insurance policy as collateral, but the death benefit must meet the lender's terms. Alternately, the policy owner's access to the cash value is restricted to protect the collateral.

Unless instructed differently, your life insurance company creates a revocable beneficiary designation when you purchase the policy. If you want to assign an irrevocable beneficiary, let your insurance company know. You may be able to update an existing life insurance policy to include an irrevocable beneficiary.

A collateral assignment supersedes your beneficiaries' rights to the death benefit. If you die, the life insurance company pays the lender, or assignee, the loan balance. As noted earlier, any remaining benefit goes to your beneficiaries.

If you have a life insurance policy, you're in luck, because most businesses typically accept life insurance as collateral as they can guarantee funds if the borrower dies or defaults.