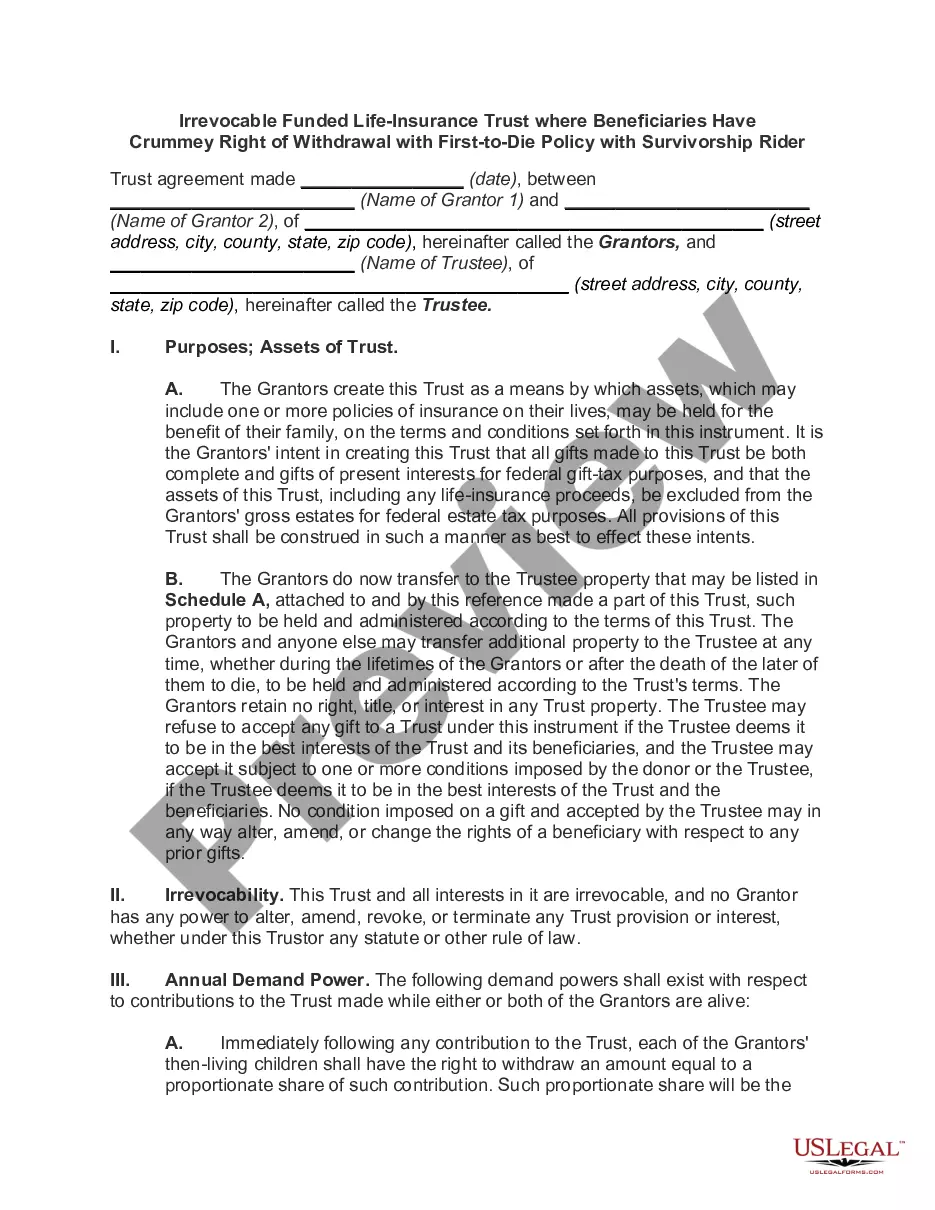

Irrevocable Life Insurance Trust

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Irrevocable Life Insurance Trust - Beneficiaries Have Crummey Right Of Withdrawal?

- Log in to your US Legal Forms account if you're a returning user to access your saved documents and download the necessary ILIT form.

- If you are new to US Legal Forms, start by reviewing the available documents in the preview mode to ensure you select the appropriate ILIT template for your needs.

- Use the search functionality if you're unable to find the correct form, to locate a suitable alternative that fits your local requirements.

- Purchase the selected document by choosing the preferred subscription plan and completing the registration process to access the full library.

- Finalize your transaction securely by entering payment details, either through credit card or PayPal, to complete your purchase.

- Once processed, download your completed form and save it for easy access through the 'My Forms' section of your profile whenever necessary.

US Legal Forms stands out with its robust collection of over 85,000 legal documents, ensuring that you can find precisely what you need. With access to premium experts who can assist in form completion, you can be confident in the legality and precision of your documents.

Start your journey towards effective estate planning by utilizing US Legal Forms today. Empower your legal processes and ensure your family's future is protected.

Form popularity

FAQ

One notable downside of an irrevocable trust is that it may lack the flexibility to adapt to changing life circumstances. When you set up an Irrevocable Life Insurance Trust, you cannot easily make alterations, which can create challenges down the line. Furthermore, you must comply with specific trust management and tax rules, which can be complex and require professional assistance.

The disadvantages of an Irrevocable Life Insurance Trust (ILIT) include limited flexibility and potential difficulties in management. Once established, making changes can require agreement from all beneficiaries, which is not always feasible. Additionally, the costs of setting up and maintaining the trust can be higher than simpler estate planning tools.

The primary danger of an irrevocable trust, such as an Irrevocable Life Insurance Trust, is the permanent transfer of assets. Once you place your life insurance policy into the trust, you cannot retrieve it or alter the trust terms easily. This can lead to complications if your circumstances change or if you need access to those funds in the future.

You should consider using an Irrevocable Life Insurance Trust (ILIT) when you want to keep life insurance proceeds out of your taxable estate. It effectively avoids estate taxes and provides a way to manage how the death benefit is distributed. An ILIT is particularly beneficial when you have a significant life insurance policy and want to ensure your beneficiaries receive the full benefit without tax implications.

One downside of an Irrevocable Life Insurance Trust (ILIT) is the loss of control over the policy assets once transferred. You cannot change beneficiaries or adjust the terms of the trust without the consent of all beneficiaries. Additionally, the trust must follow strict management rules, which can add complexity to your estate planning.

Creating an irrevocable life insurance trust involves several steps. First, you should draft a trust document outlining the terms and designate a trustee to manage the assets. Next, you will need to fund the trust with your life insurance policy and complete any necessary paperwork to transfer ownership. Platforms like Uslegalforms can guide you through each stage and offer resources to ensure your irrevocable life insurance trust is established successfully.

You can create an irrevocable life insurance trust yourself, but it requires careful consideration. It is essential to understand the legal requirements and implications involved in setting it up. While templates and guides are available, consulting a legal professional can ensure your trust meets all legal standards and goals. Using a platform like Uslegalforms can simplify the process and provide the necessary documents to help you create your irrevocable life insurance trust correctly.

The significance of the 3-year rule for irrevocable life insurance trust lies in its impact on estate planning strategies. This rule dictates that any policy transferred within three years of death may still be treated as part of the gross estate, potentially triggering estate taxes. Thus, being proactive and planning transfers well in advance can help you maximize tax savings and protect your beneficiaries, and resources from USLegalForms can guide you through this process effectively.

The 3-year rule for an irrevocable life insurance trust states that if you transfer an insurance policy into the trust within three years of your death, the death benefit may be included in your estate for tax purposes. This rule helps prevent individuals from evading estate taxes by simply transferring assets just before death. Being aware of this rule is crucial while planning your estate, so consider seeking expert advice for a deeper understanding.

An irrevocable life insurance trust can be a beneficial tool for individuals looking to mitigate estate taxes and protect assets. By removing the life insurance policy from your estate, you can often reduce tax liabilities and ensure that funds go directly to your beneficiaries. It's important to evaluate your unique financial situation, and consulting with a financial advisor can provide clarity on whether this trust aligns with your goals.