Limited Liability Company Pllc With Multiple Owners

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

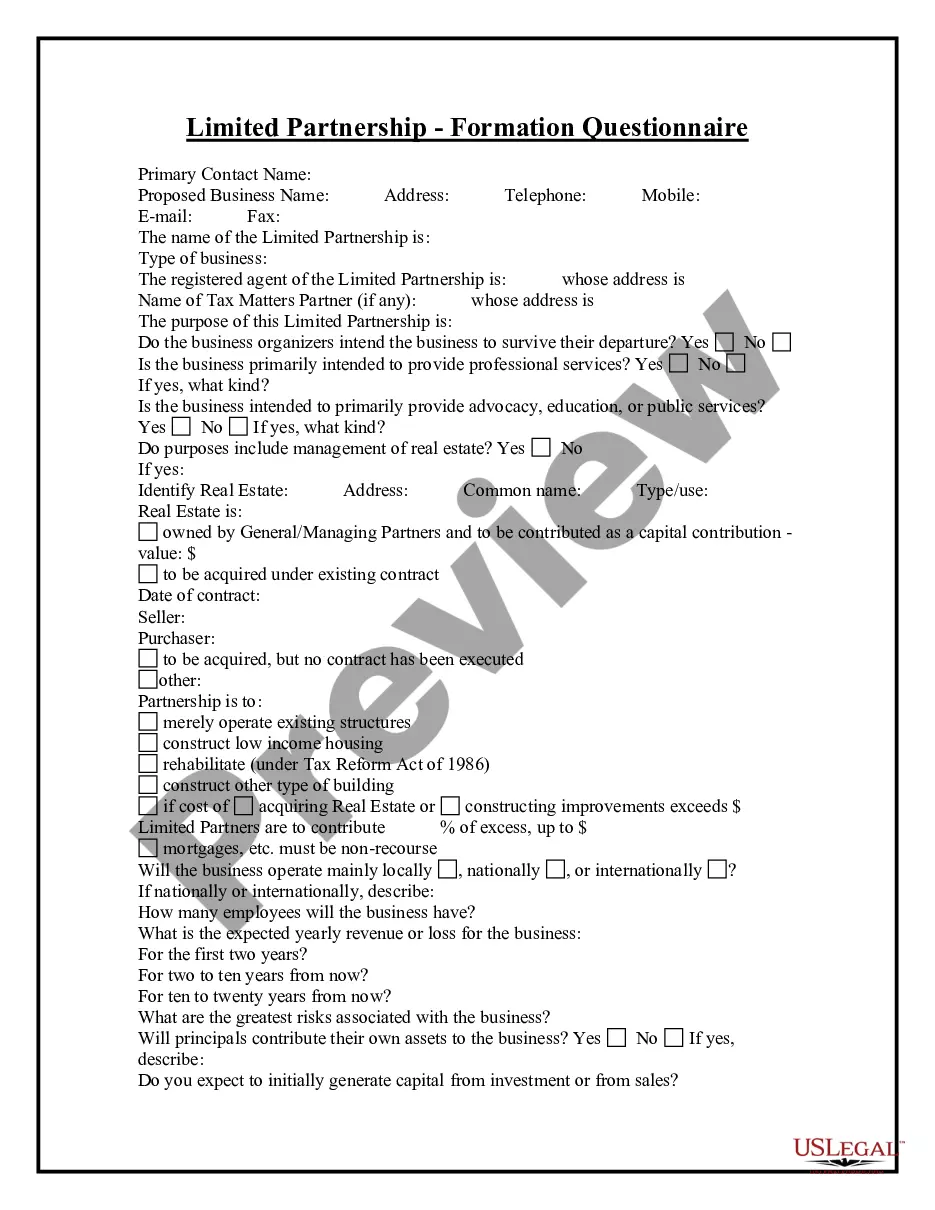

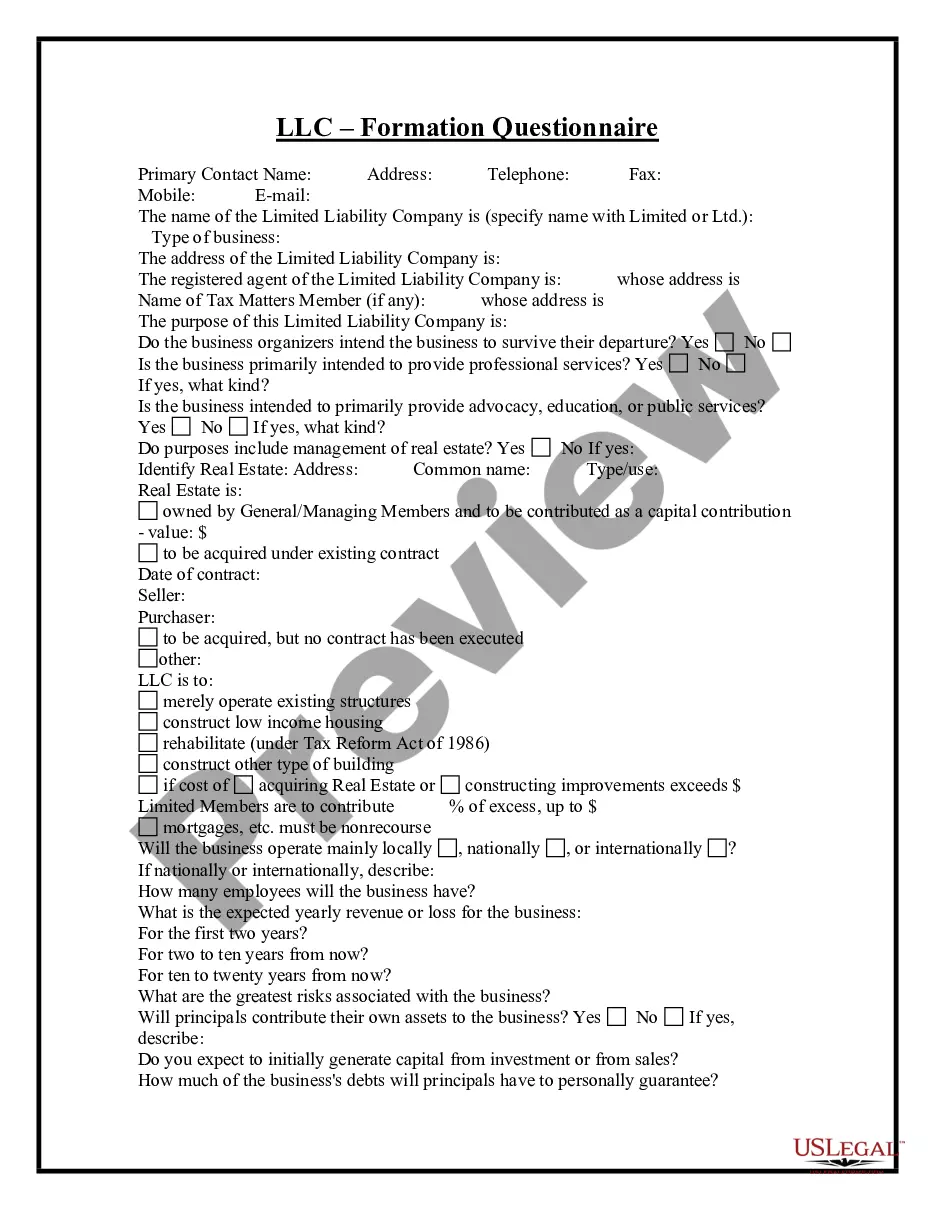

How to fill out Professional Limited Liability Company - PLLC - Formation Questionnaire?

Handling legal documentation and procedures may be a lengthy addition to your entire schedule.

Limited Liability Company Pllc With Multiple Owners and similar forms typically require you to look for them and figure out how to complete them correctly.

Thus, whether you are managing financial, legal, or personal affairs, employing an all-encompassing and user-friendly online directory of forms readily available will be very beneficial.

US Legal Forms is the premier online platform for legal documents, featuring over 85,000 state-specific forms and numerous tools to assist you in completing your paperwork effortlessly.

Is this your first experience using US Legal Forms? Create and set up an account in just a few minutes and you will gain access to the form directory and Limited Liability Company Pllc With Multiple Owners. Then, follow the steps below to complete your form.

- Examine the directory of suitable documents available to you with just one click.

- US Legal Forms provides state- and county-specific documents accessible at any time for downloading.

- Protect your document management processes with a high-quality service that enables you to prepare any form in minutes without extra or concealed charges.

- Simply Log In to your account, locate Limited Liability Company Pllc With Multiple Owners, and download it immediately from the My documents section.

- You can also access previously downloaded forms.

Form popularity

FAQ

Yes, two people can form a limited liability company pllc with multiple owners. This type of structure allows both individuals to share the profits, losses, and management responsibilities. By filing together, they can enjoy the legal protections that an LLC offers, while also benefiting from flexible management options. Using platforms like US Legal Forms can simplify the filing process for forming your LLC.

A limited liability company (PLLC) can have one or more owners. There is no strict limit on the number of members, which makes the PLLC an attractive choice for entrepreneurial groups or partnerships. Each member shares in the management and profits of the business, ensuring all owners have a stake in its success. Whether you are a solo practitioner or a group of professionals, a PLLC can accommodate your needs effectively.

Certainly, two people can own a limited liability company (PLLC) equally, sharing ownership and decision-making power. This equal partnership encourages collaboration and aligns both parties towards common business goals. Often, members outline their respective rights and responsibilities in an operating agreement to ensure clarity. This structured approach can foster a positive working relationship, enhancing the overall functionality of the PLLC.

Indeed, a limited liability company (PLLC) can have multiple owners, also referred to as members. This aspect is one of the primary benefits of forming a PLLC, as it allows individuals to pool their resources, share profits, and manage the business collectively. Each owner's liability is limited to their investment, which protects their personal assets. If you're considering forming a PLLC, this cooperative aspect can lead to a stronger, more resilient company.

Yes, a professional limited liability company (PLLC) can absolutely have multiple members. This structure allows licensed professionals, like lawyers or doctors, to come together under one entity while enjoying personal liability protection. Each member can actively participate in the company’s management or invest capital, contributing to its success. Thus, a PLLC truly facilitates effective cooperation among multiple owners in a professional setting.

A limited liability company (PLLC) with multiple owners operates under a flexible structure, allowing owners to share profits and responsibilities. Each member typically contributes to the capital and participates in management decisions, promoting collaboration. This type of setup provides personal liability protection for each member, shielding their personal assets from the company's debts and legal issues. Choosing to form a PLLC can be a strategic decision for owners looking to minimize risk while working together.

To split up ownership of a limited liability company (PLLC) with multiple owners, you should start by drafting an operating agreement. This document outlines the ownership percentages, roles, responsibilities, and profit distribution among the members. It's essential to have clear communication between all members to ensure everyone agrees to the terms. Using a platform like US Legal Forms can simplify this process, providing you with templates that help you create a tailored operating agreement reflecting your business's unique needs.