Subrogation With Car Insurance

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Subrogation Agreement Between Insurer And Insured?

- Start by visiting the US Legal Forms website and logging into your account. If you're new, create an account to access the form library.

- Use the search function to find the specific subrogation with car insurance template that meets your jurisdiction's requirements.

- Preview the form to ensure it aligns with your needs, evaluating descriptions and any sample content provided.

- Select the desired form and choose a subscription plan that suits your needs by clicking 'Buy Now.'

- Complete your purchase by entering your payment details via credit card or PayPal.

- Download the completed form to your device. You can always retrieve it later from your account's 'My Forms' section.

With US Legal Forms, you benefit from a vast library of over 85,000 forms designed to simplify your legal processes. Access premium support from legal experts to ensure accuracy and compliance.

Get started today and make the legal document process easier. Visit US Legal Forms to explore your options!

Form popularity

FAQ

Ignoring subrogation with car insurance can lead to severe repercussions. If you do not address the matter, your insurance provider may take legal action to recover costs, potentially resulting in a court judgment against you. This judgment could further affect your credit rating and lead to increased premiums in the future. To avoid these outcomes, it’s advisable to treat subrogation requests seriously and seek help if needed.

Yes, it is essential to respond to a subrogation letter. Ignoring this communication can lead to more significant financial and legal issues down the road. Responding allows you to clarify your position and, if necessary, dispute any claims made against you. If you need assistance, you may find valuable resources on platforms like uslegalforms to guide you through dealing with subrogation with car insurance.

Subrogation with car insurance has both advantages and disadvantages. On one hand, it helps insurance companies recover costs, which can contribute to lower premiums for policyholders. On the other hand, it can create complications for individuals who may not fully understand their rights and responsibilities. Ultimately, whether it's good or bad varies based on individual circumstances, so understanding the process is crucial.

Failing to respond to a subrogation request can lead to serious consequences. Your insurance company may pursue legal action against you to recover the costs related to the accident. Additionally, ignoring subrogation with car insurance can negatively impact your credit score and future insurance rates. To avoid these issues, it's best to address the matter promptly.

If you receive a subrogation letter regarding your car insurance, first read it carefully. This letter explains that your insurance company is seeking reimbursement from another party for costs related to your accident. It's essential to gather any relevant documents, such as accident reports and medical bills, and respond promptly. If you're unsure about the process, consider seeking help from a legal professional to navigate subrogation with car insurance effectively.

The timeframe for subrogation with car insurance can vary widely. Generally, it depends on the complexity of the case and the willingness of the responsible party to settle. Some cases may resolve quickly, while others could take several months or longer. Using platforms like uslegalforms can streamline the process by providing necessary documentation and guidance to both parties.

The rules of subrogation with car insurance establish the framework for recovery. Insurers typically cannot subrogate against their own policyholders. Additionally, subrogation actions must be timely filed within the statute of limitations. Understanding these rules helps insured individuals navigate their claims and the insurer's recovery options effectively.

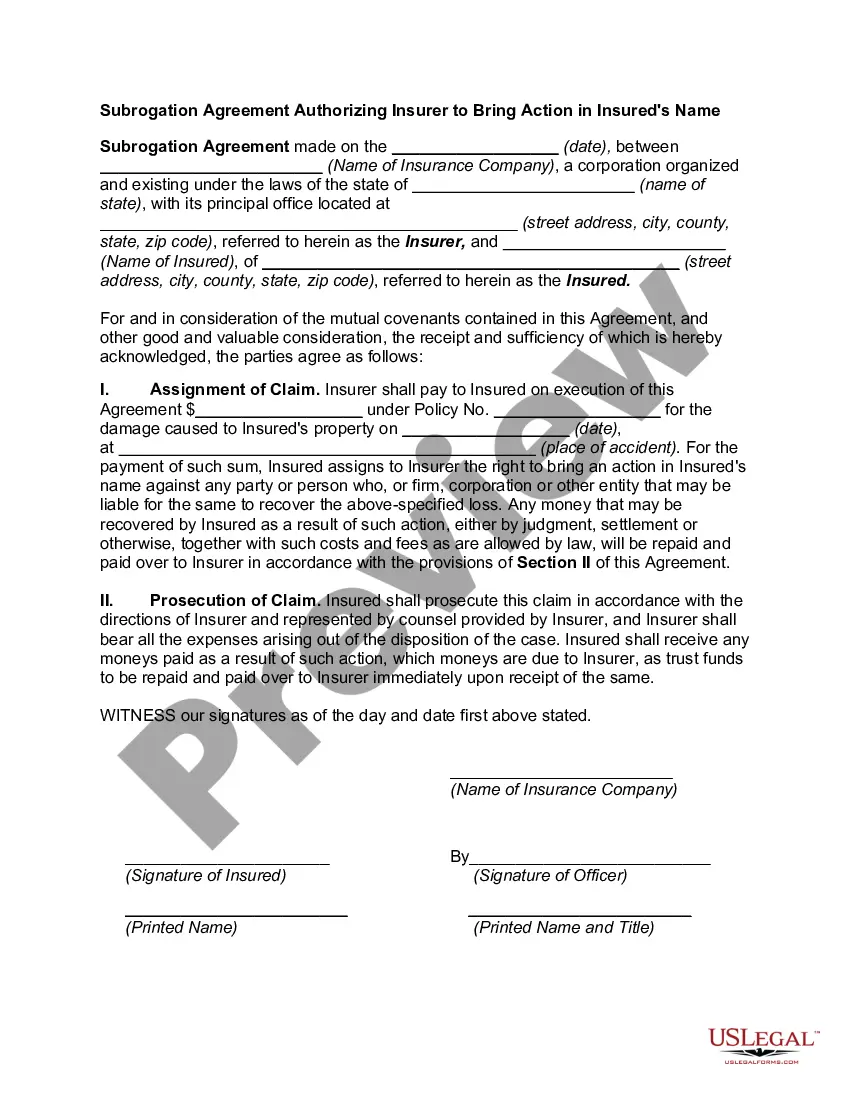

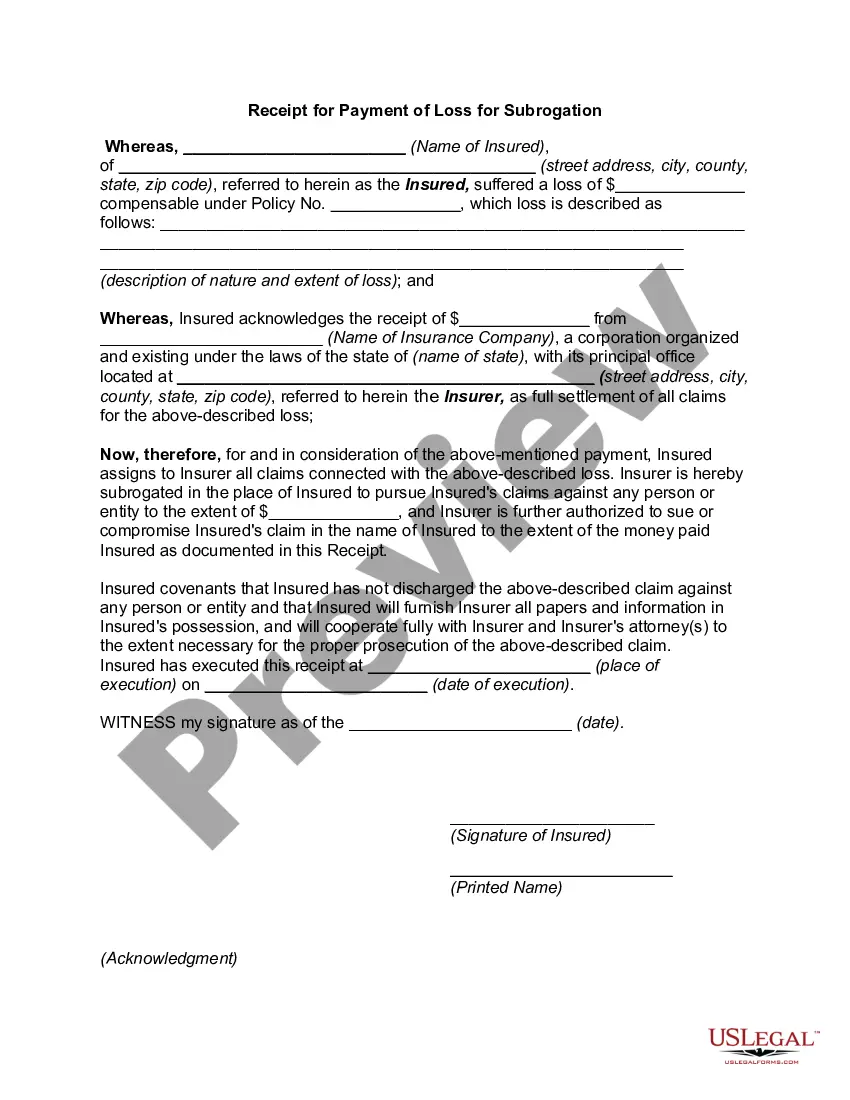

The subrogation condition in car insurance requires that the insurer maintains the right to seek recovery after paying a claim. This means that, after compensating the insured, the insurer can take legal action against the party responsible for the loss. It’s important for policyholders to understand this provision, as it affects both their rights and obligations following an accident.

The three principles of subrogation with car insurance include the right to recovery, the duty to mitigate loss, and the obligation to reimburse. First, the insurer has the right to pursue the third party after they cover the claim. Secondly, the insured must minimize further losses during this process. Lastly, if the insured receives compensation from both the third party and their insurer, they must repay the insurer for the overpayment.

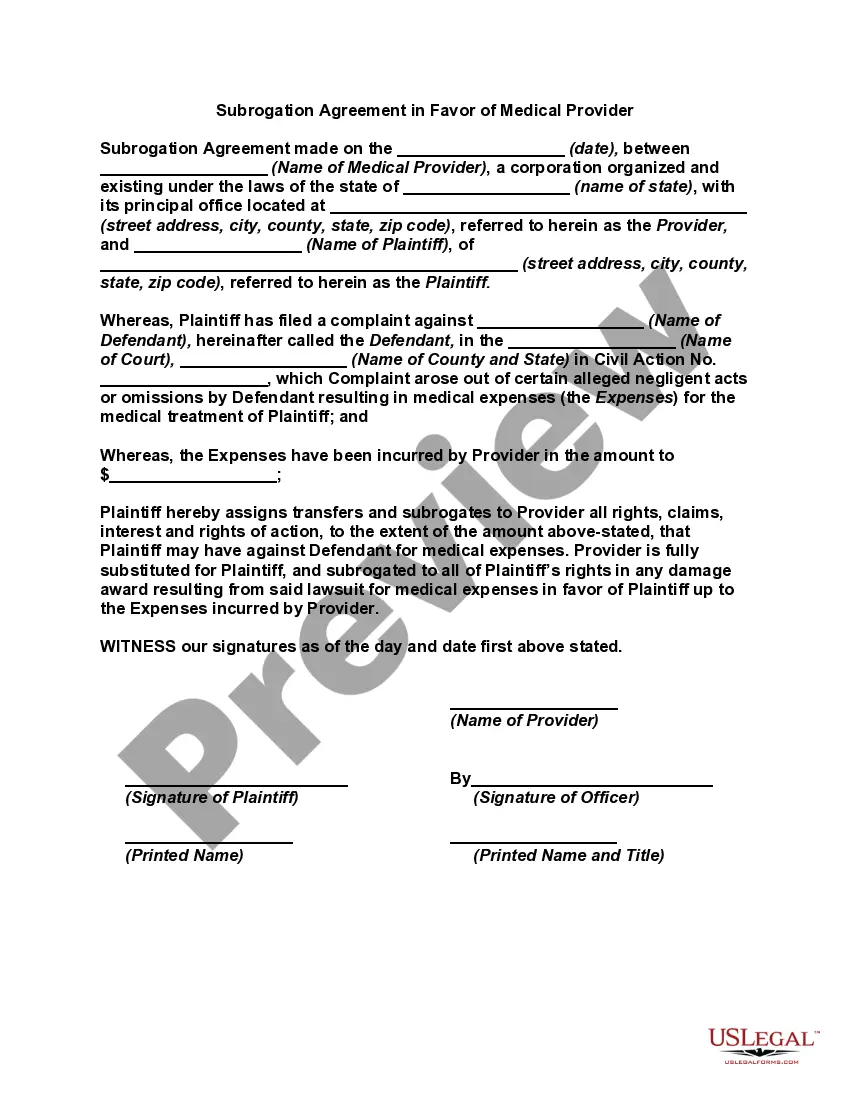

A simple example of the principle of subrogation occurs when someone slips and falls in a store due to negligence. If their insurance covers medical bills, they can later have their insurer pursue subrogation against the store's insurance. This illustrates how subrogation with car insurance, in general, ensures that the party at fault bears the financial responsibility.