Connecticut Terms for Private Placement of Series Seed Preferred Stock

Description

How to fill out Terms For Private Placement Of Series Seed Preferred Stock?

You are able to invest hours on-line searching for the legal record format that meets the state and federal needs you want. US Legal Forms provides a huge number of legal types which are examined by pros. It is simple to acquire or print out the Connecticut Terms for Private Placement of Series Seed Preferred Stock from your support.

If you already have a US Legal Forms accounts, it is possible to log in and click on the Obtain option. After that, it is possible to full, modify, print out, or indicator the Connecticut Terms for Private Placement of Series Seed Preferred Stock. Each and every legal record format you get is your own property for a long time. To acquire an additional copy of any obtained develop, check out the My Forms tab and click on the corresponding option.

If you work with the US Legal Forms internet site the first time, follow the easy guidelines under:

- Initially, be sure that you have chosen the proper record format to the state/metropolis of your choosing. See the develop information to make sure you have picked the appropriate develop. If accessible, use the Review option to search through the record format too.

- If you want to locate an additional version of your develop, use the Research area to discover the format that fits your needs and needs.

- When you have discovered the format you desire, click Buy now to continue.

- Find the prices plan you desire, key in your qualifications, and sign up for an account on US Legal Forms.

- Comprehensive the purchase. You should use your credit card or PayPal accounts to purchase the legal develop.

- Find the format of your record and acquire it to your product.

- Make alterations to your record if required. You are able to full, modify and indicator and print out Connecticut Terms for Private Placement of Series Seed Preferred Stock.

Obtain and print out a huge number of record templates using the US Legal Forms website, which provides the most important collection of legal types. Use professional and condition-particular templates to deal with your business or personal demands.

Form popularity

FAQ

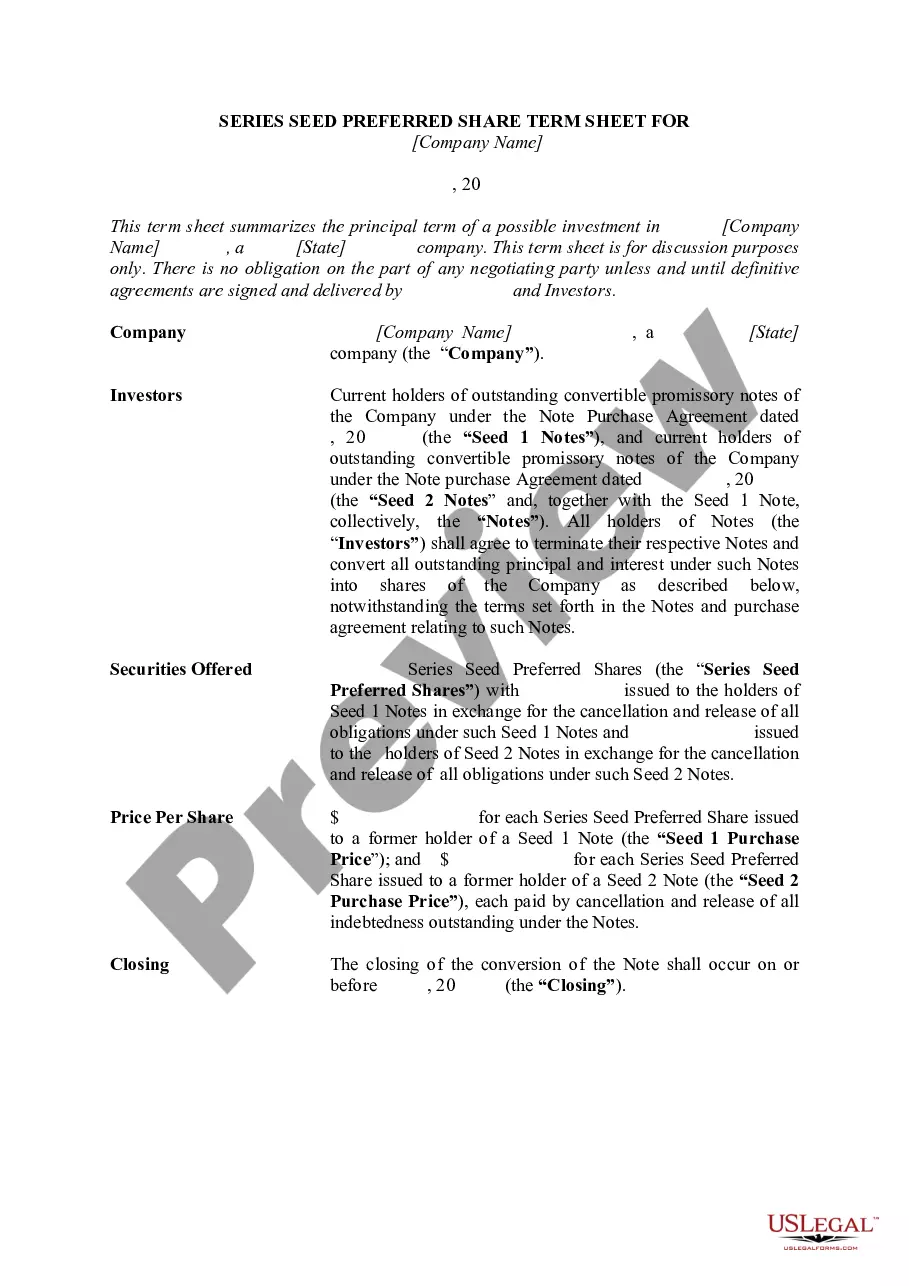

But no matter who the investor is, a term sheet will always contain six key components, including: A valuation. An estimate of what a company is worth as an investment opportunity. ... Securities being issued. ... Board rights. ... Investor protections. ... Dealing with shares. ... Miscellaneous provisions. The 6 key components of a term sheet - Espresso Capital espressocapital.com ? resources ? blog ? term-she... espressocapital.com ? resources ? blog ? term-she...

Key Takeaways The company valuation, investment amount, percentage stake, voting rights, liquidation preference, anti-dilutive provisions, and investor commitment are some items that should be spelled out in the term sheet. Term Sheets: Definition, What's Included, Examples, and Key ... Investopedia ? ... ? Investing Basics Investopedia ? ... ? Investing Basics

The valuation is one of the most important elements of a term sheet and distinguishes it from similar documents, such as SAFEs, which are used in earlier funding rounds when your company's valuation is not yet known. Term Sheets for Startups: Uses & Examples - Carta Carta ? blog ? term-sheets Carta ? blog ? term-sheets

The key clauses of a term sheet can be grouped into four categories; deal economics, investor rights and protection, governance management and control, and exits and liquidity. The Ultimate Term Sheet Guide - all terms and clauses ... Salesflare Blog ? term-sheet-guide Salesflare Blog ? term-sheet-guide

Key provisions of a VC term sheet include: investment structure, key economic terms, shareholder agreements, due diligence, exclusivity and closing. Institutional venture capital (VC) term sheets | Securing investment marsdd.com ? article ? securing-investment-i... marsdd.com ? article ? securing-investment-i...

How to Prepare a Term Sheet Identify the Purpose of the Term Sheet Agreements. Briefly Summarize the Terms and Conditions. List the Offering Terms. Include Dividends, Liquidation Preference, and Provisions. Identify the Participation Rights. Create a Board of Directors. End with the Voting Agreement and Other Matters. How to Prepare a Term Sheet: A Step-By-Step Guide westchesterangels.com ? how-to-prepare-a-term-s... westchesterangels.com ? how-to-prepare-a-term-s...

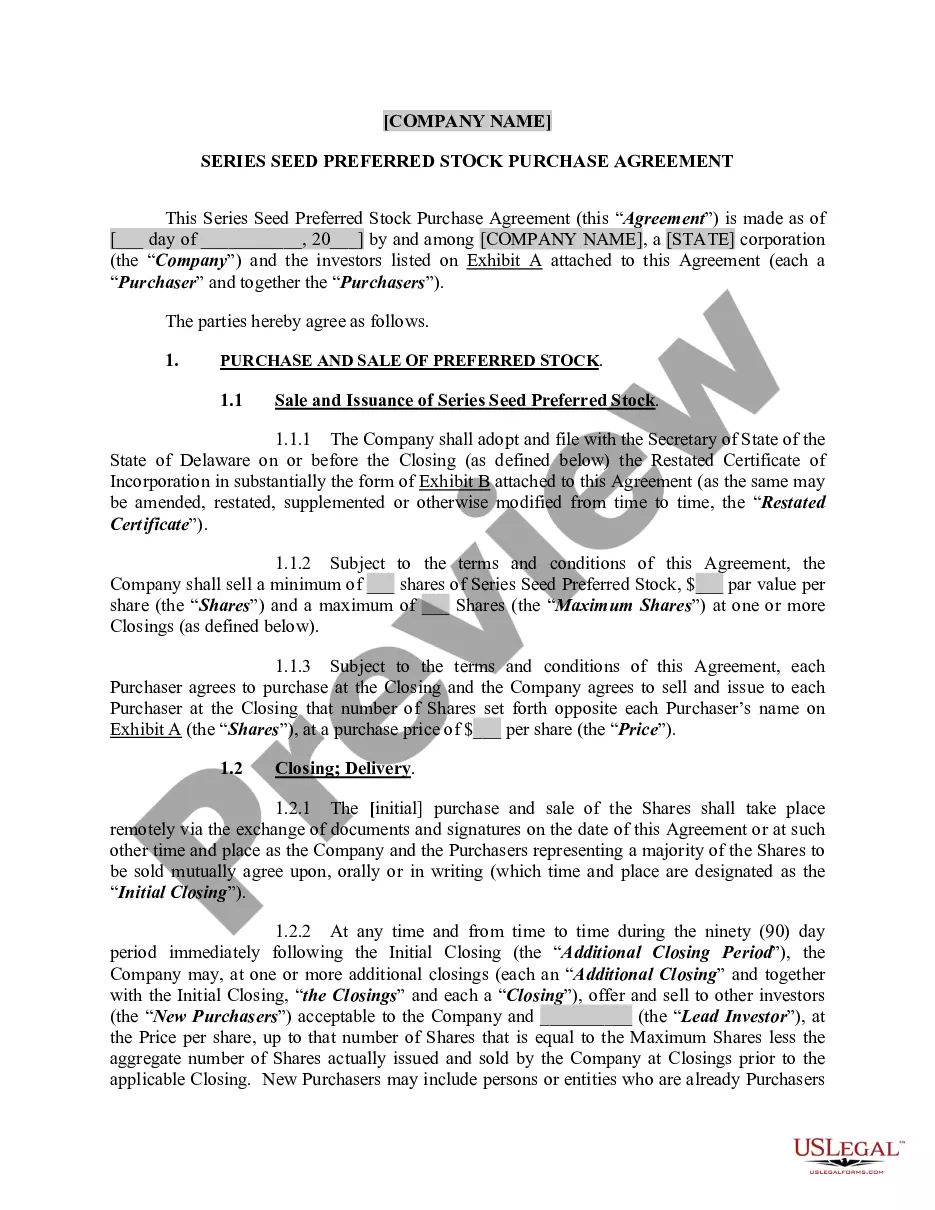

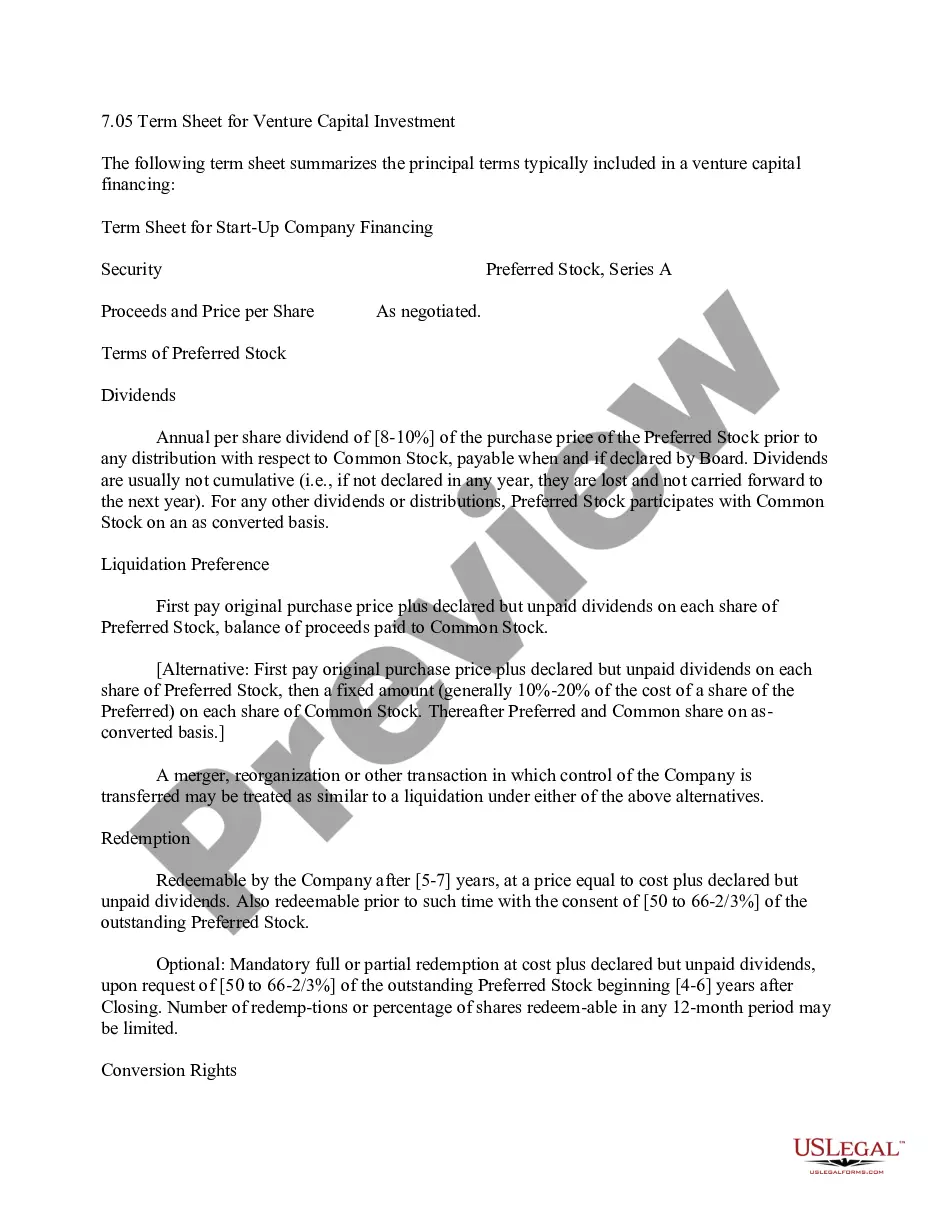

Series Seed Preferred Stock is a type of preferred stock issued by startups during their early stage of development. Preferred stock is a hybrid security that combines elements of both debt and equity. What Is Series Seed Preferred Stock? | Wojcik Law Firm Wojcik Law Firm ? what-is-series-seed-... Wojcik Law Firm ? what-is-series-seed-...

While drafting a term sheet, a few things should be kept in mind like, keeping it simple and clear, knowing your audience, defining the key terms of the agreement, having a scope for flexibility, having set timelines, defining confidentiality and exclusivity clauses, and addressing potential contingencies. 7 Tips for Writing a Term Sheet and Its Importance - BimaKavach bimakavach.com ? blog ? 7-tips-for-writing... bimakavach.com ? blog ? 7-tips-for-writing...