Bankruptcy Hardship Discharge Foreclosure

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

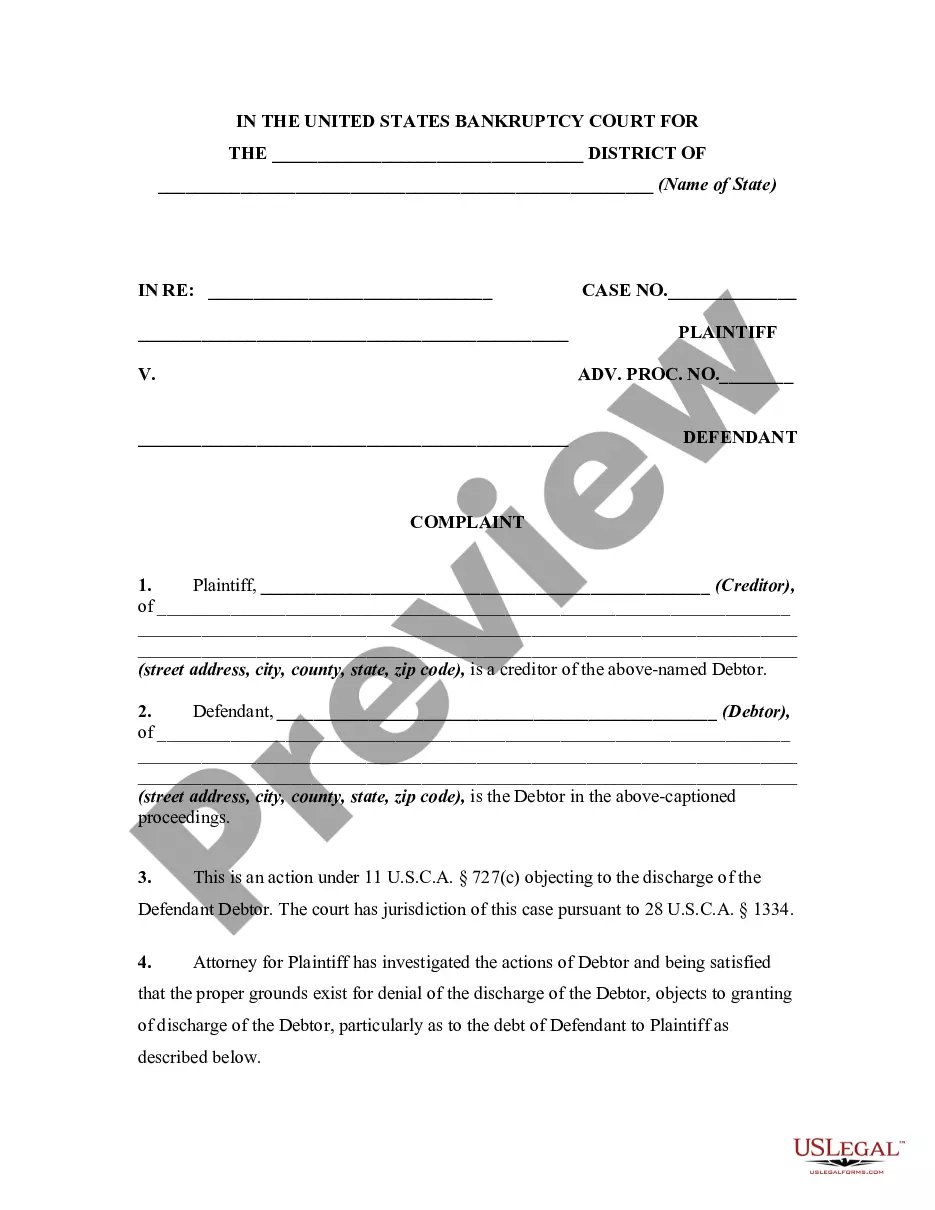

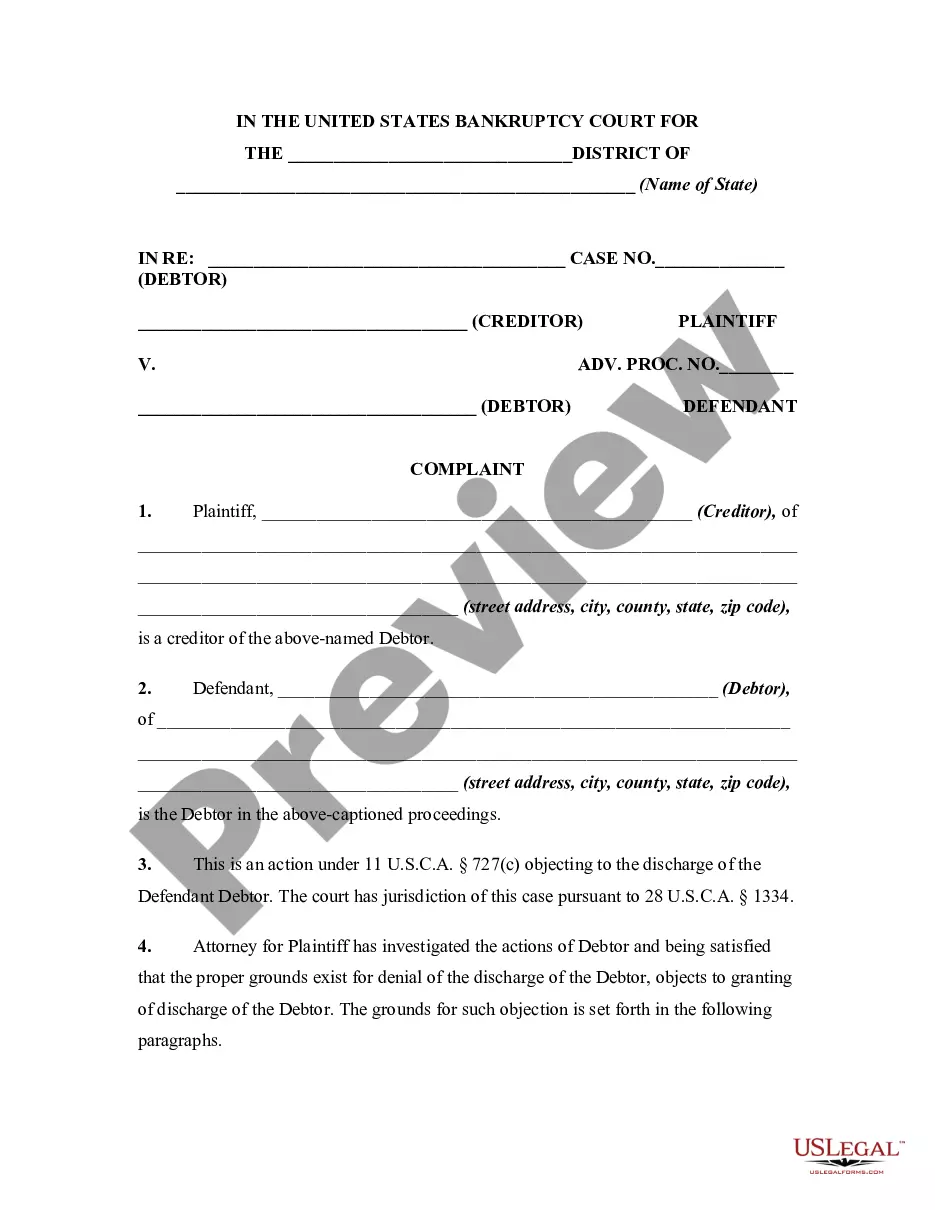

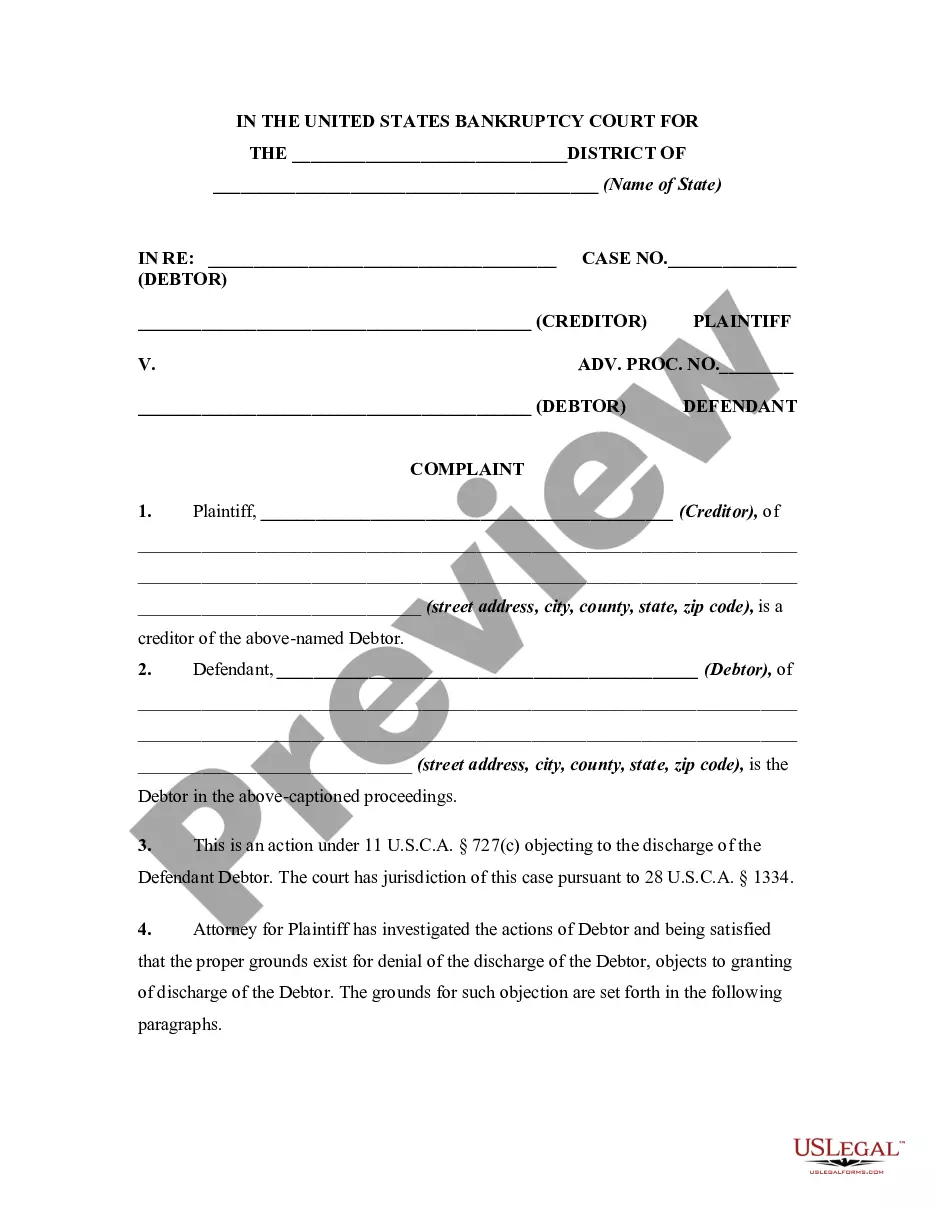

How to fill out Complaint Objecting To Discharge In Bankruptcy Proceedings For Concealment By Debtor And Omitting From Schedules Fraudulently Transferred Property?

Regardless of whether for corporate objectives or personal issues, everyone encounters legal circumstances at some stage in their life. Filling out legal forms requires meticulous care, starting with selecting the appropriate template sample.

For example, if you choose an incorrect version of a Bankruptcy Hardship Discharge Foreclosure, it will be denied upon submission. Thus, it is vital to have a trustworthy source of legal documents such as US Legal Forms.

With an extensive US Legal Forms catalog available, you don’t need to waste time searching for the correct template online. Utilize the library’s user-friendly navigation to find the appropriate template for any scenario.

- Locate the template you need by utilizing the search bar or browsing the catalog.

- Review the form’s details to confirm it aligns with your circumstances, state, and county.

- Click on the form’s preview to examine it.

- If it is the incorrect document, return to the search option to find the Bankruptcy Hardship Discharge Foreclosure sample you need.

- Obtain the template once it fulfills your requirements.

- If you possess a US Legal Forms account, simply click Log in to access previously saved documents in My documents.

- If you do not have an account yet, you may purchase the form by clicking Buy now.

- Choose the appropriate pricing option.

- Fill out the account registration form.

- Select your payment method: you can utilize a credit card or PayPal account.

- Choose the file format you desire and download the Bankruptcy Hardship Discharge Foreclosure.

- Once it is downloaded, you can complete the form using editing software or print it and finish it manually.

Form popularity

FAQ

For example, if your income goes down during bankruptcy, you might be able to modify your plan to reduce your payment amount. A judge can reduce the amount you're paying toward nonpriority, unsecured debt, such as credit card balances, medical bills, and personal loans.

In Chapter 13 bankruptcy, the debtor proposes a repayment plan to manage a portion of their debts over three to five years. The remaining debts are typically discharged at the end of the repayment plan. Monthly payment amounts vary greatly, as one of the factors they are based on is disposable income.

The Chapter 13 Hardship Discharge After confirmation of a plan, circumstances may arise that prevent the debtor from completing the plan. In such situations, the debtor may ask the court to grant a "hardship discharge."

A hardship discharge is granted to help a debtor who cannot complete a Chapter 13 debt repayment plan for reasons that are completely outside the debtor's control. It will not be granted to debtors who cause their own difficulties, such as debtors who quit their jobs while making payments in a Chapter 13 plan.

A hardship discharge ends your Chapter 13 plan, so your opportunity to catch up with debt such as missed mortgage or car payments, priority tax debts or secured tax debts, or past-due child or spousal support also ends.