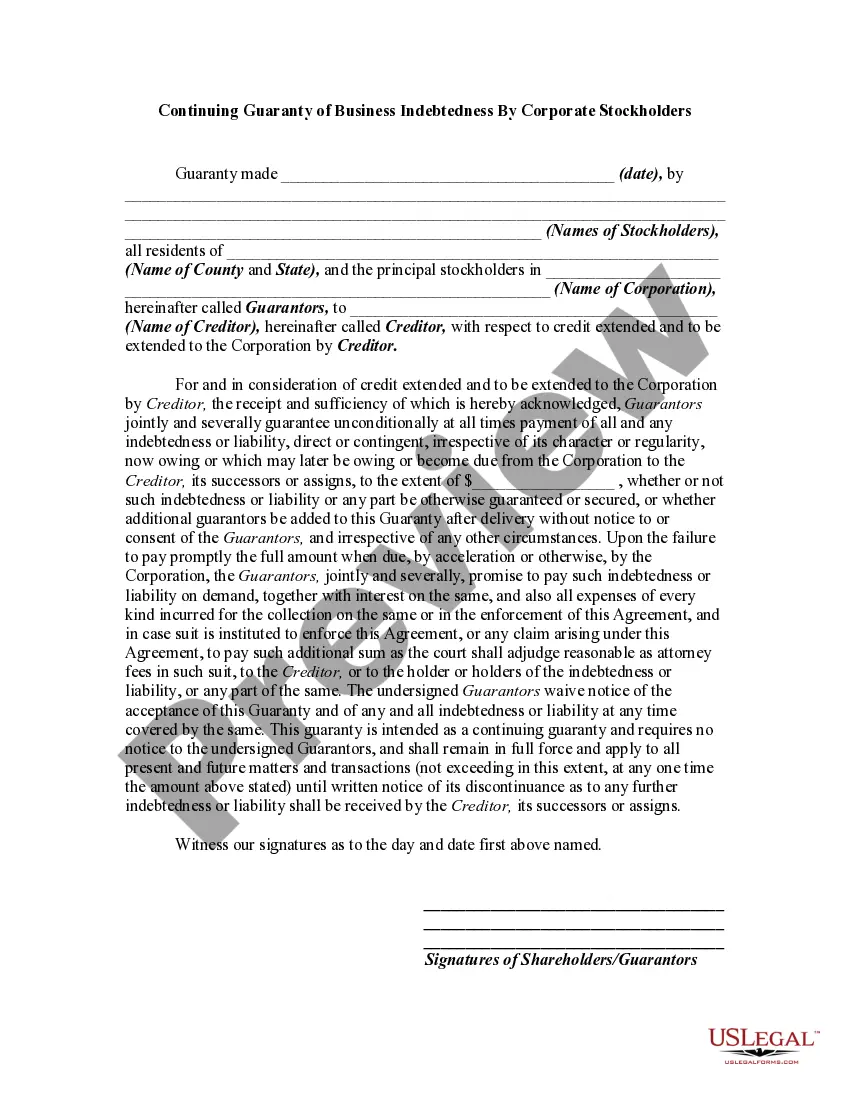

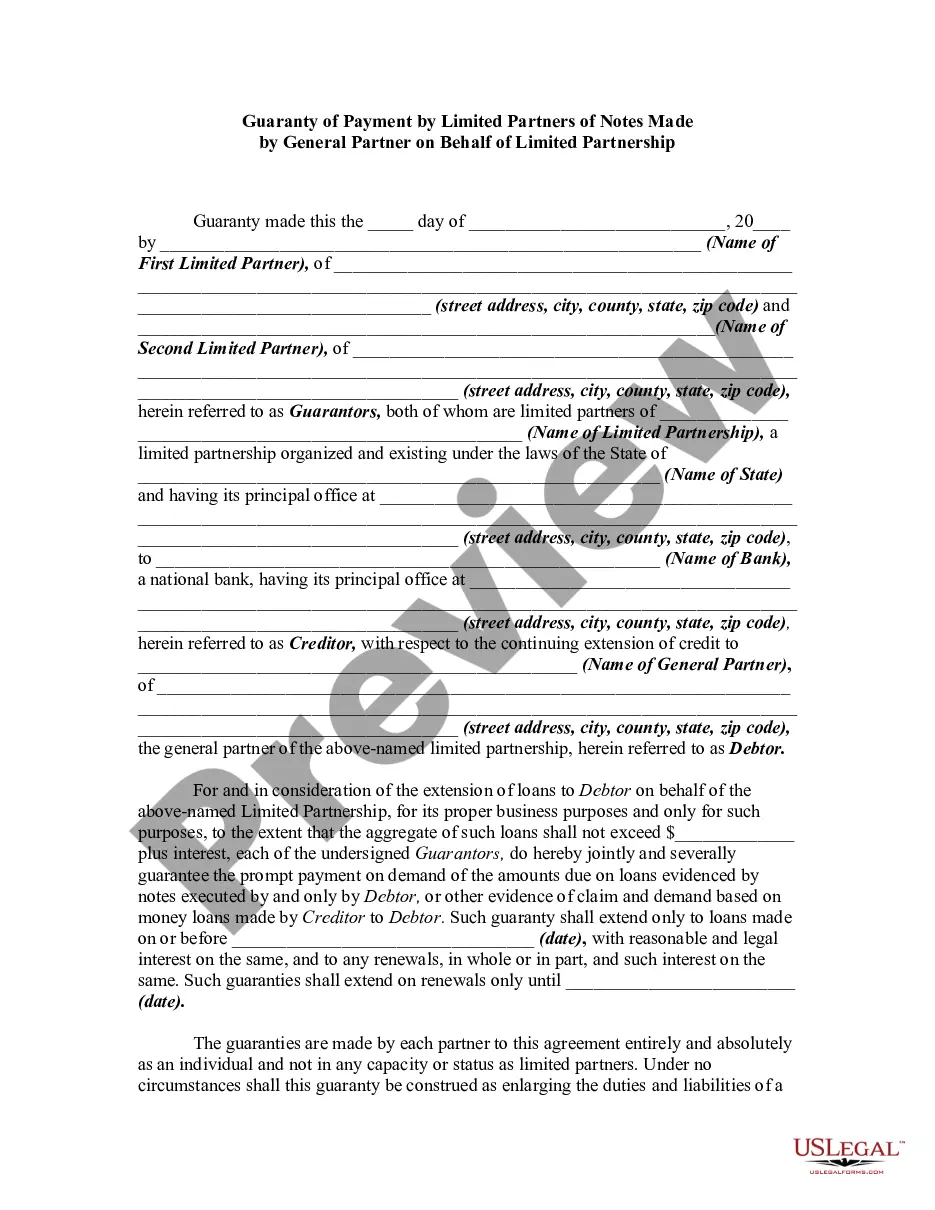

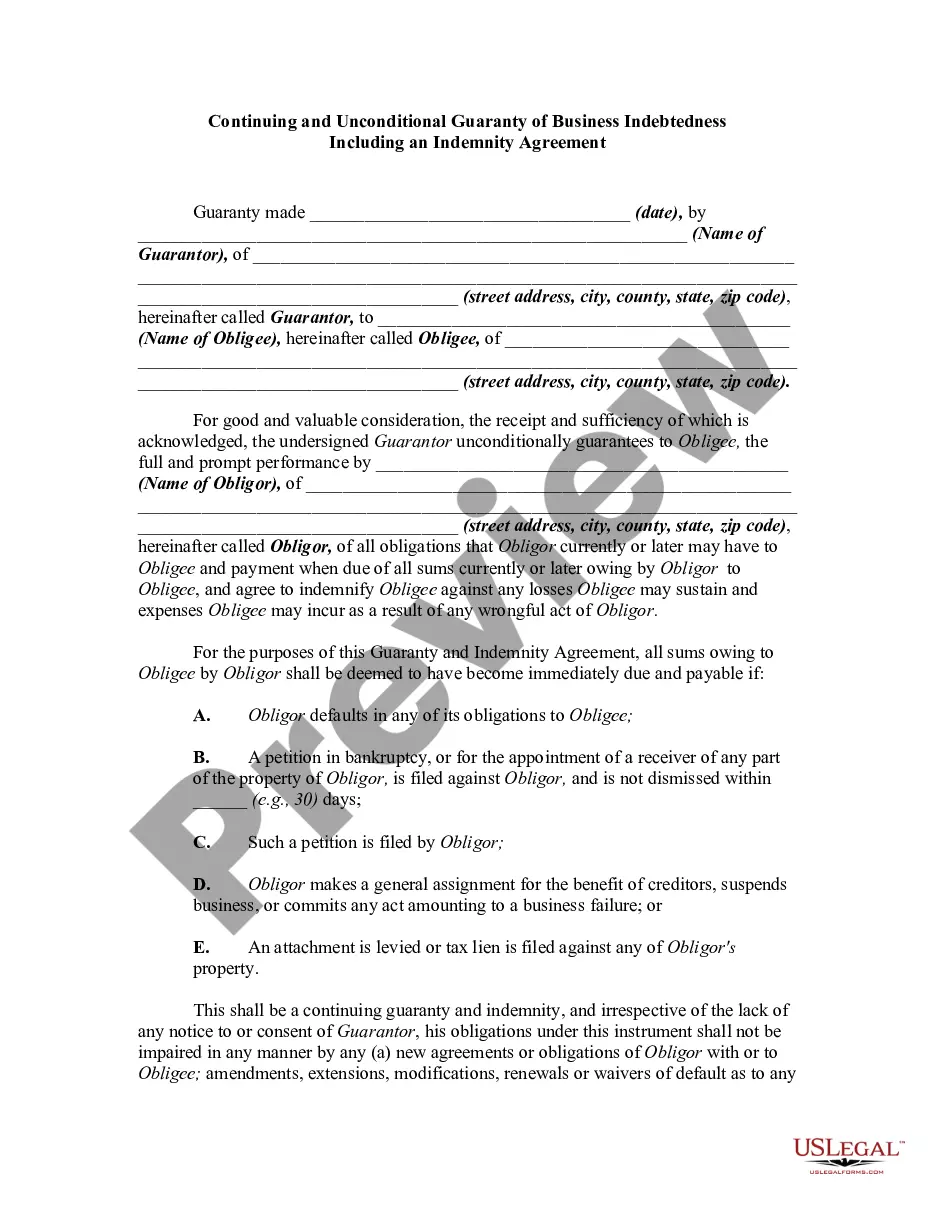

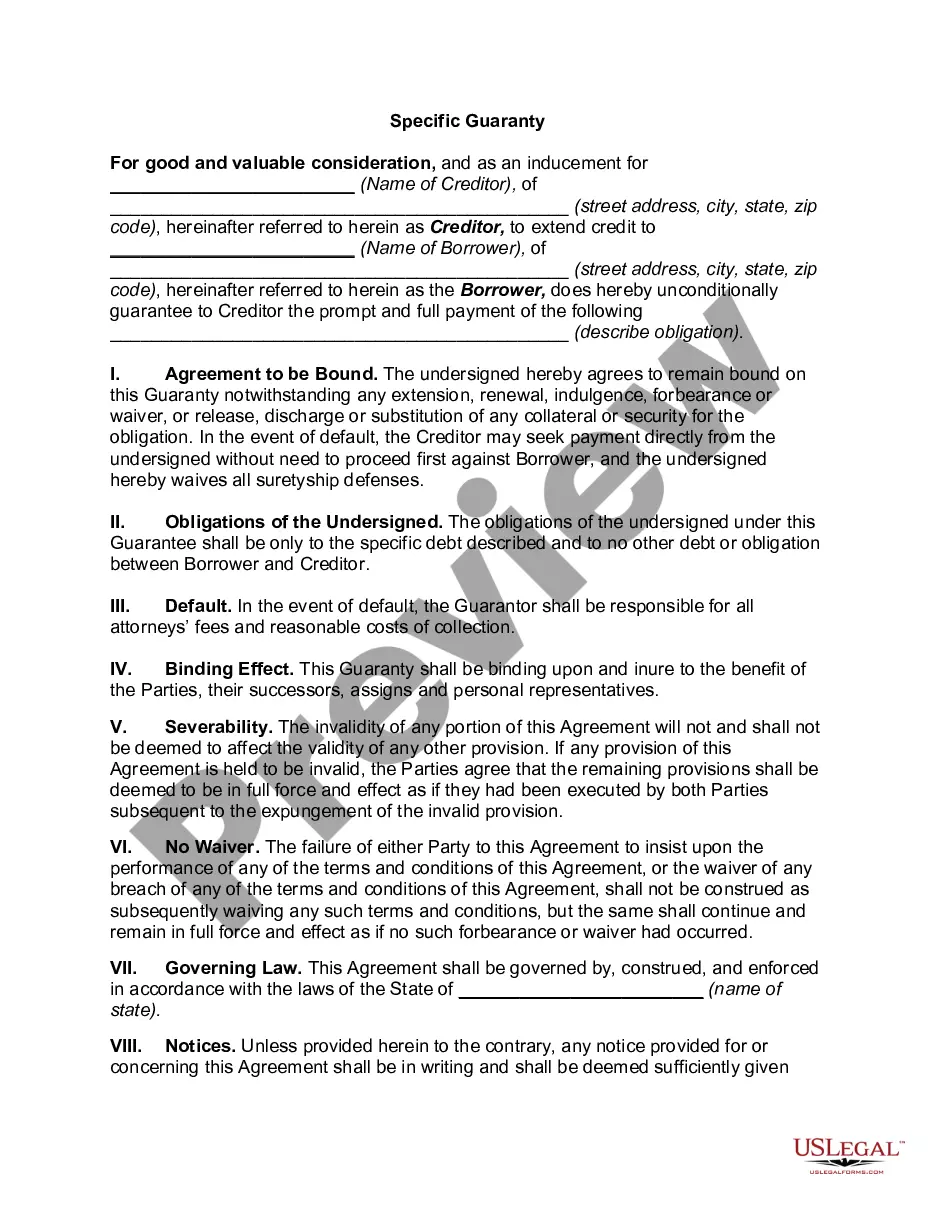

A guaranty is an undertaking on the part of one person (the guarantor) that is collateral to an obligation of another person (the debtor or obligor), and which binds the guarantor to performance of the obligation in the event of default by the debtor or obligor. A guaranty agreement is a type of contract. Thus, questions relating to such matters as validity, interpretation, and enforceability of guaranty agreements are decided in accordance with basic principles of contract law.

Colorado Continuing Guaranty of Business Indebtedness with Guarantor Having Limited Liability

Category:

State:

Multi-State

Control #:

US-01116BG

Format:

Word;

Rich Text

Instant download

Description

Free preview

How to fill out Continuing Guaranty Of Business Indebtedness With Guarantor Having Limited Liability?

Are you in a situation where you require documents for either business or personal purposes on a daily basis.

There are many legal document templates available online, but finding ones you can trust can be challenging.

US Legal Forms provides thousands of form templates, including the Colorado Continuing Guaranty of Business Indebtedness with Guarantor Having Limited Liability, which can be customized to comply with state and federal regulations.

Utilize US Legal Forms, the most comprehensive selection of legal templates, to save time and avoid mistakes.

The service offers professionally crafted legal document templates that you can use for various purposes. Create an account on US Legal Forms and start making your life a bit easier.

- If you are already familiar with the US Legal Forms website and have an account, simply Log In.

- Afterward, you can download the Colorado Continuing Guaranty of Business Indebtedness with Guarantor Having Limited Liability template.

- If you do not have an account and want to begin using US Legal Forms, follow these steps.

- Find the form you need and ensure it is for the correct city/region.

- Utilize the Review option to examine the form.

- Read the description to confirm you have selected the correct form.

- If the form isn’t what you’re looking for, use the Lookup field to find the form that suits your needs and requirements.

- Once you find the correct form, click on Purchase now.

- Choose the pricing plan you desire, fill in the required information to create your account, and complete your order using your PayPal or credit card.

- Select a convenient file format and download your copy.

- You can find all the document templates you have bought in the My documents list. You can download an additional copy of the Colorado Continuing Guaranty of Business Indebtedness with Guarantor Having Limited Liability at any time by clicking on the required form to download or print the document template.

Form popularity

FAQ

Personal guarantees often contain loopholes that can protect the guarantor from excessive liability. For instance, if the agreement lacks clear language regarding the extent of liability, you might argue for limited responsibility. Additionally, some state laws, such as those relevant to a Colorado Continuing Guaranty of Business Indebtedness with Guarantor Having Limited Liability, may provide protections. To navigate these complexities effectively, using platforms like USLegalForms can guide you in understanding your rights and obligations.

Being a guarantor means you agree to take on the responsibility for a debt or obligation if the primary borrower fails to make payments. In the context of a Colorado Continuing Guaranty of Business Indebtedness with Guarantor Having Limited Liability, this liability can be limited, meaning you may not have to cover the entire debt. It's crucial to understand the terms of your guaranty, as this agreement can influence your financial stability. Consulting resources on USLegalForms can help clarify these obligations.

A limited guarantor is a party that agrees to cover a borrower’s debt but only up to a specified amount or under stipulated conditions. This concept is often tied to the Colorado Continuing Guaranty of Business Indebtedness with Guarantor Having Limited Liability, where the guarantor's risk is mitigated. Understanding the role and limits of a limited guarantor can help individuals make informed decisions in business dealings.

The three main types of guarantees are absolute guarantees, limited guarantees, and performance guarantees. An absolute guarantee offers total liability coverage, while a limited guarantee restricts the extent of this liability, a concept often seen in a Colorado Continuing Guaranty of Business Indebtedness with Guarantor Having Limited Liability. Performance guarantees ensure that specific contractual obligations are fulfilled, providing varied options to suit different financial situations.

Yes, an LLC can serve as a guarantor in various financial transactions. When a Colorado Continuing Guaranty of Business Indebtedness with Guarantor Having Limited Liability is involved, the legal structure of the LLC can limit personal liability for its owners. It's essential to understand the implications of this arrangement, especially in terms of risk management and financial commitment.

A guarantee provides unconditional protection to a lender, ensuring payment on a debt if the borrower defaults. In contrast, a limited guarantee, typically associated with a Colorado Continuing Guaranty of Business Indebtedness with Guarantor Having Limited Liability, restricts the amount or extent of liability. This distinction is crucial for those navigating financial agreements, especially when considering the responsibilities of a guarantor.

A personal guarantor offers a personal asset guarantee, while a corporate guarantor represents a business entity backing the obligation. This difference impacts liability and how claims can be pursued in case of default. In the context of the Colorado Continuing Guaranty of Business Indebtedness with Guarantor Having Limited Liability, understanding these distinctions can help businesses select the right type of guarantor for their financial agreements.

Guarantors can protect themselves by thoroughly understanding the terms of the guarantee and limiting their liability. Under the Colorado Continuing Guaranty of Business Indebtedness with Guarantor Having Limited Liability, this can be achieved through negotiating terms that specify limits to the guarantee. Furthermore, professional guidance and legal advice can provide critical insights into safeguarding against potential risks.

The primary difference between a guarantor and a limited guarantor is the extent of liability. A guarantor assumes full responsibility for the debt, while a limited guarantor's liability is capped or restricted by specific terms. This distinction is crucial in the Colorado Continuing Guaranty of Business Indebtedness, as a limited guarantor may protect personal or business assets by outlining their obligations clearly.

In general, there are several types of guarantors, including personal guarantors, corporate guarantors, and limited guarantors. Personal guarantors are individuals, while corporate guarantors are businesses or organizations that provide a guarantee. Limited guarantors, as part of the Colorado Continuing Guaranty of Business Indebtedness with Guarantor Having Limited Liability, have restrictions on their liability, providing some protection for their personal or corporate assets.