Personal Residence Trust Sample With Tax

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Personal Residence Trust?

It’s clear that you cannot transform into a legal expert instantly, nor can you quickly learn how to effectively create a Personal Residence Trust Sample With Tax without a specific skill set.

Drafting legal documents is a lengthy procedure that necessitates certain education and expertise. So why not entrust the development of the Personal Residence Trust Sample With Tax to the professionals.

With US Legal Forms, one of the most extensive libraries of legal templates, you can find everything from court documents to templates for internal business communication. We recognize the importance of compliance and adherence to both federal and state regulations.

You can regain access to your documents from the My documents tab at any time. If you are an existing customer, you can simply Log In, and find and download the template from the same section.

Regardless of the intent behind your documents—whether they are for financial, legal, or personal use—our platform has you covered. Experience US Legal Forms today!

- Find the form you need using the search bar at the top of the page.

- Preview it (if this feature is available) and review the supporting description to determine whether the Personal Residence Trust Sample With Tax meets your needs.

- Start your search again if you require a different template.

- Create a free account and select a subscription plan to purchase the template.

- Click Buy now. Once the payment is completed, you can download the Personal Residence Trust Sample With Tax, complete it, print it, and deliver it or send it by mail to the necessary individuals or organizations.

Form popularity

FAQ

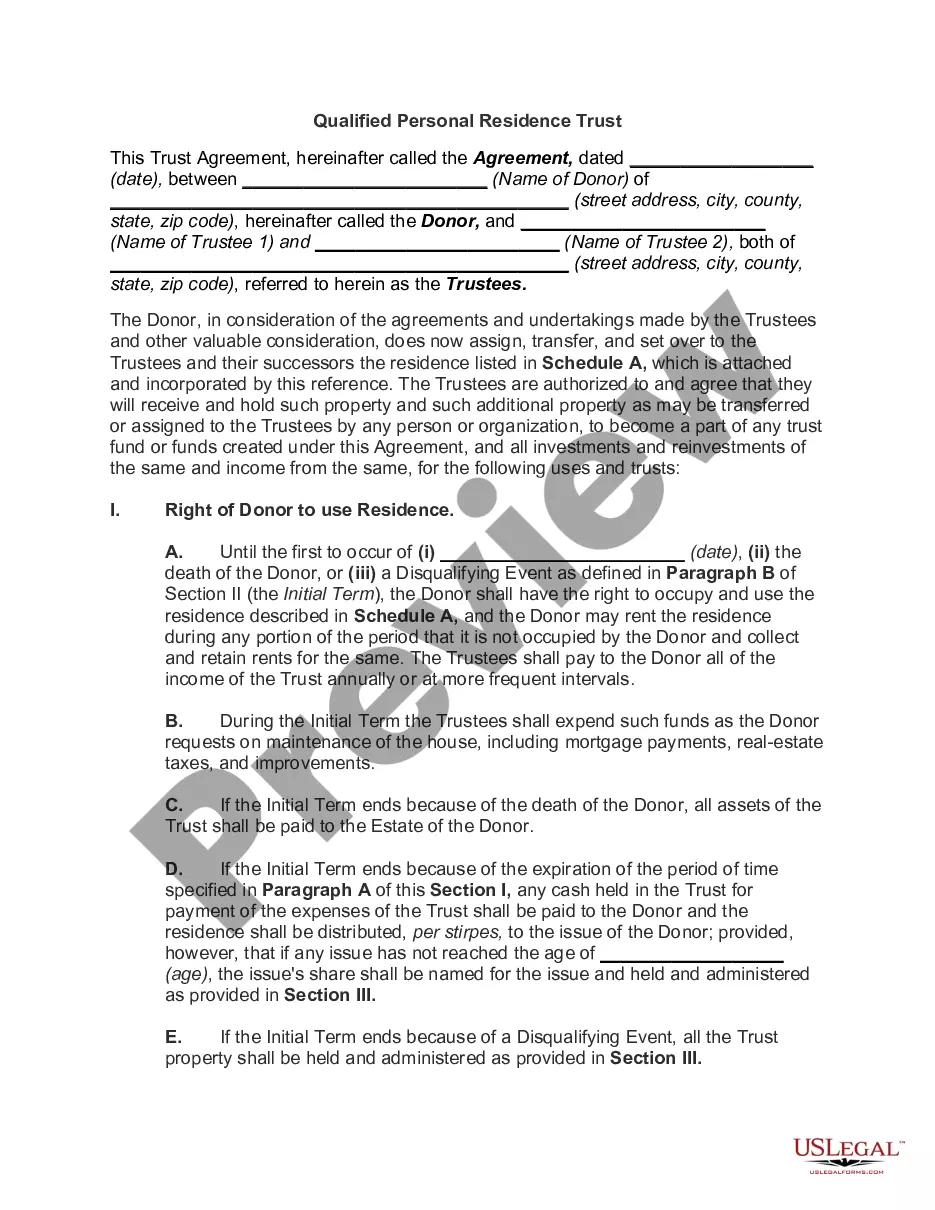

A PRT is very limited and inflexible, because it must not hold any assets other than the residence and must not allow the sale of the residence. A QPRT can hold limited amounts of cash for expenses or improvements to the residence, and can allow the residence to be sold (but not to the grantor or the grantor's spouse).

There is no set limit on the term of a QPRT. Setting the term length is one of the most important aspects of the Trust. It should be set up such that it expires before you pass away. Otherwise, the property goes back into the estate and will be subject to estate taxes, including gift taxes.

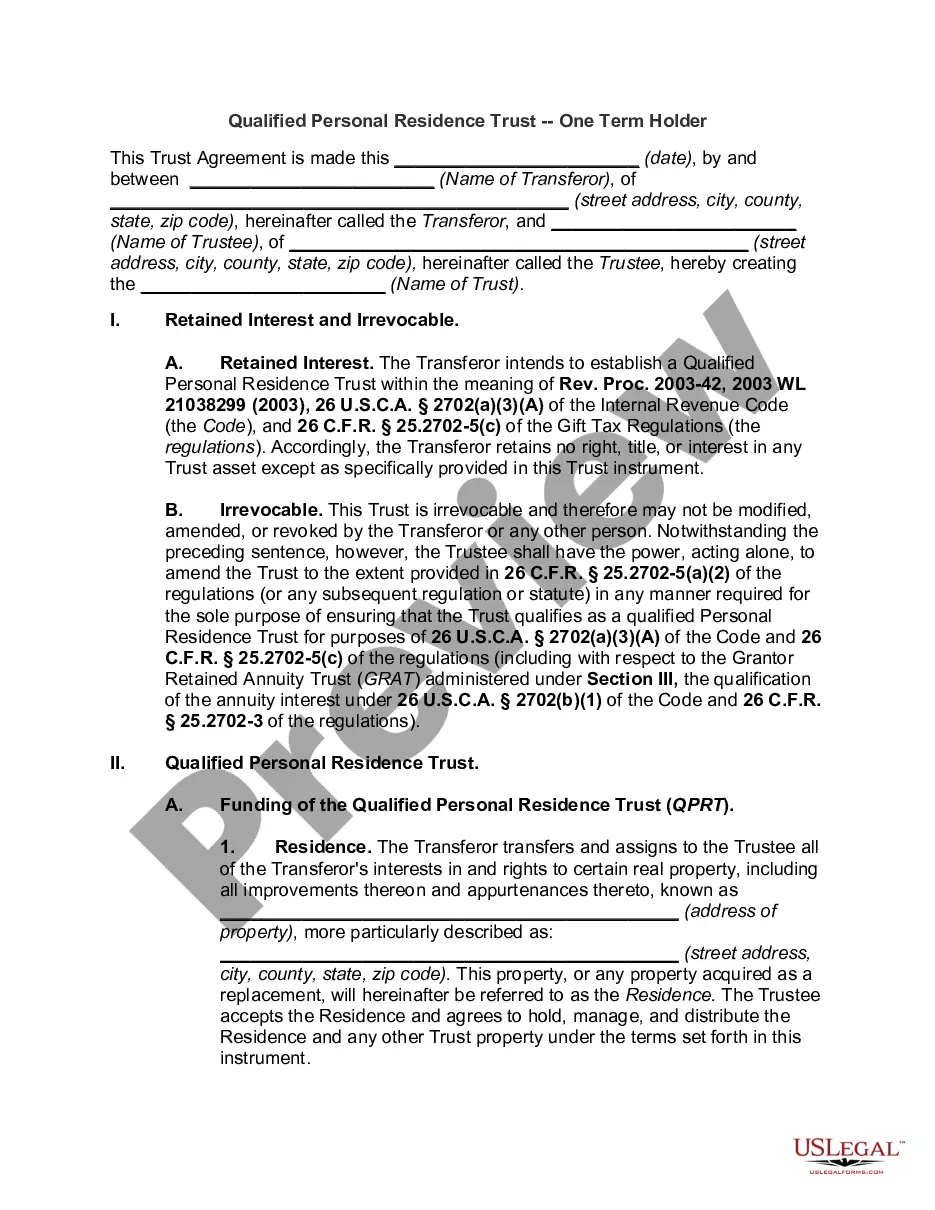

A Qualified Personal Residence Trust (?QPRT?) is an irrevocable trust that holds either a Grantor's personal residence or occasional residence for a certain term, then distributes the property to named beneficiaries at the end of the term.

What happens at the end of the QPRT term? Once the QPRT terminates and the beneficiary becomes the owner of the property, the Grantor can pay rent in exchange for the use of the property.

To calculate this value, the program determines the value of the interest retained by the grantor (income interest plus reversion). It then subtracts the value of the grantor's retained interest from the principal placed into the trust. The result is the taxable portion of the QPRT.