Maryland Installments Fixed Rate Promissory Note Secured by Commercial Real Estate

Overview of this form

The Maryland Installments Fixed Rate Promissory Note Secured by Commercial Real Estate is a legal document in which a borrower promises to repay a loan with a fixed interest rate over a specified period. This form is specifically used when a commercial property serves as collateral for the loan, distinguishing it from unsecured promissory notes. Additionally, it is essential to execute a separate deed of trust or mortgage to secure the loan adequately.

Form components explained

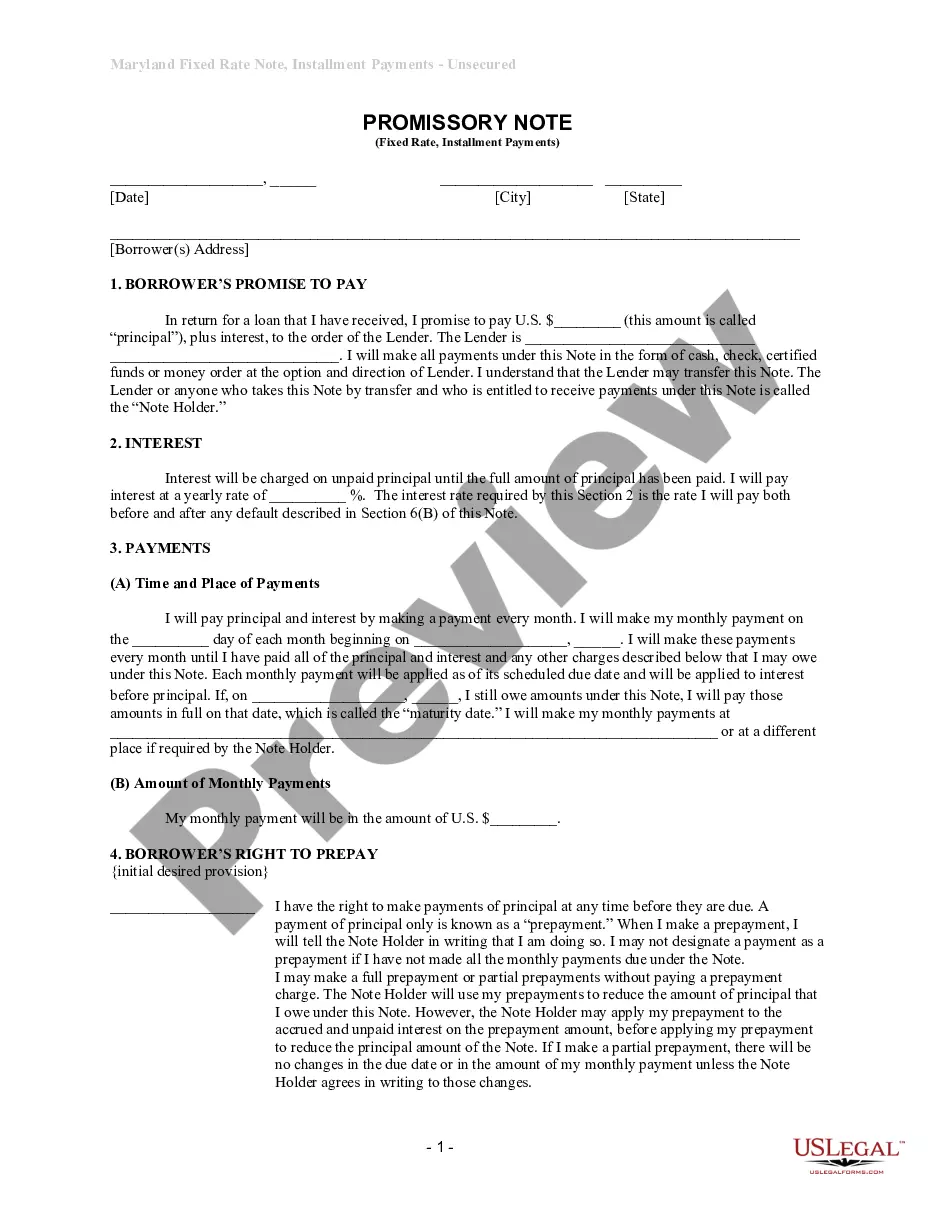

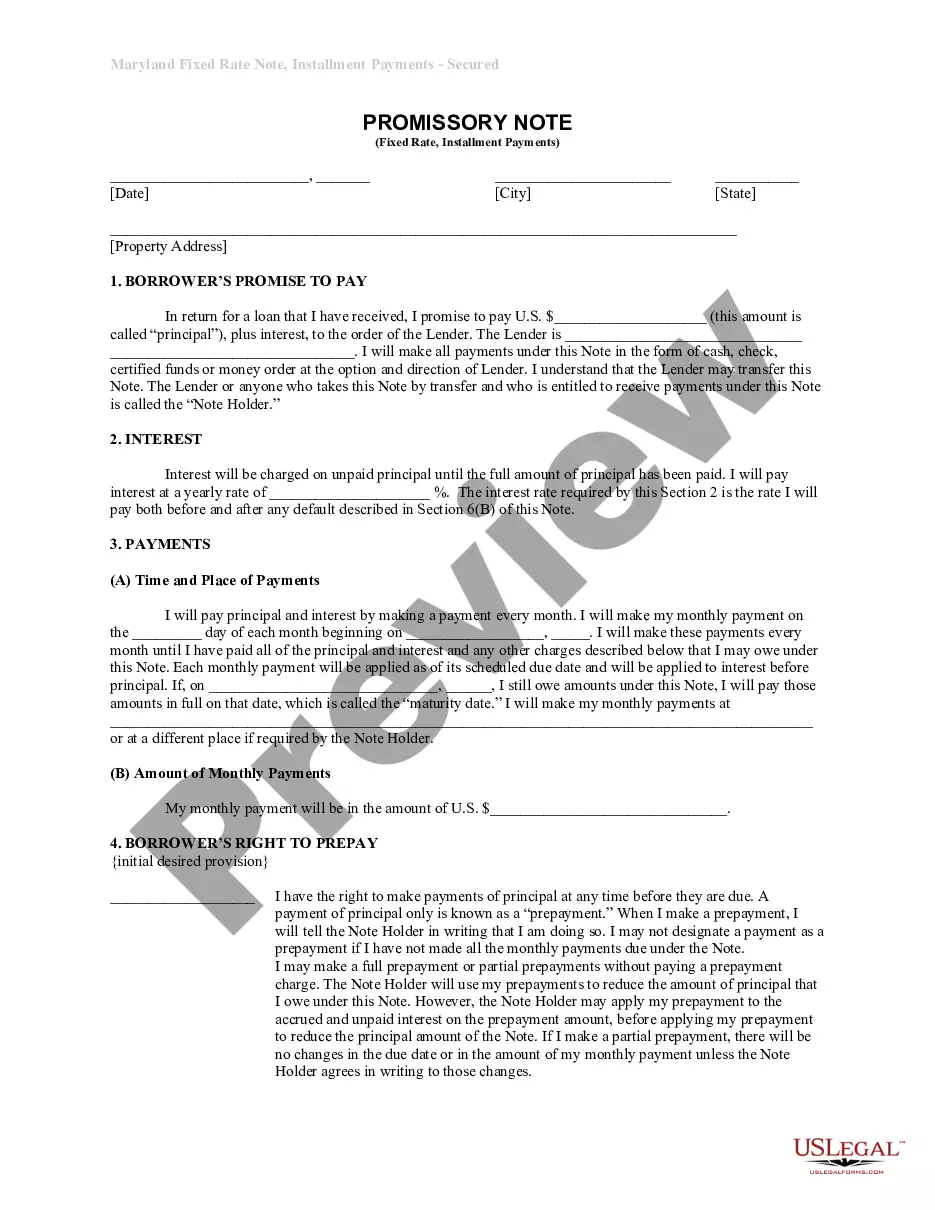

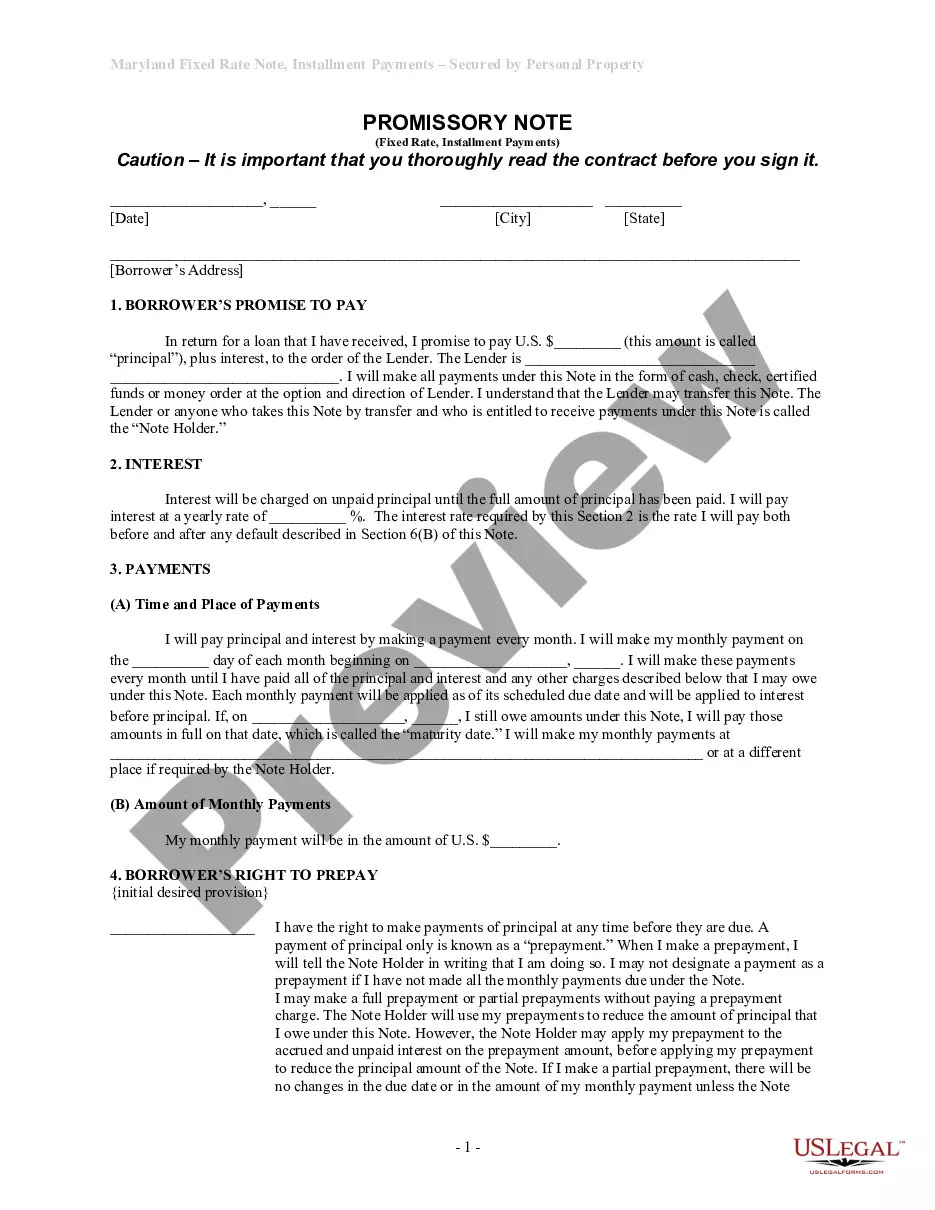

- Borrower's details, including the address and the lender's name.

- Principal amount of the loan and interest rate charged.

- Payment schedule outlining monthly payment amounts and due dates.

- Borrower's right to prepay without penalty, under specified conditions.

- Consequences of late payments and provisions for default.

- Secured nature of the note with a detailed description of the collateral.

Situations where this form applies

This form is appropriate for borrowers who are acquiring a loan secured by commercial real estate. It is often used in situations where a business needs financing for property purchases or renovations, and it requires the backing of the property itself to mitigate lender risk. Use this form when you are prepared to enter into a secured loan agreement with clear repayment terms.

Who this form is for

- Business owners seeking to finance the purchase of commercial property.

- Lenders providing loans secured by real estate as collateral.

- Real estate investors looking to formalize loan agreements.

- Individuals or entities needing a structured repayment plan for real estate investment financing.

Steps to complete this form

- Identify the parties involved by providing the names and addresses of the borrower and lender.

- Specify the principal amount of the loan and the annual interest rate.

- Fill in the payment schedule, including the monthly payment amount and the start date.

- Detail any rights to prepay the loan along with terms regarding penalties, if applicable.

- Review the notice and default provisions to ensure understanding of the consequences of late payments.

- Obtain signatures from all parties involved to finalize the agreement.

Notarization guidance

Notarization is required for this form to take effect. Our online notarization service, powered by Notarize, lets you verify and sign documents remotely through an encrypted video session, available 24/7.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Avoid these common issues

- Failing to specify the correct principal amount or interest rate.

- Not including required information about the property securing the note.

- Overlooking the need for a separate deed of trust or mortgage.

- Ignoring state-specific laws that might affect terms or provisions.

- Forgetting to obtain all necessary signatures before executing the document.

Why complete this form online

- Convenient access to customizable templates tailored to your needs.

- Time-saving, allowing you to fill out and download the form instantly.

- Reliability as documents are drafted by licensed attorneys to ensure legal validity.

- Easy edits and adjustments to meet your specific requirements.

- Secure storage of your completed forms for future reference.

Looking for another form?

Form popularity

FAQ

There are four significant types of promissory notes in India. A personal note is the kind of promissory note that an individual should seek when lending money to family members or close relatives. A commercial note is the type of promissory note that is signed between a borrower and a financial institution.

When a loan changes hands, the promissory note is endorsed (signed over) to the new owner of the loan. In some cases, the note is endorsed in blank which makes it a bearer instrument under Article 3 of the Uniform Commercial Code. So, any party that possesses the note has the legal authority to enforce it.

The individual who promises to pay is the maker, and the person to whom payment is promised is called the payee or holder. If signed by the maker, a promissory note is a negotiable instrument.

A promissory note can be secured with a pledge of collateral, which is something of value that can be seized if a borrower defaults.

What Is a Promissory Note? A promissory note is a financial instrument that contains a written promise by one party (the note's issuer or maker) to pay another party (the note's payee) a definite sum of money, either on demand or at a specified future date.

What is the difference between a Promissory Note and a Loan Agreement? Both contracts evidence a debt owed from the Borrower to the Lender, but the Loan Agreement contains more extensive clauses than the Promissory Note. Further, only the Borrower signs the promissory note while both parties sign a loan agreement.

The lender holds the promissory note while the loan is being repaid, then the note is marked as paid and returned to the borrower when the loan is satisfied. Promissory notes aren't the same as mortgages, but the two often go hand in hand when someone is buying a home.

A simple promissory note might be for a lump sum repayment on a certain date. For example, you lend your friend $1,000 and he agrees to repay you by December 1. The full amount is due on that date, and there is no payment schedule involved.

Personal Promissory Notes This is a particular loan taken from family or friends. Commercial Here, the note is made when dealing with commercial lenders such as banks. Real Estate This is similar to commercial notes in terms of nonpayment consequences.