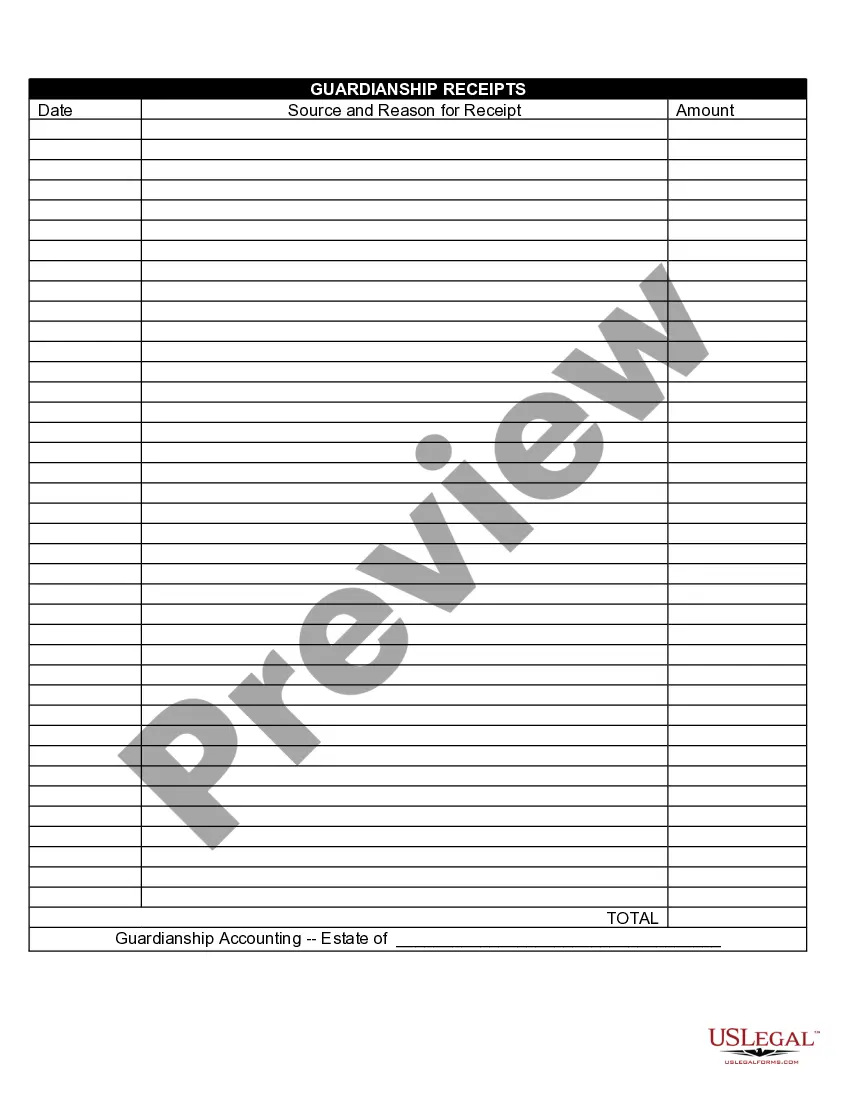

Ohio Temporary Guardianship Form For Kansas

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Ohio Standby Temporary Guardian Legal Documents Package?

The Ohio Temporary Guardianship Document For Kansas presented on this page is a reusable official template crafted by expert attorneys in accordance with federal and local regulations.

For over 25 years, US Legal Forms has supplied individuals, businesses, and legal practitioners with more than 85,000 verified, state-specific documents for various business and personal circumstances. It’s the quickest, easiest, and most reliable method to acquire the paperwork you require, as the service ensures bank-level data confidentiality and anti-malware safeguards.

Subscribe to US Legal Forms for access to verified legal templates for all of life’s situations.

- Search for the document you require and review it.

- Browse through the template you found and preview it or read the form description to confirm it meets your requirements. If it doesn’t, utilize the search bar to find the appropriate one. Click Buy Now once you’ve identified the template you need.

- Register and Log In.

- Choose the pricing plan that best fits your needs and create an account. Use PayPal or a credit card for swift payment. If you already possess an account, Log In and verify your subscription to proceed.

- Acquire the editable template.

- Select the format you prefer for your Ohio Temporary Guardianship Document For Kansas (PDF, DOCX, RTF) and download the template onto your device.

- Complete and sign the documents.

- Print the template to fill it out manually. Alternatively, utilize an online multifunctional PDF editor to quickly and accurately complete and sign your form with an eSignature.

- Download your documents once more.

- Use the same document again whenever necessary. Access the My documents tab in your profile to redownload any previously purchased forms.

Form popularity

FAQ

Some examples of violations are the improper disclosure of the amount financed, finance charge, payment schedule, total of payments, annual percentage rate, and security interest disclosures. Under TILA, a creditor can be strictly liable for any violations, meaning that the creditor's intent is not relevant.

Share This Page: The Truth in Lending Act (TILA) protects you against inaccurate and unfair credit billing and credit card practices. It requires lenders to provide you with loan cost information so that you can comparison shop for certain types of loans.

An extraordinary event beyond the control of any interested party or other unexpected event specific to the consumer or transaction (A natural disaster, such as a hurricane or earthquake).

It replaces the GFE provided under RESPA and the initial disclosure provided under TILA. What form is used to provide the Loan Estimate? CFPB has provided a standard Loan Estimate form, which you must use for ?federally related mortgage loans? subject to RESPA.

Lenders have to provide borrowers a Truth in Lending disclosure statement. It has handy information like the loan amount, the annual percentage rate (APR), finance charges, late fees, prepayment penalties, payment schedule and the total amount you'll pay.

The Truth in Lending Act (and Regulation Z) explains which transactions are exempt from the disclosure requirements, including: loans primarily for business, commercial, agricultural, or organizational purposes. federal student loans.

TILA's provisions cover two types of credit: open-end and closed-end. Open-end: Open-end credit includes home equity lines of credit (HELOCs), credit cards, reverse mortgages and bank-issued cards. Closed-end: A closed-end credit has a set amount, like home equity loans, mortgage loans and car loans.

The Truth in Lending Act, or TILA, also known as regulation Z, requires lenders to disclose information about all charges and fees associated with a loan. This 1968 federal law was created to promote honesty and clarity by requiring lenders to disclose terms and costs of consumer credit.