Alaska General Partnership Package

What is this form package?

The Alaska General Partnership Package provides a comprehensive set of legal forms designed to assist with the formation, management, and dissolution of a partnership in Alaska. This package includes customizable templates drafted by licensed attorneys, making it a reliable resource for business partners to establish terms that best fit their unique circumstances. Unlike other packages, this one covers various aspects of partnership life cycles, ensuring partners have the necessary documentation throughout their journey.

What’s included in this form package

- Agreement for the Dissolution of a Partnership

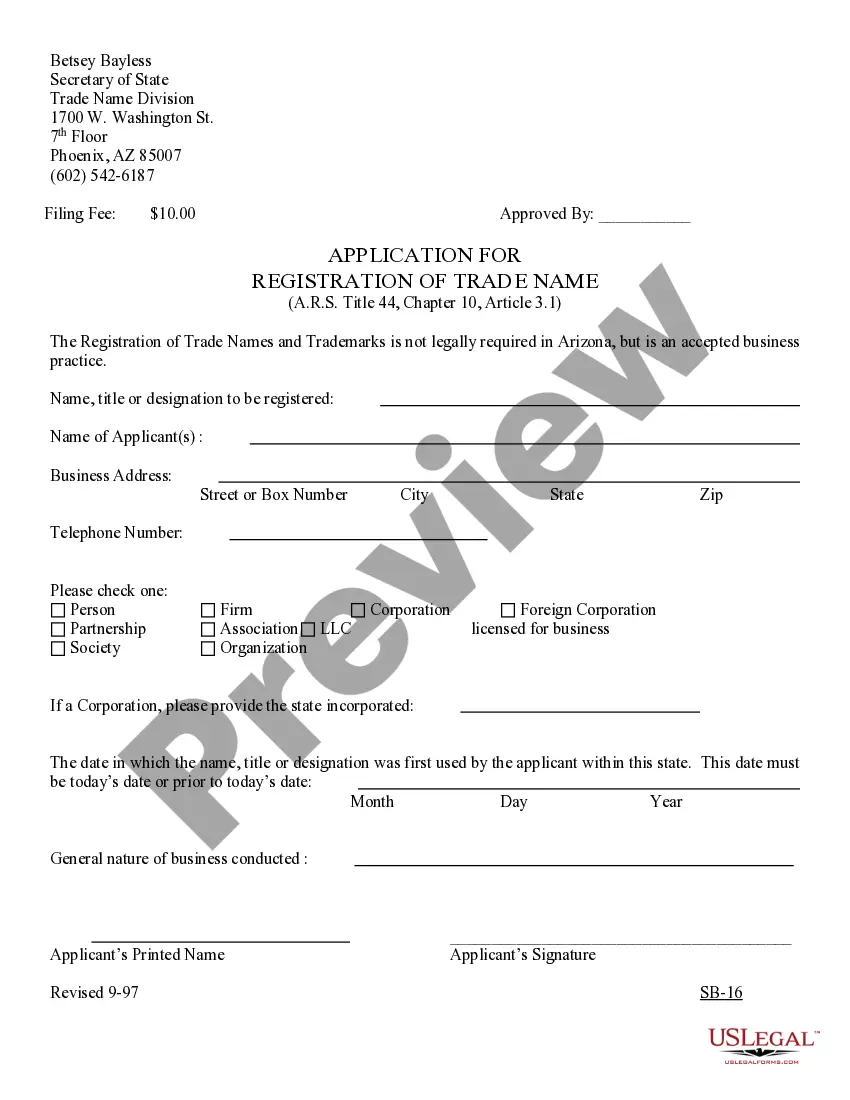

- Business Name Registration Application

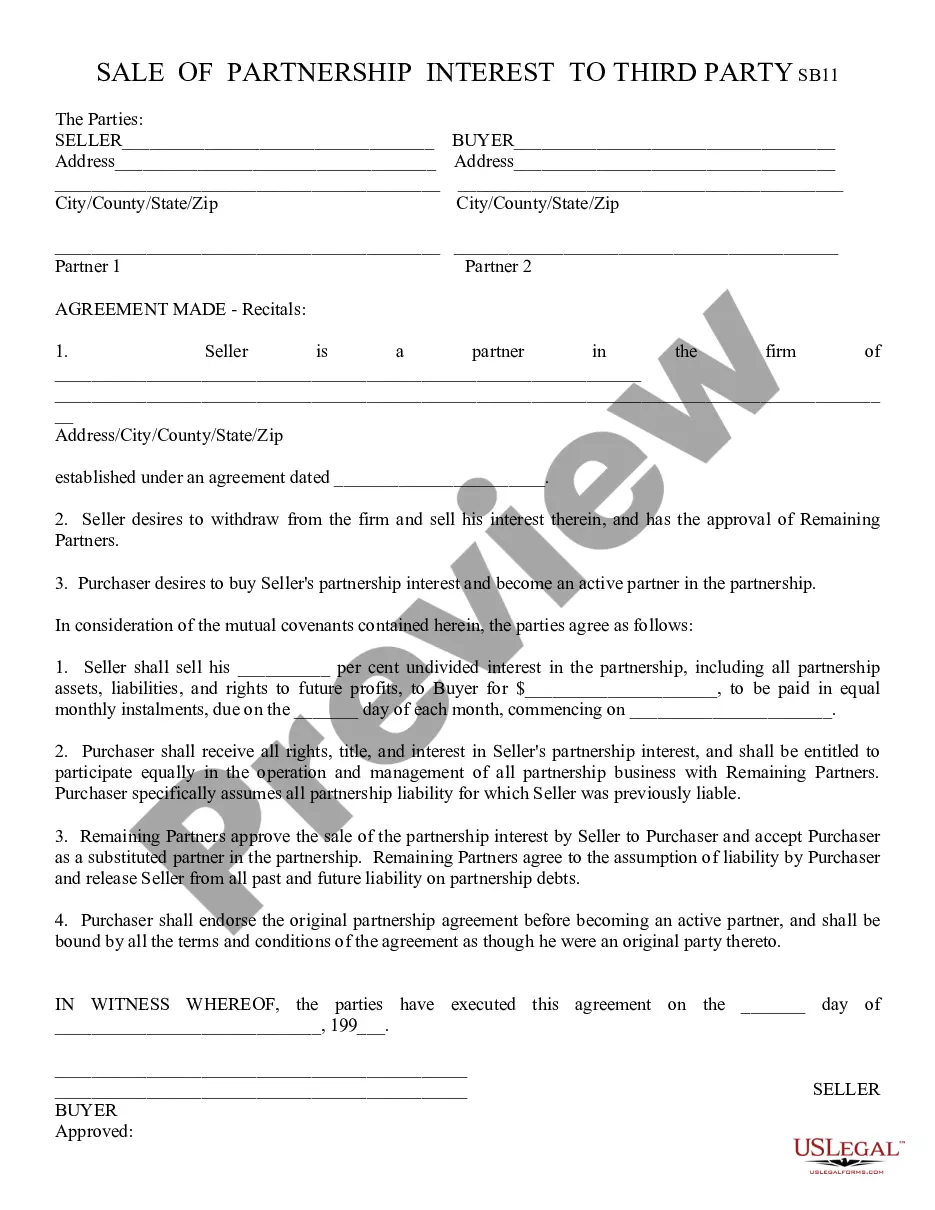

- Buy Sell Agreement Between Partners of a Partnership

- I.R.S. Form SS-4 (to obtain your federal identification number)

- Sample Business Plan Template

- Simple Partnership Agreement

- Checklist for Starting Up a New Business

- General Partnership Agreement - Complex

- Profit and Loss Statement

- Business Startup Costs

- Employment or Work Application - General

- Stand Alone Confidentiality and Noncompetition Agreement with Employee

- Self-Employed Independent Contractor Employment Agreement - General

Situations where these forms applies

This form package is beneficial in several scenarios, including:

- When starting a new general partnership and needing a formal partnership agreement.

- When existing partners want to establish a buy-sell agreement to manage potential changes in partnership.

- When recording the financial health of a partnership with a profit and loss statement.

- When partners decide to dissolve the partnership and require a formal agreement to finalize the process.

Who should use this form package

- Business owners who are planning to establish a new partnership in Alaska.

- Existing partners who wish to clarify terms and strengthen their business relationship.

- Partners looking to formalize the processes for financial reporting and asset division.

- Anyone involved in a partnership looking to dissolve or restructure their business arrangement.

How to prepare this document

- Review the included forms to identify which documents apply to your situation.

- Gather required information, such as partner details and the agreed terms of the partnership.

- Fill out the partnership agreement, ensuring all relevant sections are completed accurately.

- Complete the profit and loss statement with financial data pertinent to your partnership.

- Have all partners review the completed documents before signatures are obtained.

- Store the signed documents securely for future reference, ensuring compliance with all relevant regulations.

Notarization guidance for this package

Forms in this package typically do not require notarization unless required by local law. However, it is advisable to consult local regulations for any specific notarization requirements that may apply to partnership documents in Alaska.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Common mistakes

- Failing to define the roles and responsibilities of each partner clearly.

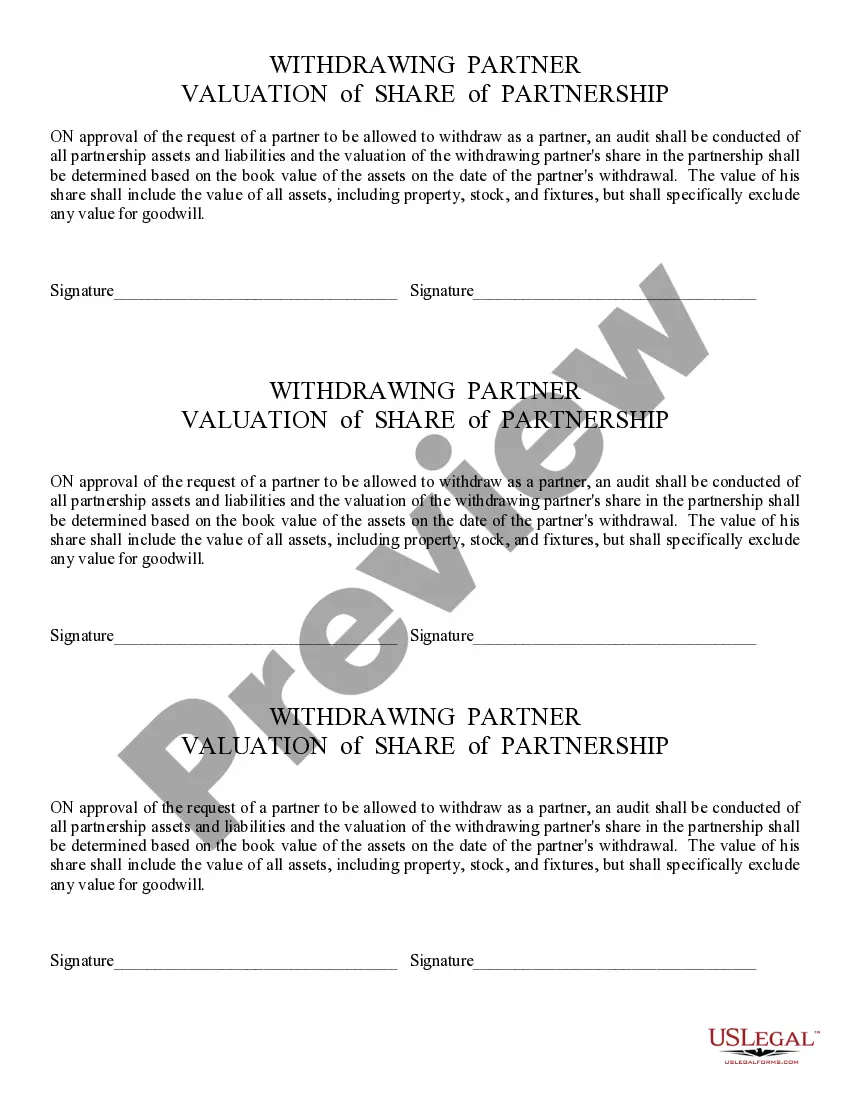

- Not addressing what happens in cases of partner withdrawal or death.

- Neglecting to update partnership agreements when circumstances change.

- Inaccurately reporting financial data in the profit and loss statement.

Why use this package online

- Convenience of downloading and accessing forms from anywhere.

- Editability allows for customization to meet specific partnership needs.

- Reliability, with forms developed by licensed attorneys to ensure compliance with legal standards.

Legal use & context

- These documents are enforceable in accordance with Alaska partnership laws.

- Properly completed forms outline responsibilities and protect the rights of partners involved.

- Dissolution agreements prevent future disputes by establishing clear terms for winding up partnership affairs.

Key takeaways

- The Alaska General Partnership Package includes essential forms for partnership formation, management, and dissolution.

- Using this package can help prevent common mistakes and ensure compliance with state laws.

- Customization of the forms allows flexibility to meet specific partnership needs.

- This package offers a cost-effective solution, saving up to 40% compared to purchasing individual forms.

Looking for another form?

Form popularity

FAQ

They both offer "pass-through" taxation, which means that the owners report business income or losses on their individual tax returns; the partnership or LLC itself does not pay taxes. And both are eligible for the 20% pass-through deduction established by the Tax Cuts and Jobs Act.

A limited liability company (LLC) is a popular choice among small business owners for the liability protection, management flexibility, and tax advantages this form of business entity often provides.

Advantage: Easy to Create. Disadvantage: Easy to Dissolve. Advantage: Flow of Personal Income. Disadvantage: Little Protection. Advantage: Flexibility. Disadvantages: Lack of Structure.

LLCs protect owners against personal liability for business debts and lawsuits. This safeguards the personal assets for all owners. In a general partnership, owners have unlimited, personal liability for the businesses' debts, including, but not limited to, the acts of employees.

Aside from formation requirements, the main difference between a partnership and an LLC is that partners are personally liable for any business debts of the partnership -- meaning that creditors of the partnership can go after the partners' personal assets -- while members (owners) of an LLC are not personally liable

Because you don't have to file paperwork, setting up a general partnership is relatively inexpensive. Simplified taxes. General partnerships benefit from pass-through taxation, where taxes on the business' profits or losses pass through the business entity directly to the business owners' personal taxes.

LLCs are similar to corporations in that they offer limited liability protection to its owners. LLCs also have fewer corporate formalities and greater tax flexibility. However, one of the disadvantages is that profits may be subject to self-employment taxes.

Profits subject to social security and medicare taxes. In some circumstances, owners of an LLC may end up paying more taxes than owners of a corporation. Owners must immediately recognize profits. Fewer fringe benefits.

A general partnership is a business arrangement by which two or more individuals agree to share in all assets, profits, and financial and legal liabilities of a jointly-owned business.Furthermore, any partner may be sued for the business's debts.